New Hope Liuhe: The Architecture of China's Protein Giants

I. Introduction: The Scale of the "King of Feed"

Picture a single grain of corn. Now picture twenty-eight million metric tons of them, mixed with soybean meal, fishmeal, vitamins, and trace minerals, then compressed into pellets and trucked to roughly two hundred thousand farms scattered across the rice paddies of Sichuan, the loess plateaus of Shaanxi, the duck ponds of the Mekong Delta, and the chicken sheds of Jakarta. That, in 2023, was a single year of output for a company most Western investors have never heard of.

In that same year, New Hope Liuhe processed and sold roughly seventeen million hogs, slaughtered nearly a billion ducks and chickens combined, and quietly supplied the marinated beef that ended up in the hotpot bowls of Haidilao. If you have eaten dinner anywhere in mainland China over the past decade, the odds are uncomfortably high that some part of your meal was once metabolized through a New Hope production line.

This is the invisible infrastructure beneath the dinner tables of 1.4 billion people. And the company behind it, listed on the Shenzhen Stock Exchange under the ticker 000876, is not run by some faceless state-owned enterprise or a Politburo-connected oligarch. It is run by a forty-five-year-old woman named Liu Chang, who took the chair in 2013 from her father, Liu Yonghao, the patriarch of a family that began this entire empire in 1982 with one thousand renminbi, four brothers, and a lot of quail eggs.

The thesis of today's deep dive is this. New Hope Liuhe is the most instructive case study in modern Chinese agribusiness because it answers a question that almost no other company has been forced to answer at this scale. How do you take a high-frequency, low-margin, commodity feed business, generationally compounded over four decades, and rebuild it into a vertically integrated animal protein platform without imploding under the weight of the most violent commodity cycle on earth, the Chinese hog cycle?

The roadmap. We will begin with the 1982 origin story, but we will move through it briskly because the more important inflection happened in 2011, when the merger of New Hope Agribusiness and Shandong Liuhe Group created a feed colossus. We will then unpack what insiders inside the company refer to as the Hog Gamble of 2016, when management consciously decided to deploy tens of billions of yuan in capex and acquisitions to vertically integrate downstream into hog farming. We will examine the African Swine Fever shock of 2018 and 2019, the price collapse of 2021, and how those biological and financial cycles defined the company we see today. And we will spend significant time on the next chapter, the era of Liu Chang and President Zhang Minggui, the digital and food-branding transformation, and the hidden gems within the duck and central kitchen segments that almost no sell-side analyst writes about.

This is not a story about pigs. This is a story about how a family business built a platform.

II. Foundation: Quails, Feeds, and the 2011 Inflection

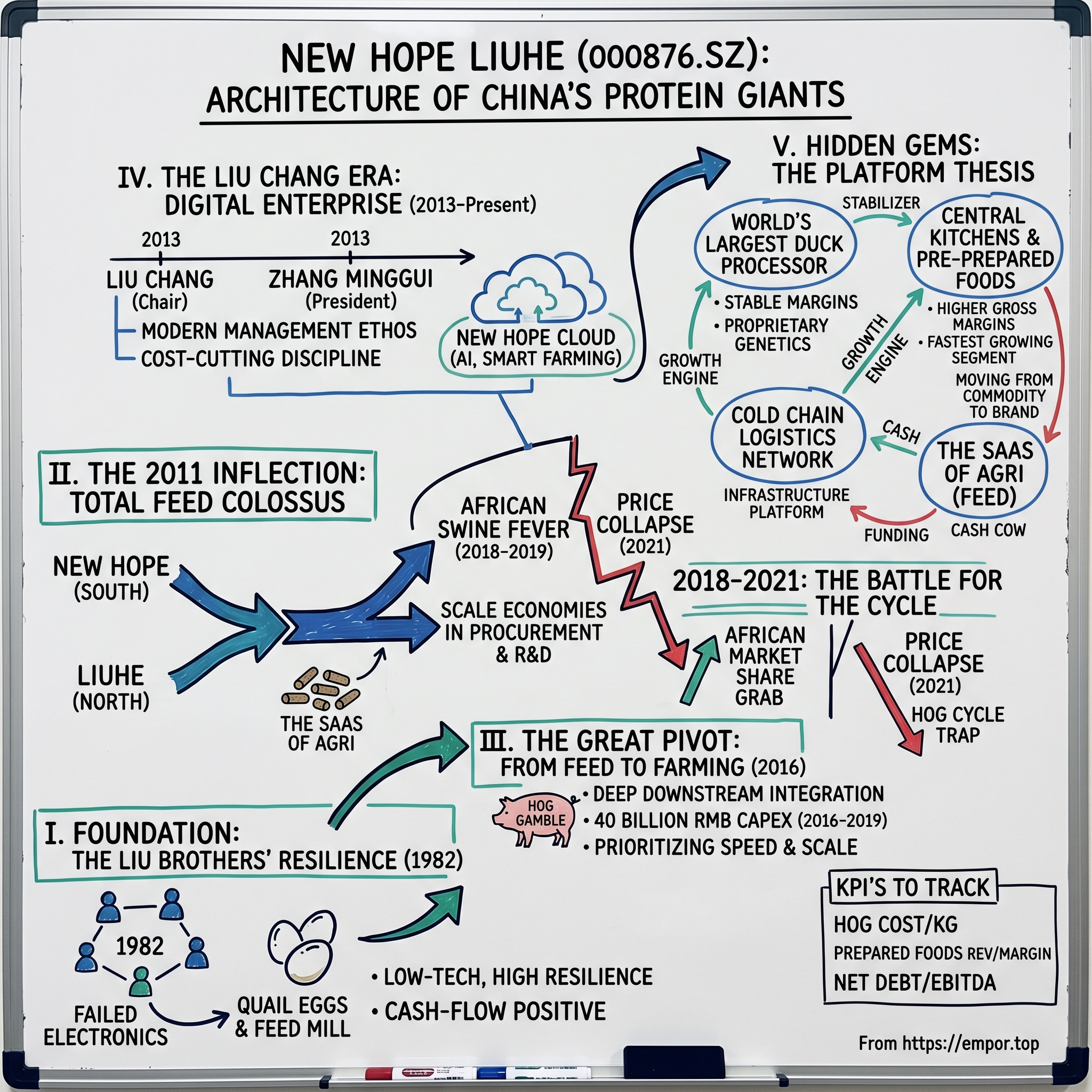

The Liu brothers did not set out to feed China. They set out, in 1982, to escape it.

The setting was Xinjin County, on the outskirts of Chengdu, in a Sichuan still recovering from the long shadow of the Cultural Revolution. The four Liu brothers, Liu Yongyan, Liu Yongxing, Liu Yongmei, and the youngest, Liu Yonghao, had been state employees, the eldest a teacher, the others engineers and technicians. They had stable iron rice bowl jobs, the kind of positions that Chinese families spent generations praying their children would obtain. And in 1982, encouraged by the early experiments of Deng Xiaoping's reforms, they walked away from those jobs to start a private business.

Their first attempt was an electronics venture, an audio equipment workshop. It failed almost immediately. They lacked components, lacked supply chains, and lacked the political connections required to import sensitive technology in the early 1980s. So they pivoted to what they could actually obtain. Quails. They pooled one thousand renminbi, roughly the equivalent of a few hundred US dollars at the time, sold their bicycles and watches to raise capital, and started raising quail in cages built from scrap wood.

The quail business was not glamorous, but it was a perfect first lesson. Quails reproduce quickly, eat little, and produce eggs that could be sold to local restaurants. Within five years, the brothers were the largest quail farmers in Sichuan, supplying roughly a quarter of the eggs consumed in Chengdu. But the real insight came not from selling eggs. It came from realizing that the bottleneck in animal husbandry was never the animal. It was the feed.

In 1986, the brothers built their first feed mill, a small operation producing pig feed under the brand Hope. They were directly competing with Charoen Pokphand, the Thai-Chinese conglomerate that dominated Chinese feed at the time. CP, as it was known, had government connections, foreign capital, and a head start of nearly a decade. The Liu brothers had none of those things. What they had was a willingness to price their feed roughly twenty percent below CP, to deliver to small farmers in remote villages CP would not serve, and to hand-train customers on how to use the formulas. By 1989, Hope feed was outselling CP across Sichuan.

This is the founding mythology, and it teaches the central lesson of the company. Low tech, high resilience. Animal feed is not a sexy business. It is a bulk commodity, sold at thin margins, requiring enormous logistics infrastructure and razor-thin operational discipline. But it is also a business that generates cash, every single day, with extreme stickiness. A farmer who switches feed brands risks the health of his entire flock. So once you win the customer, you keep them.

By 1995, the brothers had grown so large that they decided, amicably and famously, to split the company into four. Liu Yongyan took the eastern operations. Liu Yongxing took the central operations and would later build East Hope Group, a major aluminum and feed conglomerate. Liu Yongmei took the southern operations. And Liu Yonghao, the youngest and the most entrepreneurially restless, took New Hope, which would ultimately list on the Shenzhen exchange.

Fast forward to the moment that matters most for this story. June 2011. After more than a decade of running parallel operations and competing for the same farmers, New Hope Group merged its agribusiness operations with Shandong Liuhe Group, a Northern feed and poultry giant that the Liu family had been quietly accumulating stakes in since the early 2000s. Liuhe was the dominant player in duck and chicken integration across Shandong and Northern China. New Hope was dominant in pig feed and Southern markets. The combination, listed on the Shenzhen exchange under the ticker 000876, created in one stroke the largest feed producer in China and arguably the world.

Why did this matter? Because the merger was not just consolidation. It was the creation of what insiders called total feed. By owning pig feed in the south, poultry feed in the north, and aquaculture feed across the coastal provinces, New Hope Liuhe could amortize its raw material purchases, its R&D, and its branding across an unprecedented portfolio. Soybean meal bought for chickens in Shandong could substitute into pig feed in Sichuan when prices moved. Distribution trucks running half-empty on return trips could be used as backhaul for retail products. The merger was a textbook scale economy play.

Think of feed as the SaaS of agriculture. It is high-frequency, sticky, and cash-flow positive. A pig requires roughly three kilograms of feed for every kilogram of weight gained. Multiply that by the seven hundred million hogs slaughtered annually in China, and you have a market that, by some estimates, exceeds three hundred billion dollars in raw value. New Hope Liuhe captured a single-digit percentage of that market in 2011. It was a small slice of an enormous pie. But it was a slice that compounded, year after year, throwing off the cash that would fund the next, much riskier, chapter.

The implication for investors is that the feed business is the foundation. Everything else New Hope Liuhe has done, every acquisition, every farm built, every brand launched, has been funded by the predictable, boring, beautiful cash flows of selling pelletized soybean meal to small farmers. Lose sight of that, and you lose sight of the company.

III. The Great Pivot: From Feed to Farming

By 2016, the question facing New Hope Liuhe was no longer how to grow feed sales. It was what to do with the cash that the feed business kept generating. And the answer, in retrospect, was the single most consequential strategic decision in the company's modern history.

The setting is important. In the spring of 2016, Chinese pork prices were ripping higher. The previous two years had seen a brutal cull of small backyard farmers driven by environmental regulations under Xi Jinping's anti-pollution campaign, which had shut down hundreds of thousands of village-scale pig operations across the eastern provinces. Hog prices had nearly doubled in eighteen months. The country was, in the words of one Beijing analyst at the time, looking at a structural shortage of protein for the first time in a generation.

Into this environment, the New Hope board, with Liu Chang now firmly in the chair and a fresh management team in place, made a deliberate choice. Stop being just a feed company. Become a hog company too.

The economics of the pivot were defensible on paper. As a feed company, New Hope captured roughly five to seven percent gross margin on a kilogram of corn-and-soy pellets. As a hog producer, in a tight market, the gross margin per kilogram of live pig could exceed forty percent. The arithmetic was overwhelming, especially when management could point out that they already supplied the feed to most of the farmers they would now compete with. Why sell the picks and shovels when you could also dig the gold?

The execution was aggressive. Between 2016 and 2019, New Hope deployed what is conservatively estimated at over forty billion renminbi in capital expenditure and acquisitions in the swine segment. They acquired regional breeders. They built new farrow-to-finish operations across Shandong, Sichuan, and Hebei. They signed contract farming agreements with thousands of family operators, providing the feed, the piglets, and the technical support, and buying back the finished hogs at agreed prices. They went from raising under one million hogs in 2016 to raising over eight million by 2020 and over fourteen million by 2023.

But here is where the story gets interesting, and where the second-layer diligence becomes essential. Did they overpay?

Compare them to Muyuan Foods, the Henan-based pure-play hog operator that has become the gold standard of Chinese animal husbandry. Muyuan built its capacity slower, more methodically, more obsessively focused on a single integrated production model. Muyuan's cost per sow at the bottom of the cycle has consistently been lower than New Hope's, sometimes by as much as twenty percent. Why? Because Muyuan built from greenfield, controlled every variable, and obsessed over biological efficiency. New Hope, by contrast, bought speed. They acquired existing operations, inherited legacy infrastructure, and prioritized scale over per-unit cost.

Was that the wrong choice? In the short term, when pork prices stayed elevated through 2019 and 2020 due to the African Swine Fever epidemic, the answer looked like a clear no. New Hope's hog segment generated record profits. Revenue from the swine business alone exceeded forty billion renminbi in 2020. The market rewarded them. The stock price more than doubled.

Then came 2021. Hog prices collapsed. From a peak of nearly forty renminbi per kilogram in late 2019, prices fell to under twelve renminbi per kilogram by mid-2021. New Hope's hog segment swung from massively profitable to massively loss-making, almost overnight. The company posted its first annual loss in over a decade. Net debt, which had ballooned from under twenty billion renminbi to over eighty billion through the expansion years, became a serious concern. Credit rating agencies put the company on watch.

This is the hog cycle trap. It is not unique to New Hope. Every integrated Chinese pork producer has experienced it. The cycle, driven by the biological lag between when farmers see prices rise and when they can actually bring more pigs to market, runs roughly four years peak to trough. New Hope simply happened to be at maximum capital deployment when the cycle turned.

What is interesting, and instructive, is how they navigated the African Swine Fever era between those two extremes. ASF arrived in China in August 2018 and within eighteen months had killed roughly forty percent of the national pig herd. For most farmers, this was an existential catastrophe. For New Hope, with the capital to invest in biosecurity, AI-monitored farms, and rigid quarantine protocols, it was a market-share grab. While backyard farmers were wiped out, New Hope kept producing. Their share of the Chinese hog market more than doubled in three years. The biological crisis became a structural opportunity.

The lesson is that vertical integration is a double-edged sword in cyclical industries. It captures more of the value chain when prices are high. It absorbs more of the pain when prices collapse. New Hope, in 2026, is still living through the consequences of the 2016 pivot, both the good and the bad.

What this means for the long-term holder is straightforward. The hog segment is the volatility engine of the entire company. The feed segment funds the lights. But the company's stock will continue to trade on the hog cycle for the foreseeable future, no matter what management does in food, in poultry, or in central kitchens.

IV. The Liu Chang Era: From Family Business to Modern Enterprise

If you were going to design, in a laboratory, the perfect heir to a Chinese family conglomerate, you would probably end up with someone who looks remarkably like Liu Chang.

She was born in 1980, the only child of Liu Yonghao and Li Wei. She grew up in Chengdu watching her father build New Hope from a single feed mill into a national champion. She went to the University of International Business and Economics in Beijing for her undergraduate degree, then earned an MBA from MIT Sloan, and worked briefly at consulting firms before joining the family business in her mid-twenties. By 2011, at the age of thirty-one, she was on the board. By March 2013, when she formally became chair of the listed entity, she was thirty-three years old, making her one of the youngest chairs of any major company on the Shenzhen exchange.

The transition was not without controversy. Liu Yonghao remained the figure that bankers, regulators, and provincial officials wanted to meet with. He was, and remains in 2026, one of the most prominent private entrepreneurs in China, a member of various national consultative bodies, and a man whose personal brand was inseparable from the company's. Handing the chair to his daughter, in a country where family succession in private enterprise was still relatively new and culturally complicated, was a bet on continuity.

What Liu Chang brought to the role was something her father never quite had. A professional management ethos. Where Liu Yonghao had run New Hope on the basis of personal relationships, regional intuition, and decades of village-level knowledge, Liu Chang ran it on the basis of metrics, incentive systems, and digital transformation. She brought in McKinsey. She brought in Deloitte. She built a corporate strategy office. She introduced the kind of management dashboards that would have been familiar to any S&P 500 CEO but were genuinely novel in Chinese agribusiness in the early 2010s.

The most important hire of her tenure was probably Zhang Minggui, who became president in 2020. Zhang is not a flashy figure. He spent years inside New Hope's real estate arm, an arm that the family group used to monetize land holdings across China during the great property boom. When the real estate cycle turned, Liu Chang pulled Zhang into the agri-business with a specific mandate. Stabilize. Cut costs. Restore discipline.

Zhang's background in real estate matters more than it might appear. Real estate in China is a discipline of leverage management, cash flow forecasting, and ruthless project-by-project economic analysis. Those are exactly the skills that an over-leveraged hog producer in a down cycle desperately needs. Under Zhang's operational leadership, the company has spent the past three years deleveraging, divesting non-core assets, including the sale of select feed mills in less strategic regions, and obsessively driving down the cost per kilogram of pork produced. The results, while not yet matching Muyuan, have shown clear sequential improvement.

The shareholding structure tells you a lot about who actually controls this enterprise. New Hope Group, the family holding company controlled by Liu Yonghao and Liu Chang, owns approximately fifty percent of the listed entity through various subsidiaries and concert party arrangements. Liu Chang's personal direct stake is meaningful but not dominant. The remainder is distributed among institutional investors, including significant positions held by social security funds and several QFII-licensed foreign institutional holders. The family, in other words, retains absolute control. There is no realistic activist scenario for this stock.

What is more interesting is the incentive structure. Over the past three years, New Hope has rolled out multiple employee stock ownership plans. The vesting conditions are notable. Earlier ESOPs in the company's history were tied primarily to revenue and volume growth. The most recent vintages, post-2022, are tied explicitly to cost-per-kilogram reduction targets in the swine segment, to gross margin expansion in the food segment, and to free cash flow generation at the consolidated level. This is a meaningful shift. The message to senior management is unambiguous. Volume growth, on its own, is no longer rewarded. Profitable growth is.

The cultural shift, from family business to digital enterprise, is most visible in the operational technology stack. New Hope farms today are equipped with sensor networks that monitor pig weight, ambient temperature, ammonia levels, and feed consumption in real time. AI models, trained on years of internal data, optimize feed formulations based on commodity prices, animal age, and target market specifications. The company runs what is internally called the New Hope Cloud, which connects every farm, every feed mill, and every slaughterhouse in a single data plane. For a sense of the scale, the company has publicly stated that its smart farming platform manages over a hundred thousand sensors across its operations.

For investors, the importance of this generational transition is that it gives the company a real shot at re-rating. Family-run Chinese conglomerates have historically traded at deep discounts to their professional peers due to perceived governance opacity and key-person risk. New Hope under Liu Chang and Zhang Minggui is making a credible case that it is a different kind of beast. Whether the market eventually agrees is the central question of the bull case, which we will return to at the end.

V. Hidden Gems: The Duck Empire and the Central Kitchen Bet

Walk into any well-stocked supermarket in Shanghai, Guangzhou, or Beijing, head to the frozen section, and you will find a dizzying variety of pre-marinated dishes. Salt-baked chicken in vacuum bags. Pre-cooked beef brisket in aromatic broth. Cubed pork belly in soy and ginger marinade. Hotpot soup bases in concentrated paste form. Many of these products do not carry the New Hope brand. Some carry the Meihao brand, which is one of the company's premium lines. Many carry private label names belonging to retail chains. And a quietly enormous number of them are produced by, or contain inputs from, New Hope Liuhe.

This is the first hidden gem. The duck empire.

Through its Liuhe heritage, New Hope is the world's largest duck processor. Not in China. In the world. The company processes well over six hundred million ducks per year across its integrated operations, which span breeder farms, hatcheries, contract grow-out farms, slaughterhouses, processing plants, and distribution. To put that number in perspective, total global duck production is somewhere between three and four billion birds annually, depending on whose statistics you trust. New Hope Liuhe is somewhere between fifteen and twenty percent of the global supply.

Why does this matter? Because while the world fixates on Chinese pork, the duck and poultry segment quietly throws off some of the most stable margins in the entire company. Duck production is less cyclical than pork. The biological cycle is faster, roughly forty days from chick to slaughter weight versus six months for pigs, which means oversupply corrections happen quickly and prices stabilize. Demand for duck is concentrated in restaurants and processed food channels, which gives the company more pricing power than it has in commodity hog sales.

The duck business is also where New Hope's cornered resource advantage is most visible. Through decades of selective breeding, the company maintains its own proprietary duck genetics, lines that are optimized for feed conversion, meat-to-bone ratio, and disease resistance. These genetics are not licensed to competitors. They are a quiet moat, the kind of intangible asset that does not appear on the balance sheet but represents tens of years of accumulated R&D.

The second hidden gem, and arguably the more interesting one for the next decade, is pre-prepared foods, what the company calls central kitchens.

The thesis here is straightforward. China's restaurant industry, valued in the trillions of renminbi, is undergoing a structural shift toward chain restaurants, and chain restaurants increasingly want standardized, pre-prepared inputs. Haidilao does not slice its own beef. Meituan-listed chains do not marinate their own chicken. They buy pre-prepared inputs from suppliers who can deliver consistent quality, food safety certification, and cold chain logistics at national scale.

There are very few companies in China with the integrated capability to do this. New Hope is one of them. They own the protein. They own the processing. They own the cold chain. And critically, through Liu Chang's strategic prioritization, they have spent the past five years investing in the central kitchen infrastructure that turns raw protein into ready-to-cook, ready-to-heat, and ready-to-eat products.

The growth rate in this segment has been remarkable. Pre-prepared food revenue has compounded at over twenty percent annually for the past three years. While it remains a small slice of total revenue, somewhere between five and ten percent depending on how you classify intermediate processed products, it is the fastest-growing segment in the company. And critically, it carries higher gross margins than commodity pork, often in the high teens to low twenties versus mid-single-digits for raw hog sales.

The strategic implication is that New Hope is attempting to do something that almost no Chinese agribusiness has successfully done before. Move from a commodity business model to a brand-and-value-added business model without losing the cost advantages of vertical integration. The closest analog in Western markets is probably Tyson Foods, which has spent decades trying to balance its commodity chicken business with branded prepared foods like Jimmy Dean and Hillshire Farm. Tyson has had mixed success. New Hope is trying to do the same thing in a much faster-moving market, with less developed brand infrastructure, and against incumbent FMCG giants who are themselves trying to enter prepared foods.

The third quietly important asset is the cold chain logistics network. New Hope has built, over the past decade, one of the most extensive temperature-controlled distribution networks in Chinese agriculture. This network was originally built to serve internal needs, moving frozen pork and chicken from production facilities to processing plants and distributors. But increasingly, it is being externalized as a service offered to third parties. This is a classic Bezos-style move. Build infrastructure for internal use, let it scale, then open it up as a platform business with attractive marginal economics.

For investors, the implication is that New Hope today is not a single business but a portfolio. The feed segment generates approximately half of revenue and is the cash cow. The hog segment generates roughly twenty to twenty-five percent and is the volatility engine. The poultry and duck segment generates around fifteen percent and is the silent stabilizer. The food and prepared meals segment is the smallest at five to ten percent but is the most strategically interesting because it is where the future re-rating story lives.

If the company succeeds in shifting its revenue mix decisively toward prepared foods over the next five years, the entire equity story changes. We will return to this in the bull case. But first, we need to look at the competitive landscape and the analytical frameworks that explain why New Hope is built the way it is.

VI. Framework Analysis: 7 Powers and 5 Forces

Hamilton Helmer, in his book on competitive strategy, distinguishes between seven discrete sources of durable competitive advantage. Most companies, even great ones, have at most one or two. The interesting feature of New Hope Liuhe is that it has at least three identifiable powers, layered on top of each other in ways that compound.

The first and most obvious is scale economies. With twenty-eight million tons of annual feed production, New Hope is one of the three or four largest single buyers of soybean meal and corn in the world. When the company sends a procurement team to Brazil to negotiate a soybean cargo shipment, that team is buying at scales that smaller competitors simply cannot match. The result is a structural cost advantage of, by various estimates, two to four percent on raw material inputs versus the second-tier feed producers. In a business with single-digit margins, that cost advantage is the difference between profit and loss.

But the scale advantage extends beyond procurement. It also applies to R&D. New Hope's nutrition research labs, located in Chengdu and Qingdao, develop hundreds of feed formulations annually, optimized for specific animal species, growth stages, regional climates, and customer requirements. The R&D spend, while modest in absolute terms, is amortized across volumes that make it deeply economic on a per-unit basis. A small competitor cannot match this. They lack the volume to justify the investment.

The second power is cornered resource. We have already discussed the proprietary duck genetics. The same logic applies, to a slightly lesser degree, to the company's pig genetics program, which has been built up through decades of selective breeding combined with selective imports of Western breeding stock from Denmark and Canada. The chicken breeding program, integrated through the Liuhe heritage, similarly relies on proprietary lines. These genetic resources are not patentable in the traditional sense, but they are extraordinarily difficult to replicate, requiring decades of consistent investment.

The third power is what Helmer calls counter-positioning, and it is the most subtle. New Hope's feed-to-food integration allows it to absorb cyclical shocks in ways that pure-play competitors cannot. When pork prices collapse, New Hope's hog segment loses money. But the feed segment, selling to third-party farmers who are also losing money but still need to feed their animals, often sees stable or even increasing demand. The poultry segment, with its faster cycle, can pivot quickly. And the food segment, selling pre-prepared products at relatively stable prices, becomes increasingly profitable as input costs fall.

This is structural diversification that a pure-play hog operator like Muyuan cannot replicate without abandoning its focus. And it is structural diversification that a pure-play feed operator like Twins Group cannot replicate without taking on enormous capital commitments. New Hope sits in the middle, captures cycle volatility on the upside, and dampens it on the downside.

There are also powers New Hope does not have. The company does not have meaningful network effects. It does not have proprietary process power in the way that, say, Toyota Production System gives Toyota an advantage. It does not have brand power at the consumer level, although it is trying to build it through the Meihao premium line and other initiatives. And it does not have switching costs in the traditional sense, although the operational integration with farmers does create meaningful stickiness.

Now turn to Porter's five forces. The picture here is mixed.

The threat of new entrants is moderate to low in feed, primarily because of the capital intensity and the entrenched distribution networks of incumbents. It is much higher in central kitchens and prepared foods, where capital requirements are lower and where local players, regional FMCG companies, and even restaurant chains themselves can vertically backward-integrate. New Hope's defense in this segment is its protein supply integration, but the moat is not absolute.

The bargaining power of suppliers is significant for global commodities. Chinese feed producers are largely price takers in international soybean and corn markets, which are dominated by ABCD majors, Archer Daniels Midland, Bunge, Cargill, and Louis Dreyfus. New Hope cannot dictate prices. What it can do, and increasingly does, is hedge intelligently and forward-buy strategically. The company's commodity hedging desk, while not publicly disclosed in detail, is reportedly one of the more sophisticated in Chinese agribusiness.

The bargaining power of buyers varies dramatically by segment. In feed, buyers are highly fragmented small farmers with little individual leverage. New Hope has pricing power. In hogs sold to slaughterhouses, buyers are more concentrated, especially the major processors like WH Group, and pricing power shifts. In prepared foods sold to grocery chains, buyer power is high. Walmart China, Sun Art Retail, and JD Fresh are sophisticated negotiators who push margins relentlessly.

The threat of substitutes is interesting. In the long term, the substitution risk for animal protein is plant-based protein, which has gained some traction globally but remains a tiny fraction of Chinese consumption. Cultivated meat is even further away from commercial scale. In the near term, the substitution dynamic is between proteins themselves, between pork, chicken, beef, duck, and fish. New Hope's portfolio diversification across protein types provides natural hedging here.

The intensity of rivalry is the most dramatic force. The Big Four of Chinese pork, Muyuan, Wens Foodstuff Group, New Hope, and Twins Group, compete viciously on cost. Muyuan is widely considered the cost leader in pure hog production. Wens has the most extensive contract farming network. Twins has deep regional roots in Sichuan and the southwest. New Hope has the most diversified portfolio and the deepest feed business. None of these companies has been able to durably out-compete the others. The market structure is oligopolistic, but with intense competition on cost and capacity.

The takeaway from the framework analysis is that New Hope Liuhe is not the most powerful player in any single segment of Chinese agribusiness. Muyuan has lower hog costs. CP Group has stronger international distribution. WH Group has stronger downstream brand assets. But New Hope is the only player that has meaningful positions across all the relevant segments simultaneously, which is what makes the platform thesis credible.

VII. The Playbook: Business and Investing Lessons

The story of New Hope Liuhe contains, embedded within it, several lessons that apply far beyond Chinese agriculture. This section unpacks them.

The first lesson is the asset-heavy versus asset-light tradeoff. For most of its history, New Hope was an asset-light business. Feed mills require capital, but they are nothing compared to the capex of owning farms, breeding stock, slaughterhouses, and cold chain logistics. The company's return on equity, in the asset-light era, regularly exceeded twenty percent. Cash flow conversion was excellent. Working capital cycles were short. It was, in many ways, an ideal business.

The decision to vertically integrate into hogs flipped that profile. Suddenly, return on equity became dependent on hog cycle pricing. In good years, ROE could spike above thirty percent. In bad years, like 2021 and 2022, it could turn deeply negative. Capital expenditure went from a few billion renminbi annually to over twenty billion renminbi at the peak. The balance sheet bloated. Net debt to EBITDA, which had historically run under one turn, expanded to over three turns at the bottom of the cycle.

Was this the right call? The honest answer is that the verdict depends on what happens over the next five years. If New Hope can use its integrated platform to drive a successful transition into branded prepared foods, the asset-heavy investment will be vindicated. If it cannot, and the company remains primarily a commodity producer, then the ROE compression of the integrated era will look like a strategic mistake.

The lesson for investors is that vertical integration is always a bet on terminal value, not a bet on intermediate returns. The companies that get vertical integration right, like the early Apple of the 2000s or the Tesla of the 2010s, do so because the integration unlocks new categories of value creation. The companies that get it wrong end up with bloated balance sheets and mediocre returns on capital.

The second lesson is vertical integration as risk management in fragmented markets. Chinese agriculture, in 2026, remains far more fragmented than its American or European counterparts. There are hundreds of thousands of small pig farmers, tens of thousands of feed mills, and a long tail of slaughterhouses and processors. In a fragmented industry, the player that controls the most vertical layers has structural informational advantages. They see demand signals earlier. They can shift product mix faster. They can enforce biosecurity standards across the chain in ways that pure-play operators cannot.

This is why being a system, in Helmer's terminology, is better than being a part in Chinese agribusiness. The system player can dampen cyclical shocks. The part player has to absorb them.

The third lesson, perhaps the most universal, is succession planning. Liu Yonghao did something that very few Chinese family business founders have managed to do well. He genuinely transferred operational and strategic control to the next generation. Liu Chang is not a figurehead. She is not a daughter who shows up for ribbon cuttings while her father runs the business from behind. She is the chair, the strategic architect, and the public face of the company.

The mechanics of how this happened are worth understanding. Liu Chang did not parachute in. She spent over a decade learning the business in operational and board roles before taking the chair. She brought in professional management, including Zhang Minggui, who has no family ties to the Liu family but has decades of New Hope tenure. She maintained continuity with the founder's vision while introducing new strategic priorities. And critically, she has taken visible accountability for the down cycle of 2021 and 2022, including overseeing painful cost-cutting and restructuring decisions.

For any investor evaluating a family-controlled business, the question of succession is existential. New Hope offers a relatively rare positive case study. Whether that translates into superior long-term returns will depend on Liu Chang's ability to navigate the next decade, but the structural foundations look more durable than most.

The fourth lesson, embedded in the entire arc, is the importance of timing within commodity cycles. Almost every major strategic decision New Hope has made has been timed against the hog cycle. The 2016 expansion was made into a tightening market. The 2020 capacity additions were made into peak prices. The 2022 cost-cutting was forced by collapsing prices. Management did not always get the timing right. The 2020 expansion, in particular, looks in retrospect like classic late-cycle behavior. But the company has demonstrated, repeatedly, an ability to read the cycle better than most peers and to position accordingly.

For investors, the practical implication is that New Hope's stock is best understood as a function of two variables. First, where we are in the hog cycle. Second, what progress the company is making on the structural transition to branded foods. The first variable is largely beyond management's control. The second is entirely within it.

VIII. The Bear and Bull Cases

We close, as is the convention, with the two opposing views.

The bear case for New Hope Liuhe rests on three interconnected concerns.

The first is balance sheet. The 2016 to 2020 expansion left the company with substantially more debt than it carried in its asset-light era. While management has made meaningful progress on deleveraging since 2022, including divesting non-core assets and prioritizing free cash flow generation, net debt remains elevated relative to the company's pre-expansion baseline. In a high interest rate environment, or in a scenario where the next hog down cycle hits before the deleveraging is complete, the balance sheet could constrain strategic flexibility. Concentrated bank debt and bond maturities require careful management, and refinancing risk, while not acute, is not negligible.

The second is the persistent volatility of the Chinese hog market. Despite years of consolidation, the market remains structurally cyclical. The biological lag between price signals and supply response means that overshooting is endemic. New Hope, with seventeen million hogs annually, is now large enough that its own production decisions move the market. But the market also moves the company. A repeat of the 2021 price collapse would, even with improved cost discipline, generate substantial losses. The bear would argue that the cycle has not been tamed and will continue to whipsaw earnings.

The third is the slow pace of the strategic transition. Pre-prepared foods, the segment most likely to drive a re-rating, remains under ten percent of revenue. The duck and poultry segment, while stable, is not growing at rates that would meaningfully shift the company's overall profile. The bear case is that New Hope, despite its strategic ambitions, will remain primarily a commodity feed and hog company for the foreseeable future, with all the cyclical and valuation consequences that entails. In this view, the stock should continue to trade at the eight to ten times earnings multiple typical of Chinese agribusiness, with periodic dramatic swings driven by hog prices.

There are also second-layer concerns that thoughtful investors should track. Regulatory and ESG risk is non-trivial. Chinese environmental regulations on large-scale animal agriculture have been tightening over the past decade and will likely continue to tighten. Carbon emissions from livestock are a growing focus globally. Animal welfare standards, while still less stringent than European norms, are gradually rising in China. Each of these creates compliance costs and operational constraints. There is also the broader geopolitical context. New Hope sources a meaningful share of its soybean meal from imported beans, primarily from Brazil and to a lesser extent the United States. Any disruption to those trade flows, whether from US-China tensions or from Latin American supply shocks, would directly affect input costs.

The bull case rests on a different narrative.

The bull begins with the premise that the platform is fundamentally undervalued because it is being valued as a sum of commodity businesses rather than as a coherent strategic entity. If you applied Tyson Foods or WH Group multiples to the hog segment, Maple Leaf Foods multiples to the prepared foods segment, and Cargill-style multiples to the feed segment, the implied valuation would be meaningfully higher than where the stock currently trades. The market is not paying for the integration.

The bull then makes the case that the strategic transition, though slow, is real and accelerating. The pre-prepared foods segment is growing at over twenty percent annually. The cold chain network is increasingly being externalized as a service. The Meihao branded line is gaining shelf space in major retail channels. Each of these is a small lever individually, but together they shift the company's revenue mix toward higher margin and higher multiple businesses. If, over the next five years, prepared foods grow from under ten percent of revenue to, say, twenty-five percent of revenue, the company's blended margin profile and earnings stability would look very different. A re-rating from a farm multiple to something approaching a food and FMCG multiple would deliver substantial upside.

The bull also points to the cost reduction trajectory in the hog segment. While New Hope still trails Muyuan on per-kilogram costs, the gap has narrowed meaningfully under Zhang Minggui's operational discipline. Continued convergence toward best-in-class cost levels would substantially improve through-the-cycle returns even in the absence of any strategic mix shift. Combined with the elevated baseline of capacity that the expansion years built, the company is positioned to capture significant operating leverage on the next upcycle.

And the bull would emphasize the duck and poultry quiet asset. With genuine global leadership in duck processing, proprietary genetics, and stable margins, this segment alone could justify a meaningful portion of the company's enterprise value. It is the kind of asset that, if it were spun out, the market would likely value at a substantial premium to its current implicit valuation inside the conglomerate.

Pulling together both views, the framework that emerges is that New Hope Liuhe is best understood as an option on Chinese agricultural transformation. The downside is bounded by the cash-generative feed business and the platform's structural diversification. The upside is determined by execution on the prepared foods strategy and on cost convergence in hogs.

For long-term investors trying to track this story, three KPIs are the ones that actually matter.

First, cost per kilogram of hog produced. This is the single most important operational metric. It determines whether the company can compete with Muyuan over the cycle. It also determines through-cycle profitability. Track it quarterly, compare it to disclosed peers, and watch for the trajectory.

Second, prepared foods revenue growth and segment gross margin. This is the strategic metric. It determines whether the platform thesis is real. If revenue continues compounding at twenty percent or higher and gross margins expand toward FMCG levels, the bull case is unfolding. If growth decelerates and margins compress, the strategic transition is failing.

Third, net debt to EBITDA on a through-cycle basis. This is the survival metric. It determines whether the company has the balance sheet flexibility to invest in the strategic transition and to weather the next down cycle. Watch it trend over multiple quarters, normalize for hog price volatility, and stress test against scenarios.

Watch those three numbers, and you will understand New Hope Liuhe better than ninety-five percent of the analysts who cover it.

The myth versus reality contrast for this company is worth pausing on. The consensus narrative, especially among Western investors who notice the stock at all, is that New Hope is just another Chinese pork company, a bet on the hog cycle, exposed to all the risks of opaque governance and commodity volatility. The reality is more interesting. New Hope is a multi-generational family business that has navigated four decades of Chinese economic transformation, built genuine global leadership in multiple animal protein categories, and is in the middle of a strategic transition that, if successful, would represent one of the most significant business model evolutions in Chinese agribusiness history. Whether the transition succeeds is uncertain. But the bet is real, the management is credible, and the platform is genuinely differentiated.

New Hope Liuhe is not just a pig farmer. It is a platform for protein. Whether the market eventually agrees, and at what valuation, will be the central question for shareholders over the coming decade.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube