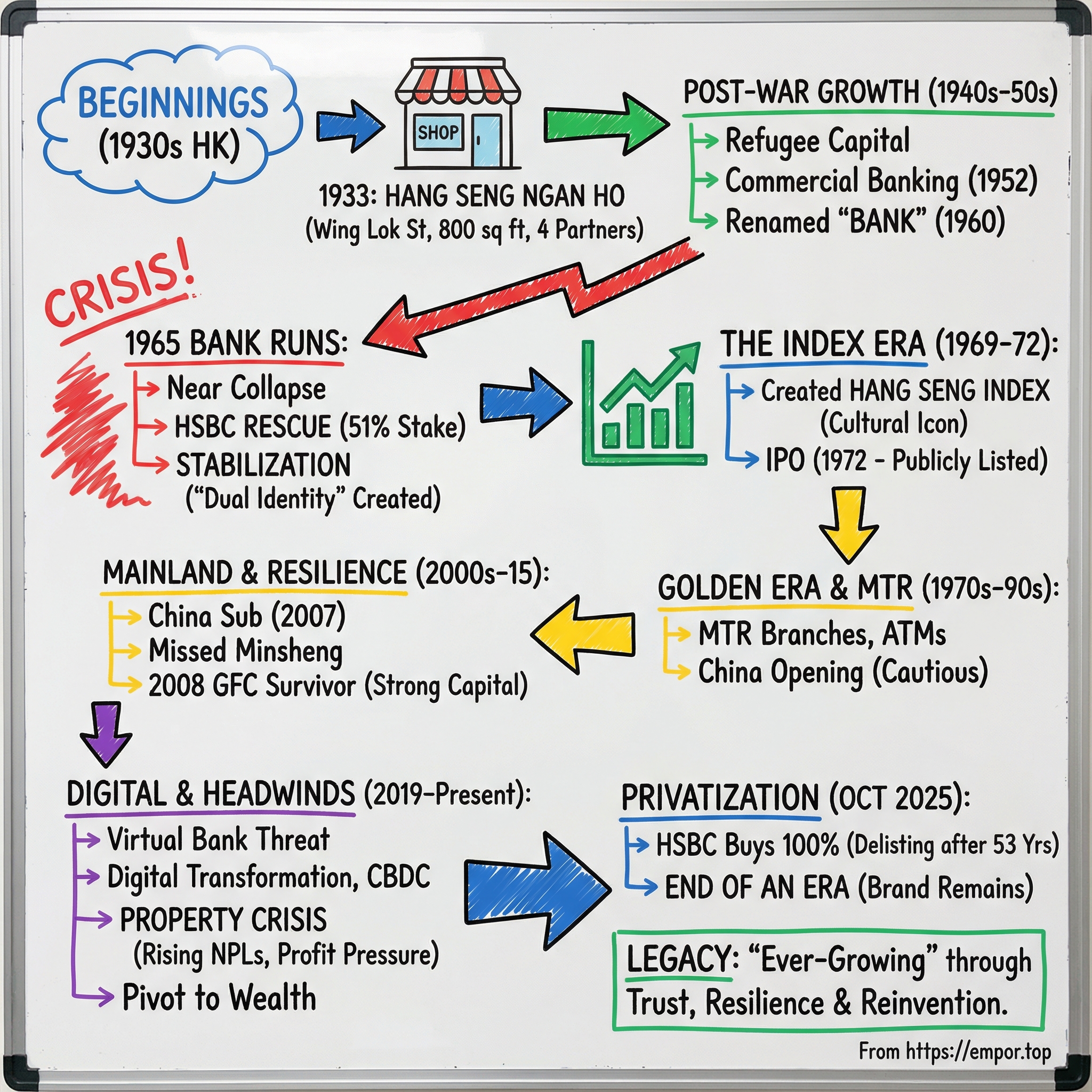

Hang Seng Bank: The Ever-Growing Bank That Defined Hong Kong

I. Introduction: A Tale of Two Eras

On the morning of October 9, 2025, newsrooms across Asia lit up with an announcement few people saw coming. HSBC Holdings plc said it would privatize Hang Seng Bank Limited through a scheme of arrangement, pulling the bank off the stock market and ending more than half a century as a publicly traded institution. Hang Seng’s Hong Kong-listed shares jumped 25.88% on the news, valuing the lender at more than HK$290 billion.

But this wasn’t just a corporate tidy-up. It felt like the final page of one of Asia’s great financial origin stories: a bank that started as an 800-square-foot money-changing shop in the Great Depression, then grew into a household name serving close to four million customers—and eventually became the name attached to the region’s most famous stock index.

Hang Seng was founded in 1933 and went on to build a reputation as Hong Kong’s leading domestic bank, known for staying close to the everyday needs of local businesses and households. Over time it also became inseparable from HSBC: a principal member of the HSBC Group, publicly listed but with HSBC Holdings owning about 63% of the shares. By this point, Hang Seng had amassed total assets of HK$1,822 billion—an “ever-growing” institution living up to its name.

So the question at the heart of this story is both straightforward and surprisingly emotional: how did a tiny four-partner operation in colonial Hong Kong become the namesake of Asia’s most famous stock index—and what does HSBC’s privatization mean for Hong Kong’s financial identity?

We’ll tell it in four movements: the early days on Wing Lok Street; the 1965 crisis that changed the bank’s fate; the moment Hang Seng became bigger than a balance sheet with the creation of a market benchmark; and the modern era of digital disruption and new headwinds—before returning to 2025, where Hang Seng prepares to leave public markets.

In many ways, this is the story of Hong Kong itself: resilience and reinvention, prosperity and panic, and the constant push-and-pull between local identity and global capital.

II. Hong Kong in the 1930s: Setting the Stage

To understand Hang Seng’s founding, you have to start with the peculiar chemistry of Hong Kong in the 1930s. This was a British colony on the edge of a vast and unstable China—small in size, but perfectly positioned as a gateway between East and West.

By the early twentieth century, Hong Kong had become a premier trading hub. Its deep natural harbor, predictable colonial rule, and strategic location made it a natural meeting point for goods, capital, and people moving in and out of China. Along with bales of cargo came something just as important: money, in every form. Gold and silver changed hands constantly. Foreign currencies circulated side-by-side. An entire street-level economy sprang up around exchange, bullion, and trade finance.

But the banking system didn’t serve everyone equally. The biggest institutions—mostly foreign, often British—sat at the top of the stack. They catered to large trading houses, shipping firms, and the colonial establishment. For small Chinese merchants, family businesses, craftsmen, and everyday savers, the experience was often simpler: you weren’t the customer these banks were built for.

That gap was the opening.

And it explains why money changing mattered so much. Before currencies standardized and modern retail banking became widespread, trade meant constant conversion—between Chinese taels, Mexican silver dollars, British pounds, and a mix of other coins and notes. A good money changer needed sharp instincts and deep credibility: knowing the day’s rates, judging the purity of precious metals, and earning trust from clients who could be handing over substantial sums.

In a city where global commerce was booming but local Chinese enterprise was still underserved, the opportunity was clear. This was a place where a small shop, run by people who understood the community and could move quickly, could grow into something much bigger.

And that’s exactly what four partners were about to try.

III. The Founding: Four Partners and 800 Square Feet (1933)

Hang Seng’s story begins on March 3, 1933—3/3/33. In Hong Kong’s local culture, that date landed with extra resonance. The Cantonese word for “three” rhymes with characters associated with life and growth, and the repeating threes suggested something like continuity: a business meant to keep expanding.

At the time, it wasn’t a “bank” in the modern sense. It was Hang Seng Ngan Ho, a money-changing business founded by four partners: Lam Bing-yim, Ho Sin-hang, Leung Chik-wai, and Sheng Chun-lin. They’d met in the late 1920s, and they brought complementary strengths. Lam and Sheng had already established banks in Shanghai. Ho and Leung came from Guangzhou’s gold and silver trade—exactly the kind of street-level financial muscle Hong Kong’s merchants relied on.

The name they chose was a mission statement. “Hang Seng” means “ever-growing” in Cantonese—an audacious promise for a firm starting in uncertain times.

The first premises were as modest as it gets: an 800-square-foot shop at 70 Wing Lok Street in Sheung Wan. The entire operation ran on a team of 11, counting everyone—the shopkeeper, street runners, gold traders, and apprentices. Not far away, the Hongkong and Shanghai Banking Corporation projected a different kind of banking power: grand buildings, thousands of employees, and the confidence of empire. Hang Seng was built for the people those institutions didn’t prioritize.

It started with only HK$100,000 in actual capital. Lam Bing-yim became the first chairman. Ho Sin-hang and Leung Chik-wai ran the place day-to-day as manager and deputy manager, while Sheng Chun-lin served as a director without an executive role.

From the beginning, the strategy was simple and hard to fake: outwork the competition, stay close to the customer, and learn fast. Hang Seng Ngan Ho operated six days a week, 9 a.m. to 5 p.m., serving small merchants and ordinary residents—exactly the segment foreign banks routinely neglected.

That focus paid off immediately. The business was profitable from the start, earning more than HK$10,000 in its first year. It was proof that the “gap” in Hong Kong banking wasn’t theoretical. It was real, and it was large.

Of the four founders, Ho Sin-hang became the bank’s most enduring figure. Born in 1900, he went on to serve as chairman and later became widely known as an entrepreneur, financier, philanthropist, and a defining presence in the institution’s culture. His own childhood poverty meant he received little formal education, which helped explain both his practical approach to business and why education became central to his charitable work.

Then history intervened. After the Second Sino-Japanese War broke out in 1937, Japanese occupation of Shanghai and Guangzhou reshaped trade and finance across the region. Hang Seng initially profited by facilitating foreign exchange needs tied to the Republic of China. But in December 1941, when Hong Kong fell to Japan, Hang Seng was forced to close. Ho moved to Macau—neutral under Portuguese rule—and continued operating there under the name Wing Wah Ngan Ho.

When Japan surrendered in 1945, Ho revived Hang Seng in Hong Kong. It emerged in the postwar years as a leader among Chinese-owned banks in the city—a survivor that had learned, early on, that “ever-growing” wasn’t just branding. It was a test. And Hang Seng had already passed the first one.

IV. From Money Changer to Commercial Bank (1940s–1960)

The years after World War II remade Hong Kong—and they remade Hang Seng right along with it. True to the meaning of its name, “ever-growing,” the firm steadily expanded beyond money changing into a wider set of banking services. The turning point came with events across the border. After the Chinese Revolution, Hong Kong became more than a port city; it became a financial refuge, increasingly separated from the Communist-controlled mainland and suddenly central to the flow of people and capital in the region.

In 1949, the Communist victory triggered a wave of capital flight into Hong Kong. Industrialists, merchants, and wealthy families arrived with money, connections, and urgency. The city’s population surged. Manufacturing accelerated. And the banking system—still dominated by foreign institutions that didn’t always prioritize ordinary Chinese customers—strained to keep up with demand.

Hang Seng was positioned perfectly for this moment. It had deep roots in the Chinese community, which made up the majority of Hong Kong, and that trust translated into recognition. By 1952, the business reincorporated as a private limited company and launched commercial banking operations. It registered a capital of HKD10 million, with HKD5 million paid up—formal structure catching up to what the market had already made true: Hang Seng was no longer just a street-level exchange shop. It was becoming a modern bank.

Leadership crystallized with the transition. Ho Sin-hang was appointed chairman, Leung Chik-wai vice chairman, and Ho Tim—one of the original 11 staff members from Wing Lok Street—became general manager. It was a signal of continuity as much as growth: the bank scaled up, but it did so with the same people and the same community-first instincts that built its early reputation.

By the late 1950s, Hang Seng’s total assets had risen to match—and in many cases surpass—older Chinese banks that had been around far longer. In 1960, the name finally caught up to what customers already called it: Hang Seng Ngan Ho was officially renamed Hang Seng Bank.

That same year, Hang Seng went public, though not yet on the Hong Kong Stock Exchange, and it ranked among the largest Chinese banks in the city. Under Ho Sin-hang’s leadership as founding chairman, the bank kept widening its offering and reach, cementing its shift from money changer to full-fledged commercial bank.

By the early 1960s, Hang Seng was the largest Chinese-owned bank in Hong Kong. In less than three decades, an 800-square-foot shop had turned into an institution with real weight in deposits, customers, and influence.

And with that prominence came a new kind of risk. Hong Kong’s banking sector was intensely competitive, even overcrowded, and the whole system was more fragile than it looked. Hang Seng was about to find out the hard way.

V. The 1965 Crisis: The Day That Changed Everything

The Hong Kong banking crisis of 1965 is one of those events that rewires an industry overnight. For Hang Seng, it was both a brush with disaster and the moment its future became permanently intertwined with HSBC.

The "Over-Banked" Problem

By the early 1960s, Hong Kong had what people at the time openly called an “over-banked” market. Too many institutions were chasing the same pool of deposits. Competition got ferocious, lending standards slipped, and the government’s hands-off approach meant light regulation and no deposit insurance. In a system built on confidence, that’s a dangerous setup: once rumors start, there’s nothing formal to stop fear from becoming a stampede.

The spark came in early February 1965 at Canton Trust and Commercial Bank. Heavy exposure to the property sector and fraud triggered runs at its Aberdeen and Yuen Long branches. The Hongkong and Shanghai Banking Corporation agreed to lend it HK$25 million, but it wasn’t enough. On February 8, Canton Trust collapsed into bankruptcy.

That failure didn’t stay contained. It set off a chain reaction of runs across other small and medium-sized banks in Hong Kong—especially the Chinese-owned institutions that served everyday depositors.

And there was recent memory, too. In 1961, a run on Liu Chong Hing Bank had dragged on for days until the Hongkong Bank and Chartered Bank stepped in. So when stress hit again in 1965—starting with Ming Tak Bank and then spreading—the public already knew what a bank run looked like, and how quickly it could turn real.

Chinese New Year made everything worse. It’s a season when people want cash. That year, withdrawals were heavier than usual. Two smaller banks, Ming Tak and Canton Trust & Commercial, couldn’t meet demand and shut their doors in the face of angry crowds. Once depositors see a locked bank door, they don’t ask questions first. They run to the next bank and demand their money.

Hang Seng's Near-Death Experience

Hang Seng didn’t cause the panic. But it couldn’t outrun it.

Even with conservative management and strong fundamentals, Hang Seng—then the largest local Chinese bank in Hong Kong—was swept up in the contagion. The scandal at Canton Trust helped ignite widespread depositor fear, and that fear landed on Hang Seng’s counters in force. Withdrawals surged, and by the peak on April 9, the run had drained nearly a quarter of the bank’s deposits.

Governor David Trench moved to contain the situation, imposing daily withdrawal limits of 100 dollars. It was a blunt instrument, but it bought time.

The emergency measures around the city showed just how close Hong Kong was to a full-blown cash crisis. The government ordered 5,000,000 British £1 notes to be flown in from the Bank of England by chartered jet. A temporary cash-withdrawal limit was set at $17.50 per day. Another £35 million in banknotes was scheduled to arrive from London. By the end of the week, the run began to subside.

But Hang Seng still needed something more powerful than limits and fresh banknotes. It needed restored trust.

The HSBC Rescue

That restoration came the only way it realistically could in 1965: a larger institution stepping in and putting its name—and its balance sheet—behind the bank. To stabilize Hang Seng and reassure depositors, The Hongkong and Shanghai Banking Corporation acquired a controlling 51% stake for HK$51 million, in a government-backed intervention carried out the same day. The immediate run effectively ended.

Hang Seng had, in practical terms, been sold to survive. The bank had lost almost a quarter of its reserves in the run. Over time, HSBC increased its ownership from that initial majority stake to almost 63 per cent.

The significance went far beyond a single rescue. HSBC was already the dominant force in Hong Kong banking. Now it controlled the territory’s largest Chinese bank, securing a leading position in the market. In the years that followed—through political disturbances and business uncertainty from 1966 to 1972—the group’s share of deposits (including Hang Seng) sat in the mid-forties.

And here’s the twist that mattered for Hong Kong’s identity: Hang Seng still felt Chinese. In 1967, during the sustained and violent anti-British campaign in Hong Kong and on the Mainland, the Hongkong Bank saw deposits fall sharply—down almost 14 per cent. Hang Seng, widely regarded as a Chinese institution, saw deposits rise by roughly the same amount.

That “dual identity”—local face, global backing—became an enduring advantage. Hang Seng gained the stability of HSBC while keeping the trust it had earned in the Chinese community.

By May 1965, confidence had returned. Out of Hong Kong’s 87 banks, only three ultimately failed that year.

Looking back, the lesson is as old as banking itself: fundamentals matter, but confidence matters more—because confidence can vanish in a day. For Hang Seng, the crisis proved how quickly panic can threaten even a well-run institution. For HSBC, the acquisition was both a rescue and a strategic masterstroke. And for Hong Kong, it marked the moment a local champion became part of a global empire—without losing the name that people lined up to trust.

VI. The Hang Seng Index: More Than a Bank (1969–1972)

If the 1965 crisis was Hang Seng’s near-death experience, what came next was its leap into something rarer: cultural infrastructure. In 1969, the bank created an institution that would outlast any single product cycle, branch footprint, or executive team.

It created the Hang Seng Index.

Hang Seng established the index as a public service, and it went on to become the primary indicator of the Hong Kong stock market—the shorthand the world uses to understand how Hong Kong is doing.

The idea came from the top. Ho Sin-hang wanted a “Dow Jones Industrial Average of Hong Kong,” a simple, credible way to track the colony’s most important listed companies. Working with Hang Seng Director Lee Quo-wei, he commissioned the bank’s head of research, Stanley Kwan, to build it. The result became the globally recognized benchmark for Hong Kong equities.

The genius here wasn’t technical; it was positional. By creating and maintaining the market’s scorecard, Hang Seng put itself at the center of Hong Kong’s financial story. When international investors talked about Hong Kong, they talked about the Hang Seng Index. When newspapers summed up Asian markets in a sentence, the HSI was the reference point. The bank’s name stopped being just a brand and became a synonym for Hong Kong’s economic pulse.

And the timing mattered. By the end of the decade, the index had helped confirm Hang Seng’s status as a major bank in the territory. It became the Hong Kong Stock Exchange’s primary market indicator, tracking the shares of the colony’s top 33 firms. Hang Seng itself joined the Hong Kong Stock Exchange in 1972, with an initial public offering that valued the bank at HK$2.8 billion.

That listing was the capstone to Hang Seng’s post-crisis reinvention. Just seven years after a run drained nearly a quarter of its reserves, Hang Seng was now a publicly traded blue chip—its name attached to the benchmark that measured Hong Kong’s market.

For decades to come, the Hang Seng Index would be the lens through which global capital read Hong Kong: rising, falling, and making headlines far beyond the city. And through it all, Hang Seng remained its steward—cementing brand value in the one way advertising can’t replicate: by becoming part of the system itself.

VII. The Golden Era: Building Hong Kong's Domestic Champion (1970s–1990s)

After the Hang Seng Index put the bank’s name on the nightly news, Hang Seng spent the next two decades doing something less flashy, but far more durable: it built itself into Hong Kong’s domestic champion.

This was the bank’s golden era—steady expansion, conservative management, and a deepening presence in everyday life as Hong Kong evolved into a world-class financial center.

Hang Seng earned a reputation as a cautious lender, and that caution became a competitive advantage through the 1980s. At the same time, it pushed hard into consumer retail banking—especially after it secured the franchise for Hong Kong’s Mass Transit Railway system. Starting in 1981, Hang Seng began opening branches inside MTR stations. By the end of the 1980s, it had built a network of around 150 branches across Hong Kong.

The MTR play was quietly brilliant. Hong Kong’s rail system became one of the most efficient in the world, moving huge numbers of people through the city every day. By placing branches where commuters already were, Hang Seng didn’t just add convenient locations—it earned daily visibility with the mass market. It became, in a very literal sense, part of the city’s routine. Hang Seng was also the only local bank to offer extensive branch services along MTR stations, and that accessibility helped it become a leader in convenient retail services, alongside the rollout of ATMs in the early 1980s. By decade’s end, the bank was serving more than one-third of Hong Kong’s population.

Then came a jolt from politics that turned into fuel for finance.

In 1984, the Sino-British Joint Declaration rewrote Hong Kong’s future. By promising the continuation of Hong Kong’s capitalist system and a high degree of autonomy after the 1997 handover, it eased the existential uncertainty that had weighed on markets, property, and capital flows. Investor confidence snapped back. The Hang Seng Index surged. And for Hang Seng the bank—so closely associated with the city’s economic health—it translated into stronger deposits and rising market value.

The agreement didn’t remove every fear, but it replaced a void with a framework. And in finance, a framework can be enough to restart the machine.

The China Opening

Hang Seng also began edging closer to the mainland—carefully, and on its own timeline. In 1985, it opened a representative office in Shenzhen. Ten years later, it opened its first branch in Guangzhou.

That slow, deliberate approach wasn’t hesitation. It was the bank’s DNA. While others rushed into China’s newly opening markets, Hang Seng focused on relationships, regulations, and learning the terrain before it fully committed.

Still, the bank’s China ambitions came with an asterisk: HSBC.

Throughout this era, the relationship with its majority owner remained both a stabilizer and a constraint. Analysts periodically questioned Hang Seng’s long-term room to maneuver, especially as HSBC’s own mainland ambitions grew. The structure created a built-in tension—how far could Hang Seng expand beyond Hong Kong without overlapping with its parent?

For the time being, both sides stuck with the arrangement. Hang Seng continued operating as an independently run, publicly listed Hong Kong bank under HSBC’s umbrella—one of the group’s only publicly listed subsidiaries. The dual identity that emerged after 1965 still held: local in face and franchise, global in backing.

And it worked—right up until the next era forced every bank in Hong Kong to rethink what “a branch network” even meant.

VIII. The China Opportunity and Challenge (2000s–2015)

The new millennium put Hang Seng in a familiar bind: the biggest growth opportunity in its backyard was on the other side of the border, but getting there meant navigating regulation, competition, and the complicated reality of being Hong Kong’s “local champion”… while also being part of HSBC.

It was both the chance of a generation and, at times, an exercise in frustration.

Building the Mainland Subsidiary

Hang Seng started laying groundwork early, and in steps. In 2002, it launched personal e-banking services in mainland China—an early signal that it wanted more than a symbolic presence. In 2003, it expanded regionally with a branch in Macau. And in 2006, it received authorization to prepare for something much bigger: setting up a dedicated mainland subsidiary.

That green light turned into reality on May 28, 2007, when the China Banking Regulatory Commission authorized the formation of Hang Seng Bank (China) Limited. Hang Seng established the entity as a wholly owned subsidiary—its own platform to operate in the mainland market under local rules, with local branches, rather than as an extension of the Hong Kong bank.

Over time, that foothold became a meaningful network: dozens of outlets spread across major cities including Beijing, Shanghai, Guangzhou, Shenzhen, and others—organized into a set of full branches supported by sub-branches.

The Minsheng Bank Disappointment

But Hang Seng’s most ambitious China move didn’t happen in 2007. It nearly happened in 2003.

That year, Hang Seng entered negotiations to buy an equity stake in Minsheng Bank, then the largest privately held bank in mainland China. It would have been a shortcut—instant scale, a stronger local franchise, and a seat at the table inside one of China’s most dynamic private institutions.

Instead, it became the decade’s big “what if.” The talks collapsed after the two sides reportedly couldn’t agree on how much management control Hang Seng would get as part of the deal. With no agreement, Hang Seng had to look elsewhere for its mainland entry—ultimately building it the slower way, through its own subsidiary and branch network.

In the background, some analysts speculated that HSBC’s own mainland ambitions didn’t help. HSBC was building in China too, and the reality of a parent-subsidiary relationship is that strategic overlap can become strategic friction.

Weathering the Global Financial Crisis

Then came 2008—and with it, the ultimate stress test for any bank’s culture.

During the global financial crisis, Hang Seng responded the way a conservative lender tends to respond: it reduced credit risk in its balance sheet management portfolio and strengthened capital reserves. It stayed compliant under Basel II, the post-1990s framework that pushed banks toward stronger risk management and capital discipline.

The result wasn’t that Hang Seng escaped the downturn entirely—few banks did—but that it came through without the kind of existential damage that hit institutions more exposed to complex securities and aggressive balance sheets. In the years after, those crisis-era decisions helped leave Hang Seng with a notably strong capital base, and by 2014 it was regarded as one of the strongest lenders globally.

In a decade defined by China’s rise and Wall Street’s collapse, Hang Seng’s story was consistent: it pushed into new territory, missed at least one giant shortcut, and still made it through the most punishing financial storm in a generation by sticking to the same cautious instincts that had kept it alive since 1965—and, really, since Wing Lok Street.

IX. Digital Disruption and Virtual Bank Threat (2019–Present)

By the late 2010s, Hang Seng had already survived bank runs, political shocks, and global financial crises. But the 2020s brought a different kind of threat—one that didn’t start with panic at the teller window, but with a phone in your hand.

This time, the challengers weren’t scrappy Chinese banks down the street. They were virtual banks: app-first, branchless, and designed for a generation that expected money to move as smoothly as messages.

The Virtual Banking Challenge

In 2019, Hong Kong’s regulators issued eight virtual banking licenses. Overnight, the city’s famously competitive banking market gained a new class of rivals that didn’t have to pay for prime retail locations, big branch staffs, or the heavy infrastructure of traditional banking.

The results were mixed—but impossible for incumbents to ignore. Profitability remained elusive. Nearly half a decade into operations, none of Hong Kong’s eight virtual banks had reached profitability, even as some narrowed losses and improved net interest income performance.

But they were still growing. By the end of 2023, virtual bank deposits climbed to HK$37.5 billion, up 23% year-on-year, with 2.2 million depositors. The pitch was simple and sticky: better deposit rates, fewer fees, and a mobile experience that felt native rather than retrofitted.

For Hang Seng, the danger wasn’t that virtual banks would suddenly take over the market. It was that they would reset customer expectations—and force everyone else to follow.

Hang Seng's Digital Response

Hang Seng didn’t treat digital as a side project. It treated it like defense of the franchise.

In July 2023, the bank unveiled its “Future Banking” service concept at a new branch in Festival Walk, launching three “first-in-market” service and operation solutions aimed at reinventing what a modern branch could be in an app-driven world.

The investment followed. In 2023, Hang Seng put about HKD 1.2 billion into technology, including digital platforms and AI integration. By 2024, the bank expected roughly half of its transactions to be conducted digitally. And among Commercial Banking customers, digital behavior was already dominant: by the end of 2024, 92% of their transactions were completed through digital channels.

The message was clear: Hang Seng intended to compete on convenience, not just legacy.

COVID-19 Acceleration

Then COVID hit—and turned “digital transformation” from strategy into necessity.

From 2020 to 2022, remote banking usage surged as customers avoided physical branches. Hang Seng responded by rolling out Smart@Digital Banking in 2020, designed to make the shift easier with onboarding guides and upgraded investment tools. In many ways, the pandemic did what years of internal change management couldn’t: it rewired customer habits at scale.

CBDC Innovation

Hang Seng also pushed into what might become the next layer of financial infrastructure: central bank digital currencies.

When the Hong Kong Monetary Authority launched Phase 1 of its e-HKD pilot program in May 2023, Hang Seng was among sixteen participants. The bank developed three use cases—government grant disbursement, a merchant reward program, and peer-to-peer transfers—to explore how a hypothetical e-HKD could enable programmable payments and smart contracts.

All of this underscored the tightrope traditional banks now walk: stay relevant to younger, digital-first customers without abandoning the physical presence and relationships that still matter deeply to older and wealthier clients.

Hang Seng’s answer was not to pick one world over the other, but to try to win both—building digital muscle while keeping a very real footprint in the city it had served for generations.

X. The Hong Kong Property Crisis and Recent Headwinds (2021–2025)

For all the noise about fintech and virtual banks, the biggest stress test of Hang Seng’s modern era came from something far older and far more local: property.

Hong Kong real estate isn’t just another sector. It’s the backbone of household wealth, a major driver of business confidence, and a recurring theme in bank balance sheets across the city. When that engine sputters, every lender feels it. Hang Seng, as one of the largest locally incorporated banks, felt it first and felt it hard.

The Property Market Collapse

From their peak in 2021, Hong Kong property prices fell by nearly 30%. Higher mortgage rates squeezed affordability. Demand softened as some expatriates left the city. And a slower economy took the air out of both residential optimism and commercial rents.

The downturn didn’t come and go. It lingered. Prices kept sliding in 2023 and again in 2024, extending what began as a correction into a prolonged slump.

This is the backdrop for the 2025 privatization announcement: worsening real estate loan conditions in Hong Kong, following that broad decline across both residential and commercial property. The same market that had underwritten decades of stability was now the source of the most uncomfortable questions.

Financial Impact

The impact showed up where it always does in banking: credit costs.

In the first half of 2025, profit attributable to shareholders fell 30% to HK$6,880 million, and earnings per share dropped 34% to HK$3.34. At the same time, updates to models used for expected credit loss calculations reflected a deteriorating picture: the non-performing loan ratio rose to 6.69% as of 30 June 2025, up from 6.12% at the end of 2024 and 5.32% a year earlier.

Against a backdrop of ongoing uncertainty—trade-tariff threats, sustained high interest rates, and a prolonged downturn in commercial property—Hang Seng increased provisions. Expected credit losses came in at HK$4,861 million, and gross impaired loans and advances stood at HK$55 billion as of 30 June 2025.

And yet, even with profit and returns pressured by elevated credit costs, Hang Seng’s balance sheet still carried the hallmark of its culture: resilience. As of 30 June 2025, its CET1 ratio was 21.3%, with a Tier 1 capital ratio of 23.3% and total capital ratio of 24.9%. Liquidity was also strong, with a liquidity coverage ratio of 311%, comfortably above the statutory requirement.

Strategic Pivots

Rather than simply pull back, Hang Seng moved faster on a shift that had been building for years: reduce reliance on property-linked lending and grow businesses that generate fees and deepen cross-border relationships.

One clear focus was mainland customer growth. After launching an express account-opening journey for mainland customers, new account openings by mainlanders rose 81% year-on-year.

At the same time, the bank leaned harder into wealth. With stronger market sentiment and upgraded products and services, wealth management income grew 20% year-on-year, including a sharp acceleration in the second half of 2024 versus the prior year’s second half. Deposits also increased by 9% compared with the year before.

And where the risk was most sensitive, the direction was unambiguous: continued reduction. By year-end 2024, mainland China commercial real estate exposure had been cut to around 2% of the total loan book.

Taken together, the response tells a simple story. As property stopped being an easy tailwind, Hang Seng pushed toward wealth management and cross-border services—toward a model less dependent on rising collateral values and more dependent on relationships, advice, and flows. It’s a meaningful evolution in what “Hang Seng” is, and what it needs to be, in a Hong Kong where the property market no longer guarantees calm.

XI. The Privatization: End of an Era (October 2025)

On October 9, 2025, HSBC announced what had seemed unthinkable: it would privatize Hang Seng Bank. After more than half a century as a public company, Hang Seng was set to leave the Hong Kong Stock Exchange—an unexpected move framed as a simplification of HSBC’s structure at a moment when Hong Kong real estate loans were worsening.

The proposal offered HK$155 in cash for each share, pitched as a substantial premium to where the stock had been trading and to prevailing analyst targets. With HSBC already owning around 63% of Hang Seng, the deal pegged the total transaction value at roughly HK$106 billion. In a market that hasn’t seen many mega-deals lately, it was poised to be one of Hong Kong’s largest M&A transactions in a decade.

The Rationale

HSBC’s argument was straightforward: full ownership would make Hang Seng easier to manage—especially in a tougher credit environment.

“The benefit of HSBC as a 100 per cent shareholder is it gives Hang Seng Bank even more flexibility to manage its capital and its ratios more efficiently [under] the umbrella of HSBC,” group CEO Georges Elhedery said at a media roundtable in Hong Kong.

HSBC said privatization would help it capitalize on growth opportunities in Hong Kong by more tightly aligning the HSBC Asia Pacific and Hang Seng franchises. Elhedery described the move as “an investment for growth” in a home market HSBC knows well, aimed at creating “greater alignment” while still “respecting the heritage and customer proposition of Hang Seng Bank.”

Importantly, HSBC emphasized what it wasn’t changing: Hang Seng would keep its separate brand. The message was that this was about structure and flexibility, not erasing one of Hong Kong’s most recognizable financial names.

Market and Analyst Response

Analysts quickly pointed to a long-running structural issue. “Parent-subsidiary double listings are inherently problematic in terms of governance and in this sense it’s a positive and long-overdue move,” said Michael Makdad, a senior analyst at Morningstar.

Markets reacted immediately. Hang Seng’s shares jumped about 30% on the announcement. HSBC’s shares fell 6% in London trading, as investors digested the near-term hit to HSBC’s capital ratio. HSBC said it planned to rebuild that buffer by pausing share buybacks for three quarters.

What Comes Next

The proposal still needed approvals: Hang Seng shareholder approval and the High Court of Hong Kong’s sanction of the scheme. If those were secured, the transaction was expected to become effective on January 26, 2026, with Hang Seng’s listing scheduled to be withdrawn the next day.

HSBC and HSBC Asia Pacific also issued a formal “no price increase” statement, confirming HK$155 per share was final—no sweeteners later, no revised bid.

And that’s what made this feel like more than a deal. For 53 years, minority shareholders owned a piece of Hang Seng—through crises and booms, property cycles and technological change. Privatization didn’t just end a listing. It ended public participation in one of Hong Kong’s signature institutions, folding the city’s “ever-growing” bank completely into HSBC.

XII. Bull Case, Bear Case, and Investment Framework

With privatization pending, the point here isn’t to pick a side on the deal. It’s to pull out what Hang Seng’s arc teaches you about banking franchises in Hong Kong: what endures, what breaks, and what you actually watch when the headlines fade.

The Bull Case for Hong Kong Banking

Hang Seng’s history is a case study in the compounding power of trust. Even after HSBC took control in 1965, Hang Seng kept a distinct identity that mattered in Hong Kong’s Chinese community. That local legitimacy still shows up in results: the bank reported a 75% jump in new-to-bank affluent customers and a 15% rise in the overall number of affluent customers.

Then there’s the Greater Bay Area. Cross-border wealth flows are one of the few growth narratives in the region that doesn’t depend on Hong Kong property rebounding. With nine cross-boundary Wealth Management Centres and new account openings by mainland customers up 81% year-on-year, Hang Seng is positioning itself as a bridge for customers who want Hong Kong products, Hong Kong regulation, and Hong Kong currency—without being treated like a purely foreign bank.

Finally, there’s resilience. A CET1 ratio above 21% gives Hang Seng room to absorb further property weakness and still fund the investments it needs to stay competitive, especially on digital and wealth.

The Bear Case

The biggest risk is the simplest: property is still the center of gravity in Hong Kong, and the stress is already visible. A non-performing loan ratio of 6.69% reflects a market that hasn’t finished resetting. And if Hong Kong property remains below its 2021 peak for the rest of the decade, the drag isn’t just credit costs—it’s sentiment, collateral values, and deal flow.

Then there’s the HSBC factor. The relationship has always been both protection and constraint. HSBC backing stabilized Hang Seng in every crisis since 1965, but it also limited how far Hang Seng could independently expand on the mainland without stepping on its parent’s strategy. As a wholly owned subsidiary, Hang Seng could face even more pressure to coordinate with HSBC in China rather than compete or differentiate aggressively.

And digital pressure isn’t going away. Virtual banks may still be unprofitable, but they are scaling, and they’ve forced incumbents to change behavior. Aggregate operating income across all virtual banks rose sharply from FY2021 to FY2023, and even if the unit economics never fully work, they’ve permanently reset customer expectations around fees, rates, and service quality.

Porter's Five Forces Analysis

Threat of New Entrants: Moderate. Virtual bank licenses brought in new competitors, but regulatory scrutiny, funding requirements, and capital needs make banking hard to enter and harder to scale. Incumbents still have an edge in distribution and relationships.

Bargaining Power of Buyers: Rising. Customers now have more choices and more transparency, which has pushed banks to cut fees and compete harder on deposit rates. At the high end, affluent and private banking clients have meaningful negotiating leverage.

Bargaining Power of Suppliers: Low. Banks fund themselves largely through deposits and wholesale markets, where pricing is competitive and generally not dominated by any single “supplier.”

Threat of Substitutes: Growing. Fintech products, virtual banks, and non-bank wealth managers give consumers alternative paths for payments, borrowing, and investing.

Industry Rivalry: High. Hong Kong remains intensely competitive, with 151 licensed banks serving a population of 7 million.

Hamilton Helmer's 7 Powers Framework

Hang Seng’s advantages look different through Helmer’s lens—less about a single moat, more about a stack of reinforcing strengths:

Brand: Strong. “Hang Seng” isn’t just a bank name; it’s also the name of the market’s benchmark index. That association creates trust and credibility that’s hard to buy, and it supports premium positioning in wealth.

Network Effects: Limited. Banking doesn’t naturally produce platform-style network effects, though Hang Seng’s long-standing MTR station presence creates a practical convenience advantage.

Counter-Positioning: Real. “Local bank with global backing” differentiates Hang Seng from foreign banks that can feel distant, and from local peers that can’t match HSBC’s balance-sheet strength.

Switching Costs: Moderate. Retail relationships are still sticky, but digital onboarding has reduced friction. Mortgages and long-term credit relationships create more durable lock-in.

Scale Economies: Present, but not decisive. Scale helps fund technology and compliance, but virtual banks have shown that a smaller footprint can still deliver a compelling customer experience.

Cornered Resource: Meaningful. The MTR franchise is a unique distribution advantage, and stewardship of the Hang Seng Index is an irreplaceable brand asset.

Process Power: Strong. Hang Seng’s conservative credit culture—built through decades of cycles and shocks—is an internal capability that tends to show its value precisely when the market turns.

Key Performance Indicators to Monitor

For anyone evaluating Hong Kong banks, Hang Seng’s recent trajectory highlights two KPIs that cut through the noise:

-

Non-Interest Income as Percentage of Revenue: A proxy for how successfully a bank is diversifying away from property-linked lending and spread income. Hang Seng’s non-interest income grew 26% in 2024, reaching 31.6% of total revenue. The more a bank can earn from wealth, insurance, and fees, the less hostage it is to the next property swing.

-

Non-Performing Loan Ratio: The clearest real-time read on credit stress. At 6.69% as of June 2025, it captures how deep the property downturn is biting. Watching where this goes—and how well loans are covered by collateral—often tells you more about the franchise than a single period’s profit number.

XIII. Conclusion: The Ever-Growing Legacy

The story of Hang Seng Bank is, in many ways, the story of Hong Kong itself. Born in the turbulence of the 1930s, tested by war and revolution, pulled back from the edge in 1965, and then transformed into an icon of Asian finance, Hang Seng’s trajectory has always tracked the city that built it.

At its best, Hang Seng’s advantage was never complicated: it stayed close to ordinary people and local businesses, and it kept earning trust the slow way. That’s what took it from a cramped shop on Wing Lok Street to one of Hong Kong’s most recognized financial brands, serving close to four million customers.

The 1965 crisis exposed the oldest rule in banking: a bank can be well-run and still fail if confidence breaks. HSBC’s rescue preserved Hang Seng’s franchise while permanently changing its ownership—an arrangement that stabilized Hang Seng for decades, even as it raised the quiet question of how “local” a local champion can be when its majority owner sits elsewhere.

Then came the move that made Hang Seng bigger than a bank. The Hang Seng Index wasn’t a new product line; it was a claim on a position in the system. By becoming the keeper of Hong Kong’s market scorecard, Hang Seng made its name inseparable from the city’s economic pulse in a way no ad campaign could ever replicate.

And in the modern era, the reinvention continued. The delivery model shifted from street counters and branch queues to apps and digital flows. The banking relationship moved from being anchored by place to being anchored by experience. Yet the objective stayed recognizable: remain useful, remain trusted, and keep up with how customers actually live.

Now comes privatization. After 53 years as a publicly traded company, Hang Seng is set to return to private ownership—this time not as an independent Chinese money changer, but as a wholly owned part of HSBC. The brand remains. The listing doesn’t.

What stays constant is the name itself: Hang Seng, “ever-growing.” Through panics and booms, local identity and foreign ownership, physical branches and digital platforms, the bank largely lived up to the ambition its founders embedded in two words. Whether it continues to do so under full HSBC ownership is the next chapter—one that won’t be written by speeches or press releases, but by how the institution behaves the next time Hong Kong gets tested.

For Hong Kong, this deal is symbolic as much as it is financial. The city remains one of Asia’s great banking centers. But it’s also a reminder of the direction of travel: consolidation into global groups, with local names enduring more often as subsidiaries than as independent actors.

The four partners who opened Hang Seng in 1933 couldn’t have imagined what their small operation would become. They built something that could survive. Their successors built something that could define an era. And soon, the publicly traded Hang Seng that investors owned for half a century will disappear into its parent—another ending, and another beginning, in Hong Kong’s ever-changing financial story.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube