Wuliangye Yibin: China's Five-Grain Empire and the Eternal Pursuit of Moutai's Shadow

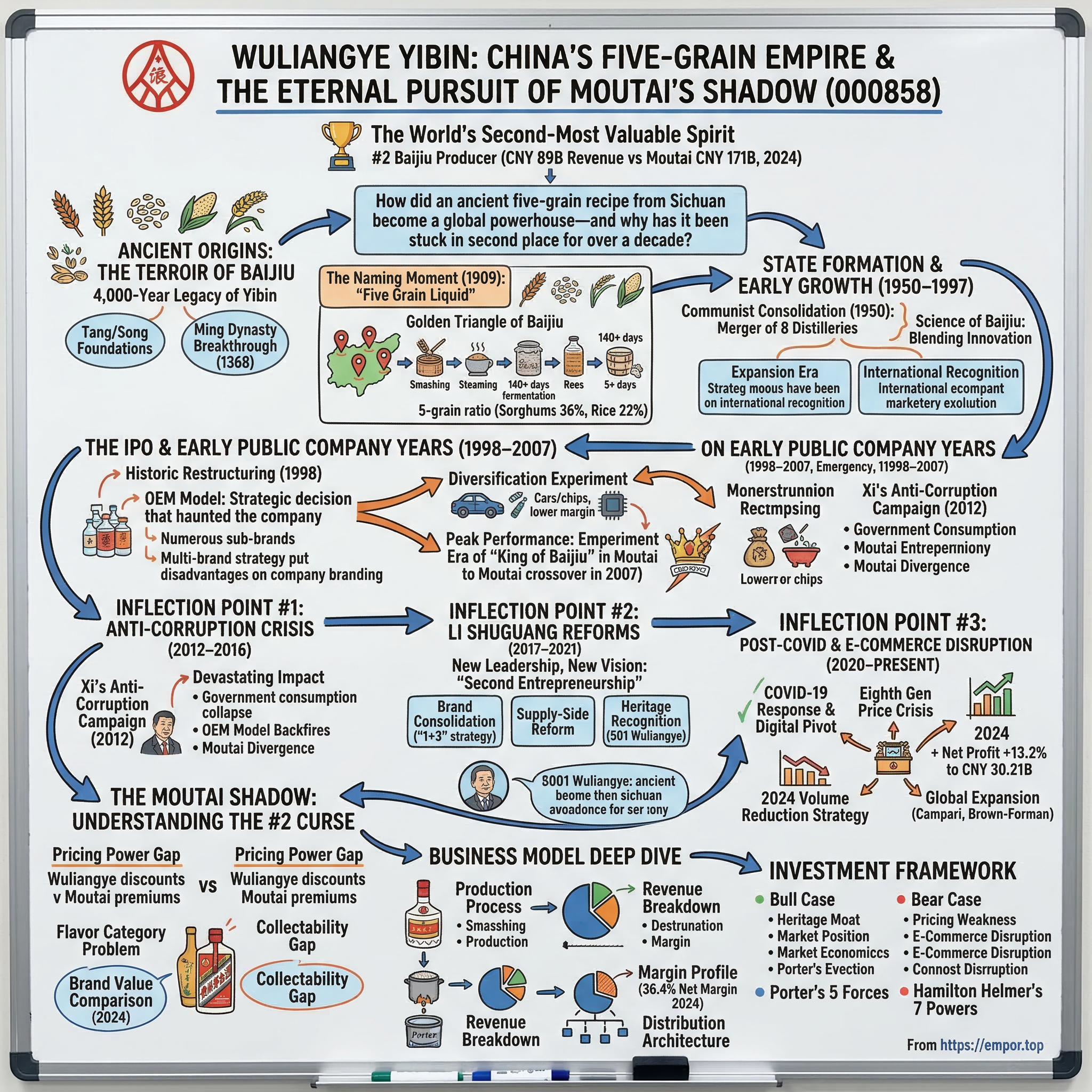

Introduction: The World's Second-Most Valuable Spirit

In the humid lowlands where the Minjiang and Jinsha Rivers converge to form the upper Yangtze, there exists a substance so intertwined with Chinese civilization that its production has continued uninterrupted for over 650 years. Wuliangye is one of the most popular baijiu brands both in China and abroad and as of 2023 is the second most valuable spirits brand in the world.

This is a story about terroir, tradition, and the tantalizing proximity of second place. Wuliangye Yibin is China's second-largest baijiu producer by revenue, with sales of CNY 89 billion in 2024 compared with CNY 171 billion for Moutai. Yet the numerical gap only hints at the strategic chasm between China's two liquor titans—a gap that widened despite Wuliangye once sitting comfortably in first place.

The central question that will guide our exploration: How did an ancient five-grain recipe from Sichuan become a global spirits powerhouse—and why has it been stuck in second place behind Moutai for over a decade despite every advantage in history, scale, and craftsmanship?

Wuliangye is a baijiu distillery headquartered in Yibin, Sichuan, China. The distillery's eponymous spirit is a nongxiang (strong aroma) baijiu made with a mix of five cereal grains: sorghum, rice, glutinous rice, wheat, and corn. This is the "Five Grain Liquid"—a name that dates to a pivotal moment in 1909 and encapsulates centuries of Chinese distillation tradition.

To understand Wuliangye's position, you must first understand baijiu itself. Baijiu is the world's bestselling liquor, with 10.8 billion liters sold in 2018, more than whisky, vodka, gin, rum and tequila combined—three times the global consumption of vodka. This is an industry where Wuliangye plays second fiddle, but second fiddle in an orchestra that dwarfs all others.

What follows is the story of fermentation pits that have operated continuously since 1368, of Communist consolidation and capitalist reform, of a brand that once dominated China's premium spirits market only to watch its rival ascend to nearly mythological status. It's also a story that continues to unfold—in 2024, Wuliangye reported a 13.2% year-over-year increase in net profit to CNY 30.21 billion, with full-year net sales rising 12.0% to CNY 83.27 billion.

The eternal rivalry between Wuliangye and Kweichow Moutai—strong aroma versus sauce aroma, five grains versus sorghum, Sichuan versus Guizhou—represents far more than commercial competition. It's a window into Chinese consumer psychology, government policy, and the elusive alchemy that transforms a commodity into a status symbol.

Ancient Origins: The Terroir of Baijiu

The 4,000-Year Legacy of Yibin

The Company headquarters at the City of Yibin, a region with 4000 years' history of liquor production and one of the world's ten spirit production areas. This is not marketing hyperbole—the archaeological record supports millennia of continuous fermentation in this corner of Sichuan Province.

Yibin and the region of Sichuan as a whole has a long history of alcohol production. While some archaeologists speculate about production of alcohol among the ancient Bo people, the earliest hard evidence for the consumption of alcohol comes from the Han dynasty from which hundreds of drinking vessels and ceramics for the purpose of storing alcohol has been found. Over time as the techniques of brewing, and eventually distillation developed, the technique of using multiple grains as the base for fermentation became a regular practice.

The geography matters. Wuliangye is a specialty of Yibin. A subtropical humid monsoon climate. The annual and day-night temperature differences are small, and the humidity is high, which is very good for grain growth and for the survival of microorganisms needed for wine making. Yibin's unique weak acid yellow soil is also an excellent material for wine cellar.

This terroir—the combination of climate, soil, and water—cannot be replicated elsewhere. Yibin is free of frost and snow with sufficient precipitation, an average annual temperature of 17.9°C and rich bio-diversity, and is a perfect environment for the microorganism used for Baijiu-making to live and reproduce. The area has been accredited by UNESCO and UNFAO as "the most suitable area for the production of high-quality pure distilled liquor in the same latitude on earth."

The Tang and Song Dynasty Foundations

The trail of written evidence begins in earnest during the Tang dynasty. The multi-grain solid fermentation process has been passed down for a thousand years, dating back to Zhongbijiu (Zhongbi liquor) produced with multiple grains in the prime Tang Dynasty. In the year 765, the great poet Du Fu passed by the City of Yibin. Yang Shijun, the then Governor of Rongzhou Prefecture, received him and treated him with Zhongbijiu at the East Pavilion. Du Fu spoke highly of the liquor and wrote a poem.

The evolution continued through the Song dynasty: During the Song dynasty Yao Junyu, a Yibin nobleman, building on the formula for zhongbijiu, developed "Yaozixuequ", a distilled spirit composed of five grains; sorghum, rice, glutinous rice, wheat, and millet, which saw a great deal of commercial popularity and success.

The Ming Dynasty Breakthrough

The pivotal moment in Wuliangye's history came in 1368—the first year of the Ming dynasty. In the Ming dynasty, the Chen family took over production of yaozixuequ and in 1368 built fermentation pits that continue to be in use to this day.

This bears repeating: fermentation pits constructed in 1368 remain in active production today. The oldest one has been producing baijiu since 1368, which is now more than 650 years. It is the earliest cellar-type baijiu yeast fermentation pit which is known and is still in use in China.

These are not museum pieces—they are the competitive moat. The mud lining these ancient pits contains microbial ecosystems that have developed over centuries, creating flavor compounds that modern science can identify but cannot replicate in new facilities. This superior spirit still follows the traditional production process, from fermentation in the aged cellars and years-long brewing to a final appropriate blending. The ancient cellar group of Wuliangye is China's oldest existing crypt-type fermentation pits group, passed down from the Ming Dynasty.

The Naming Moment (1909)

For five centuries, this spirit went by various names. It wasn't until 1909, the very tail end of the Qing dynasty, that a scholar at a Yibin banquet named Yang Huiquan gave the spirit its current name.

The story captures the spirit's evolution from regional specialty to branded product: In the late Qing Dynasty, Deng Zijun inherited Wendefeng Distillery and changed its name as Lichuanyong. In 1909, Deng Zijun attended a banquet of local celebrities with the liquor. Yang Huiquan, a scholar in the late Qing Dynasty, tasted and appraised the liquor to be superb. Yang Huiquan suggested that the name of Zaliangjiu seemed to be vulgar, and although the name of Yaozixuequ was elegant enough, it was still a step away from fully reflecting the flavor of the liquor. Since the liquor was produced with essence of five grain, he suggested the change of name to Wuliangye. His suggestion was warmly applauded by people present at the banquet.

The name "Wuliangye"—literally "Five Grain Liquid"—stuck.

Why Geography Matters: The "Golden Triangle" of Baijiu

Baijiu production in China clusters around specific regions for good reason. Wuliangye is located in Yibin in the Sichuan Province. Yibin is one of the cities with the longest history in the upper reaches of the Yangtze River. It has been defined as "the most suitable area for the production of high-quality pure distilled liquor on the same latitude of the earth" by UNESCO and World Food and Agricultural Organization. This is due to its subtropical monsoon climate, which brings warm and humid air, abundant rain and stable air circulation at the basin. Along with unique and fertile yellow clay soil and rich water resources, it has become the most suitable environment for the growth of more than 150 kinds of microorganisms needed for Wuliangye production.

The production process itself reflects this terroir: The production process involves smashing the grains, steaming, double fermentation using a special bread-like yeast for over 140 days, distillation in ancient earthen vessels, aging, and precise blending, taking approximately five months per batch.

The grain ratio—refined over centuries—represents another inimitable asset: Wuliangye is a premium Chinese baijiu produced by blending liquors fermented from five grains—sorghum, rice, glutinous rice, wheat, and corn—in specific proportions of 36%, 22%, 18%, 16%, and 8%, respectively.

For investors, the significance cannot be overstated: Wuliangye's competitive moat is literally carved into the earth of Sichuan, accumulated over 650 years, and legally protected as cultural heritage. This is not a brand that can be disrupted by a well-funded startup.

State Formation & Early Growth (1950–1997)

The Communist Consolidation

The founding of the People's Republic in 1949 transformed China's economy—and its alcohol industry. In 1950, the newly formed People's Republic merged eight Yibin distilleries under a single state owned entity and in 1959 this company was named Wuliangye after the spirit itself.

In 1950, eight distilleries which was the most famous traditional ones in Yibin including Changfasheng, Lichuanyong, Liudingxing, Tiancifu, Zhangwanhe, Quanhengchang, Tingyuelou and Zhongsanhe merged.

This consolidation brought together the fragmented expertise of Yibin's distilling tradition under unified state control. But it also set the stage for later complications regarding ownership—particularly of those irreplaceable Ming dynasty fermentation pits.

For decades, the State-owned Wuliangye Group, one of China's biggest and most popular baijiu companies, has prided itself on the 16 Ming Dynasty fermentation pits that it uses to produce its baijiu. The manufacturer of high-end spirits based in Yibin, Sichuan Province features the earthen pits in company profiles and promotion videos, calling them an important cultural relic and the secret behind the distinct aroma of its signature baijiu.

The Science of Baijiu: Innovation Under State Control

The 1970s and 1980s saw Wuliangye apply scientific rigor to an ancient art. In 1970s, Wuliangye invented its unique blending technique, which was later referenced and applied to the whole industry. In 1980s, together with Chinese Academy of Sciences, Wuliangye invented computer based blending system. Such system combined the human senses with data, which dramatically improved the blending efficiency and quality.

This collaboration with China's preeminent scientific institutions produced innovations that spread across the entire baijiu industry—a testament to Wuliangye's leadership position during this era.

Expansion Era

During the decades following consolidation, Wuliangye built industrial-scale production capacity while maintaining its artisanal heritage. Wuliangye Group covers a planned area of 18 km². With nearly 50,000 staff members, Wuliangye Group boasts an annual production capacity of 100,000 tons of pure grain raw baijiu made from solid fermentation with the storage capacity amounting to one million tons of raw baijiu. Wuliangye Group is a large-scale production base for pure grain baijiu with its distilleries capable of producing 40,000 tons of baijiu per year.

International recognition followed: Since Wuliangye was awarded the gold prize at the Panama International Exposition in 1915, it has won more than 100 international awards, including 'National Famous Liquor', 'National Quality Management Award', and many others. In 2008, the traditional baijiu-making techniques of Wuliangye were listed as a national intangible cultural heritage.

By the mid-1990s, Wuliangye stood as the undisputed leader of China's premium baijiu market—a position that seemed unassailable given its historical advantages and production scale.

The IPO & Early Public Company Years (1998–2007)

The Historic Restructuring

The late 1990s brought China's largest state enterprises to public markets. In 1998, Wuliangye Distillery was restructured into Wuliangye Group and Wuliangye Yibin Co. Ltd.; in the same year, the joint-stock company was listed on the Shenzhen Stock Exchange.

This restructuring separated the publicly traded operating company from the state-owned parent group—a common pattern in Chinese SOE reform that created both clarity and complexity. The listed entity, Wuliangye Yibin Co. Ltd. (000858.SZ), became the vehicle through which public investors could participate in the company's growth.

The OEM Model: Brilliant Strategy or Fatal Flaw?

Here lies the strategic decision that would haunt Wuliangye for decades. Wuliangye adopted the OEM model and the dealership model in the early 1990s, forming numerous sub-brands to produce and sell more low-end liquors.

The logic seemed sound: leverage the Wuliangye production infrastructure and brand halo to capture the broader market through licensed sub-brands. The results were initially spectacular—revenue growth accelerated as the company's products reached consumers at every price point.

The multi-brand strategy and OEM model put disadvantages on company branding and makes it difficult to gain a foothold in the high-end market. This assessment would prove prescient. By allowing hundreds of sub-brands to carry names associated with Wuliangye, the company sacrificed brand clarity for short-term volume.

The Diversification Experiment

The early 2000s saw Wuliangye venture far beyond liquor. Since 2002, Wuliangye has been diversifying and expanding, entering the industry, including but not limited to the automobile manufacturing and chip industries. But so far, only the car business continues.

This diversification—common among Chinese SOEs flush with cash—diluted management focus and generated returns far inferior to the core baijiu business. The gross profit margins of Wuliangye's liquor business and other businesses are only 77% and 10%, which are far lower than Moutai's 94% and 99%. The investment in unrelated companies further reduced the net profit margin of this second-giant to 36%.

Peak Performance: The Era of "King of Baijiu"

Through the mid-2000s, Wuliangye remained China's dominant premium baijiu producer, commanding higher prices than Moutai and boasting larger revenues. In contrast, Moutai has always adhered to the high-end boutique route, and after 2007, its revenue and profit and terminal prices surpassed those of Wuliangye all the way. Although Wuliangye's operating conditions are improving, due to a midway strategy error, this liquor giant, which was far ahead of Kweichow Moutai at the very beginning, missed the opportunity to secure the first place.

The crossover came around 2007—and Wuliangye has not recovered first place since. The divergence in strategic philosophy was becoming apparent: Moutai focused relentlessly on scarcity and prestige, while Wuliangye pursued volume and ubiquity.

For investors watching this period, the lesson was stark: in luxury goods, scarcity creates value; abundance destroys it—regardless of underlying quality.

Inflection Point #1: The Anti-Corruption Crisis (2012–2016)

Xi Jinping's Anti-Corruption Campaign

In December 2012, the newly installed Xi Jinping administration announced the "eight points" regulation—a set of austerity measures targeting official excess. To crack down on corruption and reinforce the leadership of the Communist Party of China, the CPC announced in December 2012 "eight points" of regulation. Any person or organization violating the regulation would be disciplined. This marked the beginning of the anti-corruption campaign in China. According to an official government website, 187,409 officials were indicted for corruption from 2013 to 2016.

For baijiu producers, this wasn't an abstract policy matter—it struck at the heart of their business model. High-end baijiu had become the currency of Chinese official culture: the essential gift for cultivating relationships, the mandatory bottle at government banquets, the lubricant for transactions both legitimate and otherwise.

The Devastating Impact on Wuliangye

The company said in first-half 2014 that revenue slid 24.9 percent to 11.6 billion yuan ($1.87 billion), while net profit sank 31 percent to 4 billion yuan compared with the same period a year ago. Sales and marketing expenses increased nearly 50 percent year-on-year.

The mathematics were brutal. When government consumption evaporated, volumes collapsed while the company desperately increased marketing spend to find replacement demand that didn't exist at the same scale.

Government Consumption Collapse

The magnitude of the disruption becomes clear when examining the consumption mix. Government and institutional purchasing had constituted an enormous share of premium baijiu sales. When the anti-corruption campaign began, this demand didn't merely slow—it vanished.

The consequences rippled through Wuliangye's distribution network, inventory levels, and pricing power. Dealers who had built their businesses on government relationships suddenly held stranded inventory with no obvious buyers.

The OEM Model Backfires

Here the strategic sins of the 1990s came home to roost. The multi-brand strategy and OEM model put disadvantages on company branding and makes it difficult to gain a foothold in the high-end market.

During the boom years, brand dilution had been masked by insatiable demand. When the music stopped, consumers could choose among dozens of Wuliangye-adjacent products, each eroding the flagship's price premium and prestige. The poorly controlled sub-brands competed with the mainline product, dragging down margins and confusing positioning.

The Moutai Divergence

This crisis marked the definitive parting of ways between China's two liquor giants. Moutai, having maintained stricter brand discipline and positioned itself even more exclusively, weathered the storm better. Its products retained their status as gifts and investments—precisely because they remained scarce.

Wuliangye Yibin, China's second-largest liquor distiller, reported its slowest earnings growth in a decade, reflecting the impact of an intensified anti-corruption campaign on ostentation and a slowing economy.

The gap that opened during this period has never closed. For investors, the crisis illustrated a crucial principle: in premium consumer goods, brand architecture and scarcity management matter as much as product quality.

Inflection Point #2: The Li Shuguang Reforms (2017–2021)

New Leadership, New Vision

With Li Shuguang assuming the position of chairman in 2017, Wuliangye entered the era of "second entrepreneurship." In this stage, Wuliangye began to implement a control and profit-sharing model, concentrating on controlling the supply and value systems, and dominating the distribution of profits among producers, distributors, and terminals.

Li Shuguang's appointment represented a strategic reset. The new chairman understood that Wuliangye's problems were structural, not cyclical—the OEM model and brand proliferation needed reversal, not refinement.

Starting from 2017, Li Shuguang, Chairman of Wuliangye, began to focus on Wuliangye's leading brand and to be back on the right track. Net profit saw a compounded annual growth rate of 27% in the past four years.

The Brand Consolidation Strategy

The company adopted what became known as the "1+3" product strategy: Wuliangye brand "1+3" product strategy: "1" is the generation-specific Wuliangye with the eighth-generation Wuliangye as the signature product; "3" is the super high-end Baijiu series produced from fermentation pits built in the Ming dynasty, with 501 Wuliangye as the signature; vintage Baijiu series with the classic Wuliangye as the signature and cultural customized Baijiu series with Chinese Zodiac Wuliangye as the signature.

This represented a fundamental shift: instead of licensing the brand broadly, Wuliangye would focus on a limited number of well-defined product lines. The dilutive sub-brands would be culled or restricted.

Supply-Side Structural Reform

During the 13th Five-Year Plan (2016-20) period, Wuliangye implemented a supply-side structural reform centered on liquor body innovation and process innovation based on adhering to tradition, building a full life cycle quality management system from "a seed to a drop of fine liquor."

The reforms extended beyond marketing to production itself—improving consistency, enhancing quality controls, and ensuring that every bottle carrying the Wuliangye name met exacting standards.

Heritage Recognition

In 2008, the traditional baijiu-making techniques of Wuliangye were listed as a national intangible cultural heritage. This designation—and subsequent recognitions—formalized what Wuliangye had long claimed: its production methods represented irreplaceable cultural patrimony.

The 501 Wuliangye product line, launched during this era, specifically emphasized the connection to Ming dynasty cellars: "501 Wuliangye" comes from Wuliangye's first workshop—Workshop 501. This "Ming and Qing Ancient Cellar Community" composed of 156 ancient cellars represented by "Changfasheng" and "Lichuanyong" is collectively called Wuliangye 501 Workshop. Here is the "live cellar" with the most complete storage of the cellar structure, the most continuous inheritance of the ancient winemaking techniques, and the longest uninterrupted use time. Among them, the ancient Ming Dynasty cellars 650 years ago are extremely precious resources.

International Recognition

In 2017, the brand value of Wuliangye ranked No. 60 in the "top 500 Asian brands", No. 100 in the "Top 500 Most Valuable Brands in the World" and No. 338 in the "top 500 World Brands".

The Li Shuguang era delivered measurable results. After surpassing 100 billion yuan in revenue and a market value exceeding 1 trillion yuan in advance, Wuliangye is confident in its ability to maintain its high-quality leapfrog development.

Yet even as Wuliangye recovered and grew, Moutai pulled further ahead. The reforms were necessary—but insufficient to close the gap with China's most prestigious spirit.

Inflection Point #3: Post-COVID & E-Commerce Disruption (2020–Present)

COVID-19 Response and Digital Pivot

The pandemic disrupted traditional consumption channels—banquets cancelled, restaurants closed, corporate entertainment suspended. Wuliangye accelerated digital initiatives that had been underway since the late 2010s.

According to Wuliangye, it had cooperated with technology giants Huawei and Alibaba, and software company SAP to establish a leading digital management system in an effort to build itself into a benchmark for digital transformation in the Chinese liquor industry.

The Eighth Generation Price Crisis

Despite strategic reforms, Wuliangye's flagship eighth-generation product has faced persistent pricing pressure. Wuliangye's flagship product, the 8th generation Wuliangye, experienced severe price volatility in wholesale markets, with prices dropping to as low as 800 yuan per bottle. Even during the Mid-Autumn Festival period, prices failed to recover significantly, with current wholesale prices ranging between 810-830 yuan.

The gap between official pricing and market reality undermines the entire brand positioning. In Wuliangye's official flagship store on Taobao, the actual selling price of the eighth generation Wuliangye is CNY 1,070 per bottle, and the price on the platform's billion-dollar subsidy channel is even as low as CNY 858 per bottle.

The Platform Price War

Wuliangye — the Sichuan-based distiller often called the nation's "second national liquor" after Moutai — has found itself caught in the fierce price wars of China's e-commerce age. The high-end baijiu producer recently made an unusual move: it published a list of 46 unauthorised online sellers, including some of China's biggest retail platforms such as Meituan, Taobao, Douyin, and JD.com. The announcement quickly sent shockwaves through the drinks industry. Why would household-name platforms be publicly blacklisted?

At Wuliangye's official flagship store on JD.com, a 500ml bottle of Wuliangye No. 8 sells for RMB 1,000, or RMB 905 per bottle when bought in a two-pack. On Tmall, the same product lists for RMB 1,020. Yet the same bottle sells for RMB 769 on Taobao's subsidy channel, RMB 797 at Meituan's "Famous Liquor" store—a price gap of up to RMB 250.

China's liquor market has struggled with chronic price distortions in recent years, driven by aggressive e-commerce promotions and subsidy wars. Instant retail platforms like Meituan and Ele.me lure consumers with coupons and discounts, often driving retail prices below both traditional e-commerce and wholesale levels. For merchants, this has created a lose-lose dilemma: join the platform campaigns and lose money, or stay out and lose customers. "Some big-brand liquors on instant retail channels aren't just zero-profit — they're negative margin."

Much of the discounted inventory originates from Wuliangye's own authorised dealers, pressured by sales quotas and prepayment targets. "Distributors buy large quantities in advance to keep their annual allocations. When sales slow, they unload to e-commerce platforms at lower prices. It's a structural mismatch between production, policy, and real demand." That model worked during the boom years, but in a sluggish economy, it's proving unsustainable.

2024: Volume Reduction Strategy

At Wuliangye's December 18 manufacturer co-building and sharing conference, Chairman Zeng Congqin said that in 2024, Wuliangye will make every effort to increase channel profits, and will take the opportunity to moderately adjust the ex-factory price of the 8th generation Wuliangye, and at the same time reduce investment volume appropriately. Wuliangye recently signed a 20% reduction in volume within the next year's contract plan with the dealer.

Starting from February 5, 2024, the factory price of the flagship product, the 8th Generation Wuliangye (Popular Edition), was raised from 969 yuan/bottle to 1,019 yuan/bottle, officially entering the thousand-yuan era.

The strategy represents a belated embrace of scarcity economics—reducing supply to support prices rather than pushing volume into a saturated market.

2024 Financial Performance

Despite the challenges, Wuliangye delivered strong results. Wuliangye Yibin Co., Ltd. announced its 2024 financial results, reporting a 13.2% year-over-year increase in net profit to CNY 30.21 billion, driven by robust revenue growth, margin improvements, and strategic expansion into emerging markets. The company's full-year net sales rose 12.0% to CNY 83.27 billion.

The 12% rise marked the fifth consecutive year of double-digit growth.

The company reported 15% volume growth in mid-range baijiu products, which helped offset slower growth in its high-end segments. Sales in third-tier cities and rural markets surged 27% year-over-year, as the firm leveraged its distribution network to capture demand from price-sensitive consumers.

Global Expansion Efforts

Italy's Campari Group has signed a strategic partnership with Chinese baijiu maker Sichuan Yibin Wuliangye Group Co to co-create new products. The agreement will enable the firms to collaborate on channel expansion, strengthen market cooperation and promote brand culture to support their development in China and globally.

A twist on the classic Negroni, the serve combines Campari and Cinzano Vermouth Rosso with a special 40% ABV blend of Wuliangye Baijiu that was co-created by both companies to use in the cocktail. The Wugroni marked the beginning of the partnership between Campari and Wuliangye.

The partnership with Campari—and earlier cooperation with Brown-Forman—signals Wuliangye's ambition to introduce baijiu to international cocktail culture. Brown-Forman, the Louisville-based wine and spirits producer that owns famous whiskey brand Jack Daniels, has already signed a cooperation agreement with Wuliangye.

Product Innovation for New Demographics

Wuliangye's newly launched 29-degree "Love at First Sight" variant faces market acceptance hurdles. Priced at 399 yuan and targeting younger consumers, the product has achieved over 14,000 unit sales across major platforms in its first month, though industry observers question its pricing strategy's effectiveness in reaching intended demographics.

The challenge of recruiting younger consumers is industry-wide. Producers now face a fragmented market where consumers are flooded with product choices and brand loyalty is at a premium. This is especially true for younger buyers, who tend to drink less, to seek novelty when indulging and to see baijiu as too strong and as their "parent's drink".

For investors watching 2024 and beyond, the key question is whether Wuliangye can maintain premiumization while adapting to structural changes in Chinese consumption patterns.

The Moutai Shadow: Understanding the #2 Curse

Why Moutai Pulled Ahead

The divergence between Wuliangye and Moutai represents one of the most instructive case studies in luxury brand management. Moutai has always adhered to the high-end boutique route, and after 2007, its revenue and profit and terminal prices surpassed those of Wuliangye all the way.

So far, the terminal price of Moutai is twice that of Wuliangye, reaching CNY 2,500. Although Wuliangye's operating conditions are improving, due to a midway strategy error, this liquor giant, which was far ahead of Kweichow Moutai at the very beginning, missed the opportunity to secure the first place.

The Pricing Power Gap

The pricing dynamic tells the entire story: Wuliangye's eighth-generation, a high-end liquor, was priced at CNY 1,358, but the discounted price was CNY 1,058. On the contrary, Feitian Moutai, with a retail price of CNY 2,500, has always been in short supply, given that the retail price is nearly double the original price of CNY 1,499. The MSRP of Feitian Moutai is CNY 969 and CNY 1,499, with the premium close to 55%.

Moutai commands premiums; Wuliangye offers discounts. This single fact encapsulates the competitive positioning.

From the perspective of pricing and supply and demand, Moutai has become a status symbol, but Wuliangye is still far away.

The Flavor Category Problem

The baijiu market divides into distinct flavor categories, and this segmentation affects competitive dynamics. Strong-aroma (Luzhou-flavor) baijiu, Wuliangye's category, commands the largest market share overall—but is also the most competitive.

In the field of sauce-flavored liquor, Moutai dominates, accounting for 64% of the market share, far ahead of the second at 6%. However, in the area of Luzhou-flavor liquors, Wuliangye only accounted for 49.1% of the market share under the situation that the second and third, Yanghe shares and Luzhou Laojiao, are in hot pursuit.

Moutai faces virtually no competition in its category; Wuliangye must constantly defend against well-resourced rivals.

Thick flavor is the leading part of the type segment. This confirms that strong-aroma baijiu remains the largest category—but also the most crowded.

Brand Value Comparison (2024)

Elite baijiu brand Moutai (brand value up 1% to USD50.1 billion) extends its reign as the world's most valuable spirits brand for the ninth consecutive year. Wuliangye (brand value down 15% to USD25.9 billion) and Luzhou Laojiao (brand value up 6% to USD8.2 billion) sit in second and third.

Wuliangye is now the world's strongest spirits brand, with a Brand Strength Index (BSI) score of 90.7 of 100, earning an impressive AAA+ rating. Moutai, with a BSI of 89.9 of 100, also scores the top tier AAA+ brand strength rating.

This creates an interesting paradox: Wuliangye scores higher on brand strength metrics but trails significantly in brand value. The explanation lies in pricing power and scarcity—Moutai can monetize its brand more effectively through higher margins.

The Collectability Gap

Beyond consumption, baijiu serves as a store of value—and here too, Moutai dominates. The current market price of a bottle of Moutai, produced around 2000, is about CNY 6,000, while Wuliangye is less than CNY 2,000. Since 2009, there have been 320 instances of Moutai auction prices exceeding CNY 1 million, while only four occasions have seen Wuliangye auction prices exceed CNY 1 million.

The storage value of Wuliangye is lower than that of Moutai. The longer the storage time, the more mellow the taste of liquor. Wuliangye, as a Luzhou-flavor liquor, gives the best drinking experience in ten years, while Moutai, as a sauce-flavor liquor, tastes better in about twenty years.

This creates a self-reinforcing dynamic: Moutai appreciates as an investment, driving further purchases for storage, creating artificial scarcity, and supporting prices. Wuliangye lacks this speculative floor.

Business Model Deep Dive: How Wuliangye Makes Money

The Production Process

Wuliangye is a premium Chinese baijiu produced by blending liquors fermented from five grains—sorghum, rice, glutinous rice, wheat, and corn—in specific proportions of 36%, 22%, 18%, 16%, and 8%, respectively. This liquor, characterized by its colorless transparency, pure and mellow aroma, and refreshing taste with alcohol content typically at 52% ABV. The production process involves smashing the grains, steaming, double fermentation using a special bread-like yeast for over 140 days, distillation in ancient earthen vessels, aging, and precise blending.

Each grain contributes specific characteristics: Sorghum produces spirits with fresh aroma, rice produces pure and mellow spirits, glutinous rice produces pure sweetness and rich flavour, wheat produces spirits with lingering aftertaste, and corn produces strong aroma.

Wuliangye's fermentation takes around 70 days. Fermented grains in pits are taken out layer by layer as the surface layer, the upper layer, the middle layer and the bottom layer. Such procedure can lay a solid foundation for the next "layered distillation" process and also improve the liquor's quality.

Revenue Breakdown

The company generated 92.39% revenue from selling liquors, of which high-end liquors accounted for 85.68% of the total in 2019.

The core 52-degree Wuliangye drives the business. The "1+3" strategy focuses resources on this flagship while developing premium and cultural product extensions.

As of June 2025 Wuliangye Yibin's TTM revenue is $12.63 Billion USD. In 2024 the company made a revenue of $12.37 Billion USD an increase over the revenue in the year 2023 that were of $11.82 Billion USD.

Margin Profile

With a 2024 net profit of CNY 30.21 billion—a 13.2% year-over-year increase—and a 36.4% net margin for the full year, Wuliangye's financial performance underscores its dominance in a premium segment where margins are both a shield and a sword. Its 36.4% net margin in 2024—up from 26.5% in 2020—demonstrates disciplined cost management and pricing power.

Wuliangye's profit margins widened significantly in 2024, driven by cost-control measures and supply-chain optimizations. The company reported a 35.6% net profit margin in Q4 2024, up from 28% in prior periods, aided by ¥0.8 billion in annualized cost savings from automation and supplier discounts.

Distribution Architecture

The China market covers seven major marketing areas, 21 marketing theaters, and 58 marketing bases; the international market has established international marketing centers in Europe, America, Asia-Pacific and other places, and its products are directly sold to 56 duty-free shops abroad, with distribution business covering more than 100 countries.

The channel structure—and Wuliangye's ongoing struggle to manage it—remains central to the investment thesis. The tension between maintaining price discipline and meeting volume targets creates the chronic discounting that erodes brand value.

Investment Framework: Bull Case, Bear Case, and Key Risks

Bull Case

Heritage Moat: Wuliangye possesses production assets that cannot be replicated—fermentation pits producing baijiu since 1368, over 650 years. It is the earliest cellar-type baijiu yeast fermentation pit which is known and is still in use in China. The microbial ecosystems in these ancient pits create flavor profiles impossible to achieve in new facilities.

Market Position: Wuliangye Yibin Co., Ltd. maintains a strong market position within the Chinese baijiu sector. It consistently ranks among the top producers, often holding the second-largest position by market capitalization or sales revenue, following Kweichow Moutai.

Margin Expansion: The trajectory from 26.5% net margin in 2020 to 36.4% in 2024 demonstrates operating leverage and pricing power, even amid challenging conditions.

Premiumization Trend: The global luxury baijiu market is poised for significant growth in the coming years, driven by factors such as rising disposable income, increasing demand for premium spirits. The market is projected to grow at a CAGR of 6.77% from 2023 to 2032.

International Partnerships: The Campari and Brown-Forman relationships provide channels for global expansion and product innovation that could unlock growth beyond China.

Brand Strength: Wuliangye is now the world's strongest spirits brand, with a Brand Strength Index score of 90.7 of 100, earning an impressive AAA+ rating.

Bear Case

Structural Pricing Weakness: Volume metrics show Wuliangye products achieved 27,300 tons in sales, up 12.75%, generating revenue increase of 4.57%. This translates to a 7.25% unit price decline, demonstrating classic "volume up, price down" dynamics.

E-Commerce Disruption: Platform subsidies and dealer inventory liquidation create persistent price erosion that undermines brand positioning. "Some big-brand liquors on instant retail channels aren't just zero-profit — they're negative margin."

Demographic Headwinds: Population decline in the primary baijiu consumer cohort (male aged 30-59) could be a negative driver for sector volume growth, leading to a potential 13% volume decline during 2023-25E.

Capacity Expansion Risk: Combined capacity of the top 6 baijiu companies is expected to expand 37% by 2025 from 2023 level. Combined capacity of the top five baijiu companies is expected to grow 37% during 2023-25 while demand is likely to contract 13%.

Category Competition: Unlike Moutai's dominance of sauce-aroma baijiu, in the area of Luzhou-flavor liquors, Wuliangye only accounted for 49.1% of the market share under the situation that the second and third, Yanghe shares and Luzhou Laojiao, are in hot pursuit.

Porter's Five Forces Analysis

Threat of New Entrants: LOW The ancient fermentation pits, intangible cultural heritage status, and centuries of accumulated microbial ecosystems create barriers that capital alone cannot surmount. New entrants might produce baijiu; they cannot produce Wuliangye.

Bargaining Power of Suppliers: LOW Raw materials are agricultural commodities with multiple suppliers. To ensure the highest quality of the source grains, Wuliangye builds up a nationwide production base of Baijiu-making grains with an area of millions of square kilometers.

Bargaining Power of Buyers: MODERATE TO HIGH Individual consumers have limited power, but large distributors and e-commerce platforms have demonstrated ability to extract discounts and pressure margins. The dealer channel structure gives intermediaries significant leverage.

Threat of Substitutes: MODERATE Whisky, wine, and other spirits compete for consumption occasions, particularly among younger consumers. However, baijiu's cultural integration into Chinese social rituals provides protection in traditional contexts.

Competitive Rivalry: HIGH Within the strong-aroma category, competition from Luzhou Laojiao, Yanghe, and others is intense. Wuliangye's market share faces constant pressure from well-resourced competitors.

Hamilton Helmer's 7 Powers Framework

Scale Economies: Present but not decisive. Wuliangye has significant scale, but so do major competitors.

Network Effects: Limited. Baijiu consumption doesn't exhibit direct network effects.

Counter-Positioning: Wuliangye's five-grain recipe and ancient pits represent a position that competitors cannot easily copy. However, Moutai's sauce-aroma counter-positioning has proven more effective at commanding premiums.

Switching Costs: Low for individual bottles; moderate for brand loyalty in gifting contexts where the recipient's expectations matter.

Branding: STRONG. Wuliangye's brand ranks among the world's most valuable spirits brands. However, brand value monetization trails Moutai significantly.

Cornered Resource: STRONG. The Ming dynasty fermentation pits represent a genuinely cornered resource—irreplaceable assets with documented continuous use for 650+ years.

Process Power: MODERATE. The blending and fermentation expertise is substantial but more transferable than the physical assets.

Key Performance Indicators for Ongoing Monitoring

For investors tracking Wuliangye's performance, three metrics matter most:

1. Eighth-Generation Wuliangye Wholesale Price vs. MSRP

This spread reveals the company's true pricing power. When wholesale prices fall significantly below the CNY 1,499 MSRP, it signals channel stuffing, demand weakness, or both. The recent drop to CNY 800-830 wholesale represents a warning sign that required the company's volume reduction response.

Why it matters: Luxury goods command luxury margins only when scarcity is maintained. Persistent discounting destroys the brand equity that decades of cultivation created.

2. Mix Between High-End and Mid-Range Products

The company reported 15% volume growth in mid-range baijiu products, which helped offset slower growth in its high-end segments.

When growth increasingly comes from lower-priced products, margins compress and the brand drifts toward commodity status. The ratio of flagship Wuliangye sales to series and mid-range products reveals strategic direction.

Why it matters: Premiumization drives margin expansion; commoditization erases it.

3. Channel Inventory Levels and Dealer Profitability

The company's relationship with distributors determines whether price discipline can be maintained. When dealers lose money, they liquidate inventory to platforms willing to subsidize losses—creating the price chaos that Wuliangye's October 2024 "grey list" attempted to address.

Since Pu Wu's channel profit is smaller than that of Flying Maotai and Guojiao 1573, dealers have had to sell at a price far lower than the recommended retail price in the market in order to complete sales tasks and repay payments. "Nationwide, Wuliangye dealers are not making any money."

Why it matters: Sustainable brand premiums require sustainable dealer economics.

Regulatory and Legal Considerations

State Ownership: Wuliangye remains a state-owned enterprise, with the parent Wuliangye Group controlled by the Sichuan provincial government. This creates both protections (implicit government support, regulatory advantages) and constraints (political priorities may not align with shareholder returns).

Fermentation Pit Ownership: The Yins claim they were unambiguously the legal owners of the pits until the end of 2009, when the Wuliangye Group abruptly cancelled its lease agreement but refused to move its workers out of the pits. While this specific dispute appears resolved, the complex history of property rights during China's socialist transformation creates ongoing uncertainty about certain assets.

Anti-Corruption Vulnerability: Government consumption drove significant historical demand. Policy changes can rapidly alter the demand landscape, as demonstrated in 2012-2016.

Trade and Export: At present, the performance of Chinese Baijiu in the international market is still relatively small. By 2024, the share of Chinese Baijiu in the international market will be less than 8%. International expansion faces cultural, regulatory, and tariff barriers.

Myth vs. Reality

| Common Narrative | Reality |

|---|---|

| "Wuliangye is catching up to Moutai" | The absolute revenue gap continues to widen despite Wuliangye's growth. Moutai's 2024 revenue of CNY 171 billion dwarfs Wuliangye's CNY 89 billion. |

| "Ancient pits guarantee premium pricing" | Heritage provides quality differentiation but hasn't prevented persistent wholesale discounting. Execution matters as much as assets. |

| "The OEM problem is solved" | Sub-brand proliferation has been reduced, but channel discipline remains weak. The October 2024 "grey list" demonstrates ongoing struggles. |

| "International expansion will diversify revenue" | Baijiu remains overwhelmingly domestic. Export revenues remain de minimis despite years of effort. |

| "Young consumers will adopt baijiu as incomes rise" | Generational preferences trend away from high-ABV spirits. The 29% ABV "Crush On" product attempts to address this but faces uncertain reception. |

Conclusion: The Enduring Second Place

Wuliangye Yibin stands as one of the world's great spirits companies—heir to production traditions spanning seven centuries, owner of irreplaceable fermentation assets, and the second-most valuable spirits brand globally. Its 36% net margins, consecutive years of double-digit growth, and 100-billion-yuan revenue demonstrate a business of substantial quality.

Yet the comparison to Moutai reveals what Wuliangye is not: a luxury brand with genuine scarcity economics. Brutal competition makes Wuliangye's moat not as comprehensive as Moutai's. Therefore, it is difficult for Wuliangye to stand out as a candidate to be a 'second' Moutai.

The strategic sins of the 1990s—OEM proliferation, brand dilution, volume-over-value—created wounds that decades of reform have not fully healed. When consumption collapsed in 2012-2016, Moutai's scarcity-focused positioning proved resilient while Wuliangye's accessibility worked against it.

The current challenge—e-commerce platform subsidies driving wholesale prices below dealer cost—represents the latest manifestation of these structural issues. Volume reduction strategies may stabilize pricing, but at the cost of growth that investors have come to expect.

For long-term fundamental investors, Wuliangye presents a classic value proposition: a high-quality business trading at a discount to its dominant competitor, with margin expansion potential and heritage assets providing downside protection. The bull case rests on management's ability to achieve what Li Shuguang's "second entrepreneurship" started: transforming Wuliangye from China's most accessible premium baijiu into a genuinely scarce luxury brand.

The bear case acknowledges that this transformation may be structurally impossible. Once a brand has signaled accessibility through thousands of sub-brands and persistent discounts, rebuilding exclusivity requires destroying significant near-term value. Management has shown willingness to pursue volume reduction—but whether they can sustain it through the inevitable revenue pressure remains unproven.

What cannot be denied is the extraordinary asset base: The company's fermentation pits, some over 700 years old, are a testament to its commitment to preserving the multi-grain solid fermentation process that defines its unique aroma and flavor. This heritage isn't just symbolic—it's a competitive moat. Unlike commoditized spirits, Wuliangye's baijiu commands premium pricing due to its perceived quality and cultural cachet.

The "Five Grain Liquid" will continue flowing from those Ming dynasty pits for generations to come. The question is whether Wuliangye can finally translate that heritage into the pricing power that has eluded it for nearly two decades—or whether second place is where it will remain.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube