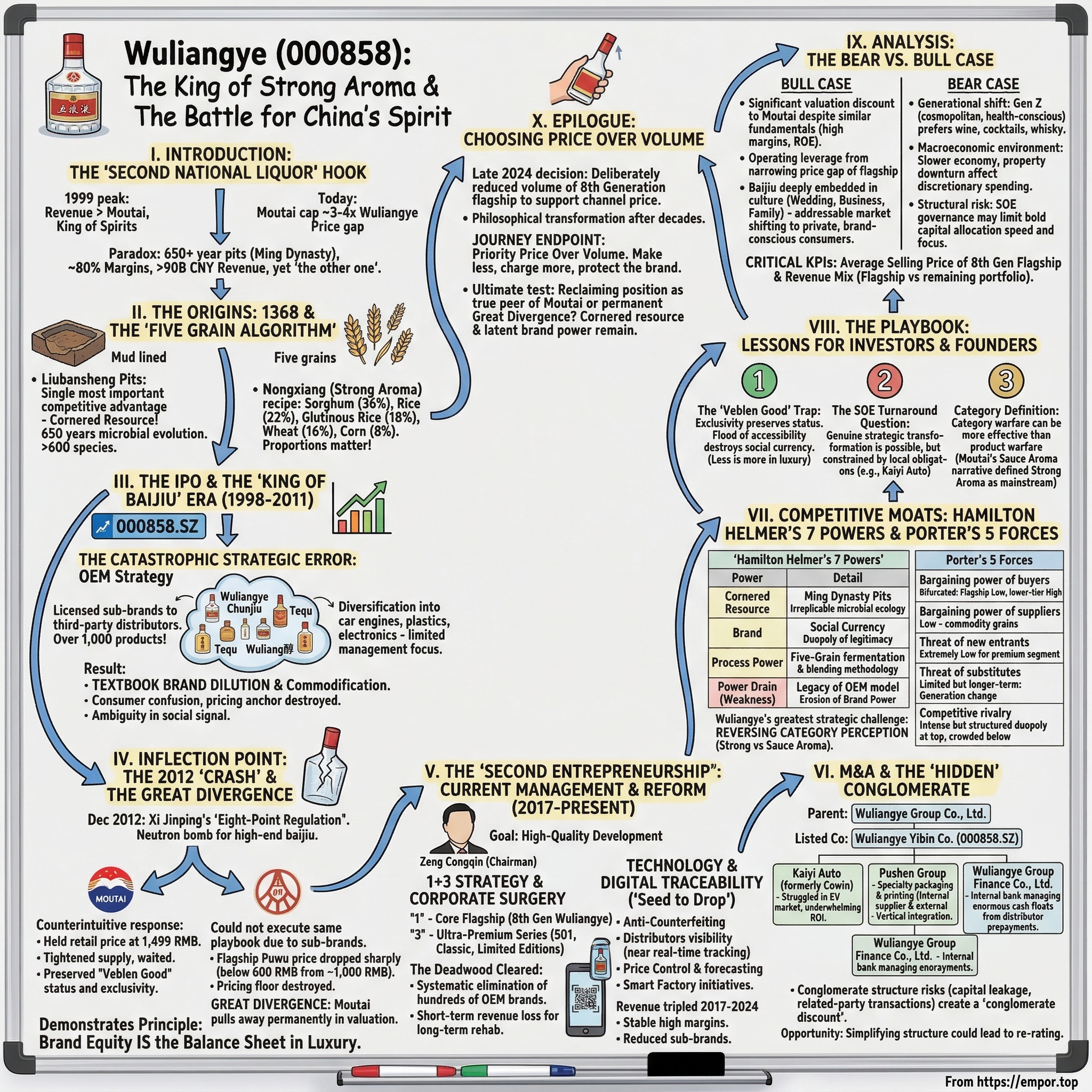

Wuliangye: The King of Strong Aroma and the Battle for China's Spirit

I. Introduction: The "Second National Liquor" Hook

In the winter of 1999, if you walked into any high-end banquet hall in Beijing, Shanghai, or Chengdu, the bottle at the center of the table was not Moutai. It was Wuliangye. The squat, crystal-clear bottle with its distinctive red-and-gold label was the undisputed king of Chinese spirits. Its revenue was higher than Moutai's. Its brand recognition was broader. Its distribution network reached further into the fabric of Chinese business culture. For a brief, glittering moment, Wuliangye sat atop the most lucrative consumer goods category in the world's most populous country.

Fast forward to today, and the picture has inverted almost completely. Kweichow Moutai commands a market capitalization roughly three to four times that of Wuliangye. Moutai's flagship bottle retails at 1,499 RMB and trades on the secondary market for significantly more. Wuliangye's 8th Generation flagship, despite being one of the finest spirits produced anywhere on earth, sells for roughly half that price. The gap is not about quality. It is about narrative, about brand architecture, and about a series of decisions made in boardrooms in Yibin, Sichuan, that nearly destroyed one of the oldest continuously operating consumer brands in human history.

Here is the paradox that makes Wuliangye one of the most fascinating business stories in Asia. This is a company with fermentation pits that have been in continuous use since the Ming Dynasty, a span of over 650 years. Its "Brand Strength" rating, as measured by international brand valuation firms, has consistently ranked among the highest of any spirit brand globally. Its gross margins hover near 80 percent, rivaling the finest luxury houses in Europe. Its annual revenue exceeds 90 billion CNY. And yet, it is perpetually described as "the other one." The Pepsi to Moutai's Coke. The AMD to Moutai's Intel. The eternal number two.

But that framing misses the real story. The real story is not about a company that lost. It is about a company that made a catastrophic strategic error in the early 2000s, watched its rival exploit that error to build an unassailable brand premium, survived a government-induced demand shock that nearly wiped out the entire high-end baijiu category, and is now, methodically and with considerable intelligence, engineering one of the most ambitious brand rehabilitations in modern consumer goods history.

The journey from the Ming Dynasty to the "OEM disaster" of the 2000s, through the 2012 anti-corruption "near-death experience," to the current digital-first "Second Entrepreneurship" is a masterclass in the fragility of brand equity, the power of cornered resources, and the question of whether a state-owned enterprise can truly reinvent itself. The themes are universal: brand dilution versus brand premium, the moat of "Strong Aroma" baijiu, and the transition from a state-owned factory to something that aspires to be a modern luxury conglomerate.

This is the story of how Wuliangye lost a throne and is trying to take it back.

II. The Origins: 1368 and the "Five Grain Algorithm"

To understand why Wuliangye matters, you need to understand something about dirt. Specifically, about what happens to dirt when you dig a rectangular pit, line it with mud, fill it with fermented grain, and then leave it alone for six centuries.

In 1368, during the early years of the Ming Dynasty, artisans in Yibin, a city nestled at the confluence of the Jinsha and Min rivers in southern Sichuan, dug a series of fermentation pits. These were not ordinary holes in the ground. They were carefully constructed vessels, lined with local clay, designed to hold a mash of grains as it slowly transformed into baijiu, the fiery clear spirit that has been the backbone of Chinese social, political, and commercial life for millennia. These pits, known as the "Liubansheng" pits, are still in use today.

This is not a quaint historical footnote. It is the single most important competitive advantage in the entire baijiu industry. Here is why: baijiu fermentation is not like wine fermentation or whiskey distillation. It is a solid-state process. The grains are mixed with water, yeast cakes called "qu," and the residue from previous fermentation cycles, then packed into these earthen pits where a staggeringly complex ecosystem of bacteria, yeasts, and fungi goes to work. Over time, the microbial community in a pit evolves. It becomes richer, more diverse, more capable of producing the complex esters and organic acids that define high-quality baijiu. The older the pit, the better the microbes. The better the microbes, the higher the quality of the spirit.

Think of it this way. If you wanted to compete with Wuliangye, you could hire their master distillers. You could source identical grains. You could replicate their water supply, their climate controls, their distillation equipment. But you could not replicate 650 years of microbial evolution. It would be like trying to build a coral reef from scratch. The biology simply does not work on human timescales. Scientists from the Chinese Academy of Sciences have studied the Yibin pit ecology extensively and identified over 600 distinct microbial species in the oldest pits, a biodiversity that younger pits, even those aged 50 or 100 years, cannot match. This is a cornered resource in the purest sense of the term, and no amount of venture capital, private equity, or government subsidy can replicate it.

But Wuliangye's founders did not just dig good pits. They also cracked a recipe that, in its own way, is as iconic and as closely guarded as any formula in the consumer goods world. Unlike Moutai, which uses pure sorghum, Wuliangye employs a blend of five grains in a specific ratio: sorghum at 36 percent, rice at 22 percent, glutinous rice at 18 percent, wheat at 16 percent, and corn at 8 percent. Each grain contributes something distinct to the final product. Sorghum provides the body and the characteristic "sauce" undertones. Rice adds sweetness and roundness. Glutinous rice contributes a silky mouthfeel. Wheat brings in aromatic complexity from the qu fermentation. Corn adds a subtle sweetness that balances the heat of the alcohol.

The result is what the Chinese spirits industry calls "Nongxiang," or "Strong Aroma." It is the most popular flavor profile in Chinese baijiu, accounting for roughly 70 percent of all baijiu consumed in China by volume. Moutai's "Jiangxiang," or "Sauce Aroma," is a different beast entirely, earthier, more pungent, an acquired taste that historically was regional to Guizhou province. For most of modern Chinese history, if you were drinking baijiu at a celebration, a business dinner, or a government banquet, you were drinking Strong Aroma. You were, in all likelihood, drinking Wuliangye.

The brand name itself has an origin story worth telling. For centuries, the spirit produced in Yibin was known as "Yaozixuequ," a name that roughly translates to "Yao's Cellar Brew," after the family that operated the most famous distillery. In 1909, a local scholar named Yang Huiquan attended a banquet where the spirit was served. Moved by the complexity of the five-grain blend, he suggested the name "Wuliangye," literally "Five-Grain Liquid." It was an act of branding genius, whether intentional or not. The name immediately communicated the product's unique differentiator, its multi-grain composition, in a market dominated by single-grain spirits. It stuck, and with it, a modern brand identity was born, one that would carry this spirit from a regional Sichuan specialty to the most recognized baijiu in China.

What investors should take from this origin story is not nostalgia. It is the recognition that Wuliangye's moat is geological and biological, not financial or technological. The pits are the product. The product is the pits. Everything else, the branding, the distribution, the pricing, is built on top of that irreplaceable foundation. And as we will see, the tragedy of Wuliangye's modern history is that management forgot this fundamental truth and nearly destroyed the brand that sat atop it.

III. The IPO and The "King of Baijiu" Era (1998-2011)

On April 27, 1998, Wuliangye Yibin Co., Ltd. began trading on the Shenzhen Stock Exchange under the ticker 000858. It was, at the time, the largest and most prestigious baijiu company to go public in China. Its revenue exceeded Moutai's. Its brand was more widely recognized. Its distribution network, built over decades of state-directed commerce and then expanded aggressively during China's early reform era, was the envy of the industry. If you had asked any analyst, any industry insider, any consumer in 1998 which baijiu company would dominate the 21st century, the answer would have been unanimous: Wuliangye.

The early years as a public company were triumphant. China's economy was accelerating. GDP growth rates were hitting 8, 9, 10 percent annually. A new class of entrepreneurs, government officials, and corporate executives was emerging, and they needed a social lubricant to seal deals, celebrate promotions, and navigate the intricate web of "guanxi," the relationship-based system that underpins Chinese business culture. High-end baijiu was not just a beverage. It was a signal. It communicated wealth, taste, and social standing. And Wuliangye was the default signal.

Revenue climbed steadily through the early 2000s. The stock performed well. The company was generating enormous cash flows from a product with minimal raw material costs and extraordinary pricing power. Everything was working. And then management made the decision that would haunt the company for the next two decades.

The decision was called the "OEM strategy," though "strategy" is perhaps too generous a word for what was, in practice, a short-term land grab. Under the leadership of the early 2000s management team, Wuliangye began licensing its brand name to third-party distributors, allowing them to create "sub-brands" that carried the Wuliangye name but were produced to lower specifications, sold at lower price points, and marketed to a broader audience. The logic was seductive. Why limit yourself to one premium bottle when you could have dozens of products at every price tier, each one paying a licensing fee back to the mothership?

The result was an explosion of products. At its peak, there were reportedly over a thousand "Wuliang-something" bottles on the Chinese market. Wuliangye Chunjiu. Wuliangye Tequ. Wuliang Chunliang. Wuliang醇. The naming conventions blurred. The quality varied wildly. Consumers could no longer tell the difference between the real flagship Wuliangye and the dozens of cheap imitations that shared its name and its logo. A bottle that looked almost identical to the premium product could be found for a fraction of the price, and the unspoken question at every banquet table became: "Is this the real one, or the cheap one?"

This is the textbook definition of brand dilution, and it is worth pausing to understand why it is so destructive, particularly in the luxury goods space. A luxury brand derives its value not from the intrinsic cost of its materials but from its scarcity, its exclusivity, and the social signal it sends. When you serve a bottle of Wuliangye at a business dinner, you are not paying for grain and water. You are paying for the message: "I value this relationship enough to spend a significant sum on this bottle." The moment that signal becomes ambiguous, the moment the recipient cannot be sure whether the bottle cost 800 RMB or 80 RMB, the social currency evaporates. And with it, the willingness to pay a premium.

Contrast this with what Moutai was doing during the same period. Kweichow Moutai, under a series of increasingly savvy management teams, took the opposite approach. They kept the product line narrow. They controlled distribution with an iron fist. They raised prices steadily, creating artificial scarcity. They understood, perhaps instinctively, perhaps through careful study of Western luxury brands like Hermès and Louis Vuitton, that in the luxury goods business, less is more. Every bottle of Moutai was Moutai. There was no ambiguity, no confusion, no cheap cousin on the shelf next to it.

While Wuliangye was flooding the market with sub-brands, Moutai was building a moat of exclusivity. The revenue growth looked similar on paper for a while, but the brand equity trajectories were diverging sharply. Wuliangye was selling volume. Moutai was selling status.

The other strategic misstep of this era was diversification. While Moutai stayed relentlessly focused on one thing, making and selling the finest Sauce Aroma baijiu in the world, Wuliangye's parent group began branching out into unrelated businesses. Car engines. Plastic packaging. Electronics. The logic, common among Chinese SOEs of that era, was that a large state-owned group should be a diversified industrial conglomerate, a "national champion" with fingers in many pies. The problem was that none of these businesses had the margins, the brand power, or the competitive position of the core baijiu operation. Every yuan of management attention and capital allocated to a car engine factory was a yuan not invested in protecting and enhancing the most valuable consumer brand in Sichuan province.

By 2011, Wuliangye was still enormously profitable. Revenue was growing. The stock was performing. But underneath the surface, the structural damage had been done. The brand had been stretched thin. The pricing power of the flagship had been undermined by the sea of sub-brands. And a storm was coming that would expose every crack in the foundation.

IV. Inflection Point: The 2012 "Crash" and The Great Divergence

In December 2012, the newly appointed General Secretary of the Chinese Communist Party, Xi Jinping, introduced what became known as the "Eight-Point Regulation." The rules were straightforward: no more extravagant government banquets, no more lavish gift-giving among officials, no more ostentatious displays of wealth by party cadres. On paper, it was an anti-corruption measure. In practice, it was a neutron bomb dropped on the high-end baijiu industry.

To understand why, you need to understand the composition of baijiu demand in 2012. By most industry estimates, somewhere between 30 and 50 percent of all high-end baijiu consumption in China was driven by what the industry euphemistically called "Three Public" spending: government banquets, military entertaining, and state-owned enterprise hospitality. These were not casual consumers picking up a bottle for a Friday night dinner party. These were institutional buyers purchasing cases at a time, often with public funds, often as a lubricant for the machinery of Chinese governance. When Xi Jinping said "stop," they stopped.

The impact on the industry was immediate and devastating. High-end baijiu prices collapsed. Inventories piled up. Distributors who had been hoarding bottles as speculative investments suddenly found themselves sitting on depreciating assets. The entire category went into a recession that would last the better part of three years.

But here is where the story diverges, and where the consequences of Wuliangye's OEM strategy became brutally apparent. Moutai's response to the crisis was counterintuitive and brilliant. They held their recommended retail price at 1,499 RMB per bottle. The actual transaction price in the market fell below that, sometimes significantly, but Moutai never officially cut the price. They absorbed the pain, tightened supply, and waited. Their bet was that the "Veblen Good" dynamics of their brand, the phenomenon where higher prices actually increase demand because the product functions as a status signal, would eventually reassert themselves. They were right. As the anti-corruption crackdown became the new normal and government-driven consumption declined permanently, a new source of demand emerged: wealthy private consumers who wanted Moutai precisely because it was expensive, because it was scarce, because serving it at a dinner said something about the host.

Wuliangye could not execute the same playbook. The problem was those thousands of sub-brands. When a consumer walked into a liquor store and saw "Wuliangye" on a 100 RMB bottle next to the "real" Wuliangye at 700 RMB, the pricing anchor was destroyed. The flagship could not sustain a premium price when the brand name itself had been commodified. The price of the 52-degree Puwu, the core Wuliangye product, dropped sharply, at one point falling below 600 RMB from its pre-crackdown highs near 1,000 RMB. The discount to Moutai widened from negligible to enormous.

This period, roughly 2013 to 2016, was the moment of "Great Divergence." Moutai's market capitalization began pulling away from Wuliangye's, and it never looked back. By the time the baijiu market stabilized and began recovering, Moutai had established itself as the undisputed luxury standard. The question "Moutai or Wuliangye?" had been answered by the market: Moutai for the most important occasions, Wuliangye for everything else. It was a devastating demotion for a company that had been number one just fifteen years earlier.

The financial impact was severe but not fatal. Wuliangye's revenue declined, margins compressed, and the stock underperformed. But the company never came close to actual financial distress. The underlying business, selling baijiu from 650-year-old pits, was still enormously profitable even at reduced prices. The damage was to the brand, to the positioning, to the intangible but enormously valuable perception that Wuliangye was the best. That damage would take far longer to repair than any balance sheet impairment.

What makes this chapter so instructive for investors is the speed and permanence of the divergence. In 2011, Wuliangye and Moutai were rough peers. By 2016, Moutai was worth multiples of Wuliangye. The gap was not driven by fundamentals in the traditional sense, both companies had similar margins, similar return on equity profiles, similar cash generation characteristics. The gap was entirely about brand perception and pricing power. It was a real-time demonstration of a principle that luxury goods investors know well but that the broader market often underappreciates: in the luxury business, brand equity is not just a line item on the balance sheet. It is the balance sheet.

V. The "Second Entrepreneurship": Current Management and Reform (2017-Present)

In May 2017, Zeng Congqin was appointed Chairman of Wuliangye Yibin Co., Ltd. To understand what happened next, you need to understand the man. Zeng was not parachuted in from Beijing. He was not a finance professional or a management consultant. He was a Sichuan local, born and raised in Yibin, the city that Wuliangye built and that, in many ways, Wuliangye is. He had spent his career in Yibin's economic planning apparatus, rising through the ranks of local government before moving into the corporate structure of the Wuliangye Group. He understood the company not as an abstract portfolio holding but as the economic engine of his hometown, the single largest employer, the single largest taxpayer, the institution around which the entire social and commercial life of Yibin revolved.

This mattered because it shaped his incentive structure in ways that are fundamentally different from a Silicon Valley CEO or even a typical Western corporate executive. Zeng's "win condition" was not a stock price target or a bonus payout. It was what the Chinese system calls "High-Quality Development," a phrase that encompasses sustainable growth, social stability, tax revenue generation, and the prestige of the institution within the national hierarchy. His job was to make Wuliangye great again, not in a flashy, disruptive way, but in a methodical, systematic, deeply Chinese way.

And that is exactly what he did. The centerpiece of Zeng's reform agenda was what the company called the "1+3" strategy, and it began with an act of corporate surgery that was as painful as it was necessary. The "1" referred to the core flagship product, the 8th Generation Wuliangye, the 52-degree, 500ml bottle that was the spiritual and commercial heart of the brand. Everything else was subordinate to this. The "3" referred to three ultra-premium series designed to compete at the very top of the market: the 501 Wuliangye, the Classic Wuliangye, and other limited-edition releases targeting the 3,000 to 5,000+ RMB per bottle segment.

But before the "1+3" could work, the deadwood had to be cleared. And there was a lot of deadwood. Zeng and his team embarked on a systematic elimination of the sub-brand ecosystem that had been choking the flagship for nearly two decades. Hundreds of OEM brands were terminated. Licensing agreements were not renewed. Distributors who had grown comfortable selling cheap Wuliangye-branded products found their contracts revoked. The process was neither quick nor painless. Each terminated brand represented a revenue stream, a distributor relationship, a local business that depended on the Wuliangye name. But Zeng held firm. The short-term revenue loss was the price of long-term brand rehabilitation.

The results, viewed from today, have been meaningful. The number of sub-brands has been reduced from over a thousand to a manageable portfolio. The flagship 8th Generation Wuliangye has been re-established as the clear anchor of the brand, with a recommended retail price that has been steadily guided upward, narrowing the gap with Moutai. Revenue has grown from approximately 30 billion CNY in 2017 to over 90 billion CNY by 2024, a tripling driven not by volume expansion but by mix improvement and pricing discipline. The company's gross margin has stabilized in the high 70s to low 80s percent range, reflecting the shift toward higher-priced products.

The other pillar of the "Second Entrepreneurship" was technology, and specifically, the construction of a comprehensive digital traceability system. This was a direct response to one of the most pernicious legacies of the OEM era: counterfeiting. When there were a thousand legitimate Wuliangye-branded products on the market, it was nearly impossible for consumers to distinguish real from fake. Counterfeit bottles were rampant, and every fake bottle that made someone sick or simply tasted bad was a direct assault on the brand.

Wuliangye's solution was to build what it calls a "seed to drop" traceability platform. Every bottle of the flagship product now carries a unique digital identifier that can be scanned by a consumer's smartphone. The scan returns the bottle's complete provenance: which pit the grain was fermented in, which batch it came from, when it was distilled, when it was bottled, and the entire chain of custody from the factory to the retail shelf. The system uses a combination of QR codes, NFC chips, and blockchain-based record keeping. It is, by the standards of the global spirits industry, one of the most sophisticated anti-counterfeiting systems ever deployed.

But the traceability system serves a dual purpose beyond consumer protection. It also gives Wuliangye unprecedented visibility into its distribution channel. In the old model, the company shipped bottles to distributors and had limited visibility into where those bottles ended up, at what price they were sold, and how long they sat in inventory. The digital system changes this. Wuliangye can now track the velocity of every bottle through the channel in near real-time, enabling far more precise demand forecasting, inventory management, and price control. This is critical because price control, maintaining the "floor price" of the flagship, is the single most important operational priority for the company's brand rehabilitation strategy.

The "Smart Factory" initiative, which complements the digital supply chain, has modernized the physical production process as well. Wuliangye has invested heavily in automating portions of the blending and bottling process, installing environmental monitoring systems in the fermentation workshops, and building new storage facilities for aged base wine. The fermentation itself, the magic that happens in those Ming Dynasty pits, remains stubbornly manual and traditional. You cannot automate 650 years of microbial wisdom. But everything around the fermentation, from quality control to packaging to logistics, has been brought into the 21st century.

For investors watching this transformation, the key question is whether the "Second Entrepreneurship" is working. The evidence is mixed but encouraging. Revenue and profit growth have been strong. The price gap with Moutai, while still significant, has narrowed. The sub-brand problem has been largely addressed. The digital infrastructure is in place. But the ultimate test, whether Wuliangye can reclaim its position as a true peer of Moutai in the minds of China's wealthiest consumers, remains unresolved. Brand rehabilitation is measured in decades, not quarters.

VI. M&A and The "Hidden" Conglomerate

There is a version of the Wuliangye story that lives entirely within the baijiu business: the pits, the grains, the bottles, the banquets. But if you look at the parent entity, Wuliangye Group Co., Ltd., a different and more complicated picture emerges. The listed company, Wuliangye Yibin Co. (000858.SZ), is the crown jewel of a sprawling state-owned conglomerate that has fingers in businesses ranging from automobile manufacturing to financial services to industrial packaging. Understanding this broader structure is essential because it shapes the capital allocation decisions, the management incentives, and the strategic priorities that ultimately affect the listed entity.

The most conspicuous and controversial non-baijiu asset is Kaiyi Auto, formerly known as Cowin. In 2018, Wuliangye Group acquired a majority stake in Chery Automobile's Cowin brand for approximately 2.4 billion CNY. The rationale, as articulated at the time, was diversification and local economic development. Yibin was positioning itself as an automotive hub, and Wuliangye, as the city's most important enterprise, was expected to play a role. The acquisition brought manufacturing capacity, a dealer network, and the theoretical ability to participate in China's electric vehicle revolution.

The reality has been more sobering. Kaiyi Auto has struggled in one of the most competitive automotive markets in the world. China's EV sector is dominated by BYD, NIO, Xpeng, and a constellation of well-funded startups, all backed by enormous R&D budgets and genuine automotive expertise. Kaiyi, with its origins as a budget brand and its parentage in a liquor company, has found it difficult to compete for consumer attention, engineering talent, or dealer enthusiasm. Sales volumes have been modest relative to the investment. The brand has limited recognition outside of Sichuan. And the return on the 2.4 billion CNY investment, if you benchmarked it against what that capital could have earned if reinvested in the core baijiu business, has been underwhelming.

This is a pattern familiar to students of Chinese SOEs. The pressure to diversify, to contribute to local economic development, to be a "responsible" state-owned enterprise, often leads to capital allocation decisions that would be difficult to justify on a pure return-on-investment basis. The Kaiyi investment is not large enough to threaten Wuliangye's financial health, but it represents a philosophical tension at the heart of the company: is Wuliangye a baijiu company that happens to be owned by a diversified group, or is it a diversified group that happens to make baijiu? The answer matters enormously for how you value the stock.

More strategically interesting, and less frequently discussed, is Pushen Group, a wholly-owned subsidiary that operates one of the largest specialty packaging and printing businesses in western China. Pushen makes the ornate boxes, holographic labels, and anti-counterfeiting seals that adorn every bottle of Wuliangye. This is not a trivial operation. The packaging of a premium baijiu bottle is an art form in China, as important to the consumer experience as the liquid inside. The box must convey luxury. The label must be impossible to counterfeit. The seal must be tamper-evident. Pushen handles all of this in-house, giving Wuliangye control over a critical component of its brand presentation and anti-counterfeiting infrastructure.

But Pushen is more than just an internal supplier. It is a significant business in its own right, serving external clients in the packaging, printing, and industrial materials sectors. It manufactures 3D holographic products, smart packaging solutions, and specialized industrial materials. The business generates meaningful revenue and provides Wuliangye with vertical integration in a supply chain component that most spirits companies outsource.

The third leg of the hidden conglomerate is Wuliangye Group Finance Co., Ltd., an internal financial services entity that functions as a de facto bank for the Wuliangye ecosystem. This entity manages the enormous cash floats generated by Wuliangye's distribution model, in which distributors must pay upfront for their allocations, often months before they receive the product. The float is substantial. At any given time, Wuliangye is sitting on billions of CNY in distributor prepayments, and the finance company manages these funds, extending credit to group entities, investing in money market instruments, and providing banking services to the broader Wuliangye ecosystem.

For investors in the listed entity, the key concern with the broader conglomerate structure is related-party transactions and capital leakage. How much value is being transferred from the listed company to the parent group through inter-company pricing, shared services, or directed investments? Chinese securities regulators have strengthened disclosure requirements around related-party transactions, and Wuliangye's disclosures have generally been viewed as adequate. But the structural complexity of the group, with its mix of baijiu, automobiles, packaging, and financial services, makes it inherently more difficult to analyze than a pure-play like Moutai.

The conglomerate structure also creates an opportunity, though. If Wuliangye Group were ever to simplify its structure, divesting non-core assets and channeling all capital back into the baijiu business, the re-rating potential for the listed entity could be significant. The market currently applies a "conglomerate discount" to Wuliangye, not explicitly, but implicitly through the valuation gap with Moutai. Narrowing that gap is as much about corporate structure and capital allocation as it is about brand positioning and pricing power.

VII. Competitive Moats: Hamilton Helmer's 7 Powers and Porter's 5 Forces

To understand Wuliangye's competitive position with analytical rigor, it is worth applying two of the most durable frameworks in business strategy. The first is Hamilton Helmer's "7 Powers," which identifies the sources of durable competitive advantage. The second is Michael Porter's "5 Forces," which maps the competitive intensity of the industry. Together, they paint a nuanced picture of a company with extraordinary structural advantages and one critical vulnerability.

Start with Helmer's framework. Wuliangye's primary power is what Helmer calls a "Cornered Resource," an asset that a company possesses and that competitors cannot replicate. The Ming Dynasty fermentation pits are the quintessential cornered resource. As discussed earlier, the microbial ecosystem in these pits has evolved over more than six centuries, producing a complexity of flavor that cannot be reproduced in younger pits. This is not a patent that expires in 20 years or a trade secret that can be reverse-engineered. It is a living biological system that improves with age and that exists in only one place on earth. No competitor, regardless of how much capital they deploy, can replicate this advantage in any commercially relevant timeframe.

The secondary power is Brand. Despite the damage inflicted by the OEM era, Wuliangye remains one of the two most recognized and respected baijiu brands in China. It carries what might be called "social currency": in the hierarchy of Chinese banquet culture, if Moutai is the first choice, Wuliangye is the undisputed second. There is no third brand that comes close. This duopoly of social legitimacy creates a powerful two-tier market in which hosts must choose between Moutai and Wuliangye, with everything else occupying a distinctly lower tier. The brand also benefits from deep cultural embedding. Wuliangye is not just a product but a symbol of Sichuan identity, of Chinese heritage, and of a particular style of hospitality that dates back centuries.

But Helmer's framework also illuminates Wuliangye's weakness. The company suffers from what might be called a "Power Drain," a persistent erosion of brand power caused by the legacy of the OEM model. Even though hundreds of sub-brands have been eliminated, the residual damage to the "Strong Aroma" category persists. Moutai successfully positioned "Sauce Aroma" as the premium flavor profile, associating it with sophistication, rarity, and elite status. "Strong Aroma," by contrast, became associated with volume, accessibility, and lower prices, partly because of the flood of cheap Wuliangye-branded products that saturated the market in the 2000s. Reversing this categorical perception is perhaps Wuliangye's greatest strategic challenge.

There is also a case for Wuliangye possessing "Process Power," which Helmer defines as embedded organizational capabilities developed over long periods. The five-grain fermentation process, the blending methodology perfected over generations of master distillers, and the operational knowledge of managing ancient pit ecology represent a deep institutional capability that is not easily transferred or replicated. This process power operates at a different level than the cornered resource of the pits themselves: even if you had the pits, you would still need the accumulated human knowledge of how to use them optimally.

Now turn to Porter's Five Forces. The bargaining power of buyers is bifurcated. For the flagship 8th Generation Wuliangye, buyer power is extremely low. Distributors compete for allocation, prepay for inventory, and have limited ability to negotiate on price. The product essentially sells itself, and Wuliangye controls the terms. For the mid-tier and lower-tier products that remain in the portfolio, buyer power is higher. These products compete in a more crowded market segment where distributors have alternatives and consumers are more price-sensitive.

The bargaining power of suppliers is low. Wuliangye's raw materials are agricultural commodities, sorghum, rice, wheat, glutinous rice, and corn, all available in abundant supply from domestic sources. No single supplier has pricing leverage over the company. The vertical integration into packaging through Pushen further reduces supplier power in that component of the value chain.

The threat of new entrants is extremely low for the premium segment, precisely because of the cornered resource of the aged pits. Building a competitive high-end baijiu operation from scratch would require not just enormous capital but decades or centuries of pit maturation. For the mid-tier segment, the barrier to entry is lower but still significant due to brand recognition requirements and distribution channel access.

The threat of substitutes is the most interesting and potentially dangerous force. At the high end, the substitutes for premium baijiu are limited in the context of Chinese social rituals. You cannot serve wine or whiskey at a formal Chinese banquet and achieve the same social effect. Baijiu is culturally mandated for certain occasions. However, the longer-term substitute threat comes from generational change. Younger Chinese consumers, particularly in first-tier cities, are increasingly choosing wine, craft beer, Japanese whisky, and low-alcohol cocktails over traditional baijiu. Wuliangye's response, including the development of lower-alcohol products and flavored spirits under sub-brands, reflects an awareness of this trend, but the trajectory is uncertain.

Competitive rivalry is intense but structured. At the very top of the market, it is essentially a duopoly between Moutai and Wuliangye, with Moutai holding the dominant position. Below that, Wuliangye faces serious competition from Luzhou Laojiao, another Sichuan-based Strong Aroma producer with its own aged pits and a strong regional brand. Luzhou Laojiao's flagship, Guojiao 1573, competes directly with the 8th Generation Wuliangye in the 800-1,000 RMB price band. There is also Yanghe, Jiangsu's provincial champion, which has built a formidable national brand through aggressive marketing and distribution. The competitive dynamics differ by price tier and region, but the overall picture is one of a market where the top two players capture disproportionate value while the rest fight over thinner margins.

VIII. The Playbook: Lessons for Investors and Founders

The Wuliangye saga offers three lessons that extend far beyond the baijiu industry. Each one illuminates a principle that applies to any business operating in the luxury goods space, the consumer staples category, or the complex world of state-owned enterprise management.

The first lesson is the "Veblen Good" trap, and it is perhaps the most important. A Veblen Good is an economic concept describing a product for which demand increases as the price increases, because the high price itself is part of the product's value. Luxury handbags, fine watches, and premium spirits all exhibit Veblen Good characteristics to varying degrees. The critical insight from Wuliangye's history is that Veblen Good status is not inherent in the product. It is constructed through brand management, and it can be destroyed through brand mismanagement.

When Wuliangye flooded the market with sub-brands, it did not merely dilute its brand equity in the abstract sense. It destroyed the Veblen Good dynamics that made the flagship product valuable in the first place. If anyone can buy something with the Wuliangye name for 50 RMB, then serving the 800 RMB version no longer sends a clear status signal. The host at the banquet table cannot be sure that the guests will recognize the difference. The social currency evaporates. And once that happens, the only way to justify the 800 RMB price is on the basis of intrinsic product quality, which is a much weaker value proposition than status signaling in the luxury context.

Moutai understood this, whether by design or by fortune, and maintained the exclusivity that preserved its Veblen Good status through the worst of the 2012 crisis. The lesson for founders and investors is clear: if you are building or investing in a brand that derives value from exclusivity, the single greatest threat to that brand is not competition. It is the temptation to make it accessible. Every sub-brand, every licensing deal, every "democratization" initiative that trades long-term brand equity for short-term volume is a step toward the destruction of the very thing that makes the brand valuable.

The second lesson concerns the SOE turnaround question. Can a state-owned enterprise, with its political incentive structures, its local government obligations, and its bureaucratic decision-making processes, execute a genuine strategic transformation? Wuliangye's "Second Entrepreneurship" provides a cautiously optimistic answer. The elimination of sub-brands, the digital transformation, the "1+3" strategy, these are not incremental adjustments. They represent a fundamental rethinking of the company's business model, executed over several years with considerable discipline.

But the SOE context also imposes constraints that a private company would not face. The Kaiyi Auto investment, for example, would be difficult to justify on pure financial grounds, but it makes sense within the framework of SOE obligations to local economic development. The pace of decision-making, while faster than many SOEs, is still slower than a privately held company would manage. And the management incentive structure, while aligned with "High-Quality Development," lacks the equity-based compensation that drives urgency and risk-taking in the private sector.

The third lesson is about category definition, and it may be the most strategically profound. When Moutai positioned "Sauce Aroma" as the premium flavor profile, it did not just win a marketing battle. It redefined the competitive landscape of an entire industry. By associating Sauce Aroma with luxury, sophistication, and exclusivity, Moutai effectively repositioned Strong Aroma, the category that Wuliangye dominates, as the mainstream, accessible, less prestigious alternative. This is category warfare at its most effective: you do not defeat the competitor's product. You defeat the competitor's category.

Wuliangye's challenge is to fight back at the category level. The company has invested in educational campaigns about the complexity and heritage of Strong Aroma baijiu, emphasizing the ancient pits, the five-grain recipe, and the scientific sophistication of the fermentation process. Whether this counter-narrative can succeed in shifting consumer perception is one of the most important open questions in the Chinese consumer goods industry. The stakes are enormous. If Strong Aroma can be re-established as a co-equal premium category alongside Sauce Aroma, Wuliangye's pricing ceiling rises dramatically. If Moutai's category narrative holds, Wuliangye will remain structurally subordinate regardless of how well it executes on product quality and brand management.

IX. Analysis: The Bear vs. Bull Case

The bull case for Wuliangye begins with valuation. As of early 2026, Wuliangye trades at a significant discount to Moutai on virtually every valuation metric: price-to-earnings, price-to-sales, enterprise value to EBITDA. This discount persists despite the fact that the two companies have remarkably similar fundamental characteristics. Wuliangye's gross margins are in the high 70s, approaching Moutai's in the low 80s. Return on equity is robust. Free cash flow generation is strong. The balance sheet is clean, with substantial net cash.

The bull thesis argues that this valuation gap is overdone. If Wuliangye can continue to narrow the price gap of the 8th Generation flagship, improving by even 100-200 RMB over the next several years, the impact on revenue and margins would be substantial given the operating leverage inherent in the business. Every incremental yuan of price on a bottle of baijiu drops almost entirely to the bottom line, since the raw material costs are negligible. The "1+3" strategy, if successful, would further tilt the product mix toward ultra-premium offerings, accelerating margin expansion.

The bull case also points to the structural position of baijiu in Chinese culture. Despite generational shifts in consumption patterns, baijiu remains deeply embedded in the rituals of Chinese social and business life. Weddings, funerals, business negotiations, government events, family reunions: baijiu is present at all of them. The total addressable market for premium baijiu is not shrinking. It is shifting from institutional consumption to private consumption, and the private consumer is, if anything, more brand-conscious and more willing to pay for quality than the institutional buyer was.

The bear case centers on three risks. The first and most frequently cited is the generational shift. China's Gen Z consumers, born after 1995, have grown up with a vastly different set of cultural influences than their parents and grandparents. They are more cosmopolitan, more health-conscious, and more likely to associate sophistication with wine, craft cocktails, or Japanese whisky than with a 52 percent ABV clear spirit that burns on the way down. Wuliangye has attempted to address this through products like "Crush On," a low-alcohol ready-to-drink offering, but it remains an open question whether a brand built on tradition and heritage can authentically connect with a generation that values novelty and global cultural fluency. The comparison to Moutai's collaboration with Luckin Coffee, which generated enormous buzz and cultural relevance, is instructive. Wuliangye has not yet found its equivalent cultural moment.

The second bear risk is the macroeconomic environment. China's economy has slowed from the double-digit growth rates that fueled the baijiu boom of the 2000s and 2010s. The property sector, which was a major driver of wealth creation and thus of luxury consumption, has been in a prolonged downturn. Consumer confidence, while not in crisis, is more cautious than it was five years ago. Premium baijiu is a discretionary purchase, and in a weaker economic environment, the willingness to spend 1,000 RMB on a bottle of spirits is more elastic than the industry might prefer.

The third bear risk is structural and relates to the SOE governance model. While Zeng Congqin has been an effective steward, the SOE structure inherently limits the company's ability to make bold capital allocation decisions. The Kaiyi Auto investment is the most visible example, but the broader question is whether a company that must balance commercial objectives with political and social obligations can ever achieve the laser focus and execution speed required to close the gap with Moutai. Moutai, it should be noted, is also a state-owned enterprise, so the SOE structure alone does not explain the divergence. But Moutai has benefited from a simpler corporate structure, a narrower product line, and, arguably, more commercially minded management over the critical 2012-2020 period.

For investors evaluating Wuliangye on an ongoing basis, two KPIs matter more than any others. The first is the average selling price of the 8th Generation Wuliangye flagship, both the recommended retail price and the actual transaction price in the distribution channel. This single number captures the health of the brand, the effectiveness of supply management, and the trajectory of Wuliangye's position relative to Moutai. If the price is rising and the gap with Moutai is narrowing, the brand rehabilitation is working. If the price is stagnating or falling, the "Second Entrepreneurship" is losing momentum.

The second critical KPI is the revenue mix between the flagship and the remaining portfolio products. As the "1+3" strategy takes hold, the proportion of total revenue derived from the 8th Generation and ultra-premium products should increase over time. A rising mix toward the flagship indicates that the sub-brand cleanup is working and that consumers are trading up within the Wuliangye portfolio. A stagnant or declining mix would suggest that the brand remains anchored to its mid-tier heritage despite management's efforts.

X. Epilogue: Choosing Price Over Volume

In late 2024, Wuliangye made a decision that would have been unthinkable a decade earlier. The company deliberately reduced volume shipments of the 8th Generation flagship, choosing to constrain supply in order to support the channel price. It was a small move in absolute terms, but symbolically, it was enormous. For a company that had spent the early 2000s flooding the market with as much product as it could push through distributors, the decision to prioritize price over volume represented a philosophical transformation.

This is the final step in a journey that has taken two decades. From the hubris of the OEM era, through the humiliation of the 2012 crash, through the slow, painful work of sub-brand elimination and digital transformation, Wuliangye has arrived at a strategy that would make any luxury goods executive nod in recognition: make less, charge more, protect the brand.

Whether it will work, whether Wuliangye can ultimately reclaim its place as a true peer of Moutai or whether the Great Divergence of 2012 is permanent, remains one of the most compelling open questions in the Chinese consumer market. The cornered resource is irreplaceable. The brand, though damaged, retains enormous latent power. The management team has demonstrated both the vision and the discipline to execute a complex turnaround. The question is whether the market, and the culture, will give them enough time.

Wuliangye is the story of a company that had the world, lost it to a brand mistake, and is now systematically, scientifically, and with considerable patience, buying it back. The fermentation pits in Yibin have been working for 650 years. They are in no hurry. The question is whether Wuliangye's shareholders share their patience.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube