Luzhou Laojiao: The 450-Year-Old Startup

I. Introduction: The "Liquid Gold" of Sichuan

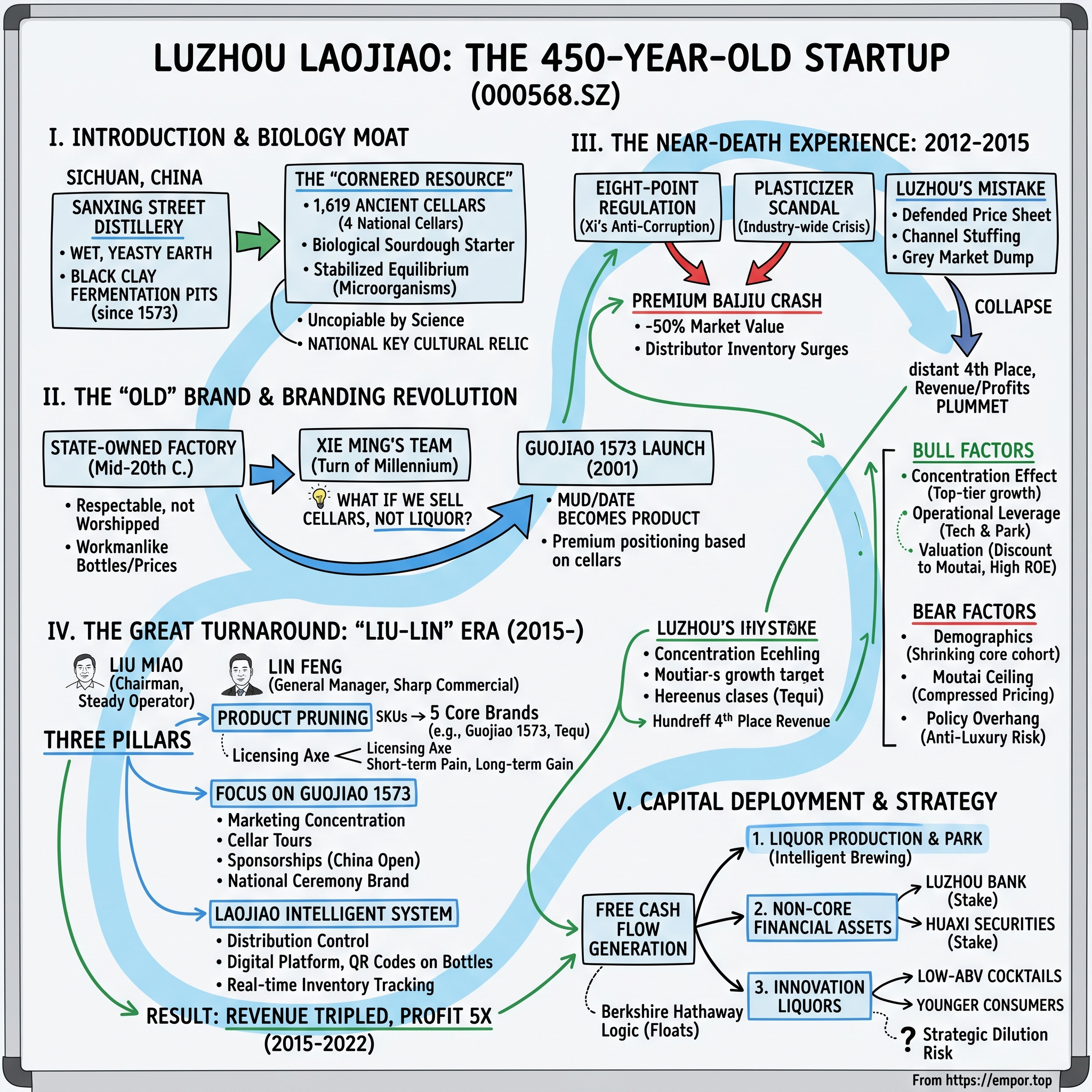

Walk into the basement of Luzhou Laojiao's oldest distillery on Sanxing Street, in the humid, hilly Sichuan city that shares the company's name, and the first thing that hits you is not the smell of alcohol. It is the smell of earth. Wet, yeasty, black, almost edible earth. The cellars, rectangular pits dug into the ground and lined with a specific grey-black clay, have been fermenting grain continuously since 1573, the sixth year of the Wanli Emperor's reign in the Ming Dynasty. Workers in white rubber boots shovel steaming sorghum out of these pits into woven bamboo baskets, while the microorganisms responsible for the whole miracle — hundreds of strains of bacteria, yeasts, and molds that have been breeding and inbreeding in that mud for four and a half centuries — keep quietly doing what they have always done.

This is the single most important asset owned by a company with a market capitalization north of thirty billion U.S. dollars. Not a patent portfolio. Not a server farm. Mud.

Luzhou Laojiao Company Limited, ticker 000568 on the Shenzhen Stock Exchange, is one of the "Big Four" of Chinese baijiu, the country's fiery, pungent, grain-based national spirit. It trades at a premium valuation. It generates net margins above forty percent — the kind of margin a luxury house in Paris would envy. And for roughly a decade now it has been locked in a ferocious, reputation-driven cage match with Wuliangye, the other great Sichuan baijiu giant just an hour and a half down the Yangtze, for the third-place throne behind Kweichow Moutai and Wuliangye itself. Inside the industry, Luzhou is often described as the most aggressive, the hungriest, the most willing to do unconventional things for a state-owned enterprise.

That aggression is the thesis of this episode. Because the single most surprising thing about Luzhou Laojiao is that the product driving most of its profit, the ultra-premium Guojiao 1573, is barely older than your average millennial. The brand was launched in 2001. It was conjured out of thin air — or more precisely, out of those ancient cellars — to rescue a sleepy state-owned enterprise that was getting systematically out-sold by more polished competitors. The playbook the company ran to pull that off, and then the near-death experience that almost ended it a decade later, and then the comeback that tripled revenue in seven years, is one of the more underappreciated business stories in modern China.

It is a story of a Cornered Resource meeting a Masterclass in Branding. It is a story of a company with the oldest continuously operating fermentation pits in the world that nevertheless had to reinvent itself like a Silicon Valley startup to survive. And it is a story of an industry where a single Communist Party policy announcement in late 2012 vaporized half the sector's market capitalization in eighteen months, and where the winners that emerged from that rubble learned a set of lessons that still shape how they behave today.

This is Luzhou Laojiao: the 450-year-old startup.

II. The "Cornered Resource": 1573 and the Power of Mud

To understand why Luzhou can charge what it charges, you have to understand a quirk of biology that would make a venture capitalist weep with envy.

Baijiu is a broad category, not a single drink. It splits into several "aroma" styles — sauce aroma, light aroma, rice aroma, and the dominant one, strong aroma. Luzhou is considered the cradle of strong aroma baijiu, the style that accounts for more than two-thirds of all baijiu consumption in China. And the essence of strong aroma baijiu is not, as you might assume, the grain or the water or the distillation technique. Those things matter. But the soul of the liquor is the cellar itself.

Here is how the process works, stripped of poetry. Sorghum and other grains get cooked, mixed with a starter culture called qu, and dumped into a rectangular clay-lined pit in the ground. The pit is sealed with mud. For sixty to ninety days, an enormous and wildly complex community of microorganisms — far more diverse than the yeast strains used in whisky or wine — ferments the grain. After fermentation the mash is pulled out, distilled, and the fresh spirit is aged for years in ceramic jars. Then the real magic: a tiny amount of the oldest, most aromatic spirit is blended with younger liquor to produce the final bottled product.

The critical fact is this: the longer a cellar has been in continuous use, the more complex, the more stable, and the more flavorful the microbial ecosystem inside it becomes. A brand new cellar produces liquor that tastes, frankly, rough. A fifty-year-old cellar produces something acceptable. A three-hundred-year-old cellar produces something transcendent. And a cellar that has been running without a single interruption since the Wanli era, like the ones at Luzhou's National Cellar No. 1, produces something that, in the Chinese baijiu hierarchy, is treated with a kind of religious reverence.

You cannot shortcut this. Chinese scientists have tried. They have sequenced the microbial communities, attempted to inoculate new cellars with old mud, attempted to accelerate the aging. It does not work. The ecosystem in an ancient cellar is not just a collection of organisms — it is a stabilized equilibrium, a living sourdough starter the size of a swimming pool, that took generations to evolve and cannot be photocopied.

Luzhou Laojiao owns 1,619 of these ancient cellars. Four of them, the so-called National Cellar group, date to 1573. They have been designated National Key Protected Cultural Relics by China's State Council, which means they are legally protected in the same category as the Forbidden City and the Terracotta Warriors. You literally cannot dig new ones that are as old. No one can. Not even with a trillion dollars. That is a Cornered Resource in the Hamilton Helmer sense of the term — a production factor that one firm uniquely controls, that competitors cannot replicate, and that generates outsized economic rents.

What the modern company did, and what the previous generation of managers failed to do, was to translate this geological and biological advantage into a brand. For most of the twentieth century, Luzhou was a state-owned factory churning out workmanlike bottles at workmanlike prices. The Qing and early Republican history was colorful — the Wen family, the Tianchenghe distillery, the consolidation of thirty-six small workshops into a single state enterprise in 1955 — but none of it showed up in the purchase price of a bottle. Luzhou was respected. It was not worshipped.

That changed at the turn of the millennium. A then-deputy general manager named Xie Ming and his team looked around at Moutai's growing premium halo and asked a question that had simply never been asked in the baijiu industry with that kind of commercial intent: what if we sold the cellars, not the liquor? What if the mud, the date 1573, the idea of a National Cellar, became the product? That question produced Guojiao 1573, and it set in motion everything that follows.

The setup for the rest of this story is that Luzhou spent decades sitting on top of a biological gold mine without knowing how to monetize it. Once they figured out the marketing, the gold mine started printing money. And then, a decade later, the Chinese government almost took the printing press away.

III. The Near-Death Experience: 2012 – 2015

On the evening of December 4, 2012, the newly installed Politburo Standing Committee of the Chinese Communist Party issued an eight-point document that sounded, at first, like routine housekeeping. The Eight-Point Regulation, or baxiang guiding, called on officials to reduce bureaucratic formalism, simplify receptions, cut down on ceremonial banquets, and avoid ostentatious displays. Within the political class it was read as the first salvo of Xi Jinping's anti-corruption campaign. Within the baijiu industry, it was read as a bullet aimed squarely at their biggest customer.

Because the uncomfortable truth, which everyone in China knew and no one publicly said, was that an enormous share of premium baijiu — somewhere between a third and a half, depending on whose estimate you believed — was purchased for the purpose of gongwu xiaofei, government-related consumption. Officials wined each other at banquets. Businesses gifted cases of Moutai and Guojiao 1573 to bureaucrats whose signatures they needed. The premium tier of the industry had, in effect, become an informal currency of influence. When the Party signalled that the music was about to stop, the entire tier heard it.

And then, just three weeks before the Eight-Point Regulation, the industry had already been hit by a separate, unrelated scandal. In November 2012, state broadcaster reports and a well-publicized consumer investigation revealed that bottles of Jiugui Liquor, a smaller premium baijiu player, contained levels of plasticizer chemicals that exceeded regulatory norms. The plasticizer crisis detonated across the entire category. Plasticizers migrated into baijiu from the plastic components of production and storage equipment; the problem was industry-wide, not Jiugui-specific, and consumers suddenly began to ask whether their ceremonial gift bottles were also quietly poisoning them.

The combination was devastating. Between late 2012 and the bottom in 2014, the premium baijiu sector lost roughly half of its market value. Distributor inventories swelled to absurd levels. Secondary-market prices for top-shelf bottles, which had been climbing for years on a tide of gifting demand, went into free fall. Some smaller brands simply stopped paying their employees.

Luzhou Laojiao did not handle the crisis well.

The company's management at the time, led by Xie Ming, made what would in hindsight be identified as the defining mistake of the cycle. They tried to defend price. When distributors called up asking for support — asking for permission to discount, asking to slow new shipments, asking for help clearing inventory — management refused. The official line was that Guojiao 1573 was a premium product, that lowering prices would permanently damage the brand, and that the company would ride out the storm by maintaining the listed price sheet. Inventory was allowed to build up at the distributor level. Channel stuffing, to be blunt, was allowed to continue.

It did not work. What happened instead was a grey market. Distributors, unable to sell at official prices and desperate for cash, began dumping bottles outside official channels at steep discounts. Within eighteen months the actual transaction price of a bottle of Guojiao 1573 had collapsed far below the listed price. The brand's premium positioning — the entire foundation of the Guojiao 1573 project — was visibly bleeding out in real time.

Meanwhile, the competition handled it differently. Kweichow Moutai, blessed with a tighter supply and a stronger grip on its distribution network, held price relatively well. Wuliangye struggled but kept its volume commitments manageable. Luzhou fell the hardest. It dropped from a respected member of the "Big Three" to a distant fourth, overtaken by Yanghe, a faster-growing rival from Jiangsu province. Revenue declined. Profits collapsed. For a company that had spent the 2000s aggressively marketing itself as the heir to a premium heritage, the fall was humiliating.

By 2015, the Luzhou SASAC — the municipal State-owned Assets Supervision and Administration Commission, which owns the controlling stake on behalf of the city of Luzhou — had seen enough. The city government, which regards Luzhou Laojiao as both its largest taxpayer and a cultural crown jewel, concluded that new leadership was required. What happened next is one of those rare cases where a state-owned enterprise actually behaves like a startup that has hired a new CEO.

IV. The "Liu-Lin" Era: The Great Turnaround

In June 2015, Liu Miao became Chairman of Luzhou Laojiao. A few months earlier, Lin Feng had been promoted to General Manager. Both were internal, both had risen through the company's commercial and operations ranks, and both had watched the previous three years of drift with undisguised frustration. The Luzhou locals — and baijiu is a deeply local industry, where senior cadres often grow up within a few kilometers of the distillery — took to calling the new duo "Liu-Lin", the way an older generation might have referred to a pair of generals sharing a campaign.

Liu, the older of the two, projected an unflashy steadiness. Trained as an engineer, he had managed the production side of the business and knew the rhythms of the cellars intimately. Lin was the sharper, more commercial half — he had worked in sales, had direct relationships with distributors across the country, and understood that the plasticizer-era collapse had been, at its root, a distribution failure rather than a brand failure. Together they set about executing what was, in effect, a corporate turnaround plan inside a 450-year-old enterprise.

The playbook had three pillars.

The first pillar was product pruning. In the decade leading up to 2015, Luzhou had developed a bad habit, common among Chinese consumer companies of that era, of licensing out its name to every distributor who would pay for it. The company's trademarks appeared on hundreds of sub-brands, most of them low-quality, many of them sold at prices so low they actively damaged the parent brand's credibility. Liu and Lin took the axe to this. Within about eighteen months, the company consolidated hundreds of SKUs into five core strategic brands: Guojiao 1573, Luzhou Laojiao Tequ (the "special" grade), Touqu (head grade), Erqu (second grade), and a smaller portfolio of flavored and innovation products. Entire revenue streams disappeared overnight. Distributors complained. Retail shelves were forcibly thinned. Short-term, the company gave up revenue. Long-term, it gave itself back the ability to charge a premium.

The second pillar was the single-minded focus on Guojiao 1573 as the company's Moutai-equivalent. Rather than hedge across the portfolio, Liu and Lin made a capital-allocation decision that in hindsight looks obvious and at the time looked bold: they concentrated marketing spend, distribution priority, and best inventory on Guojiao 1573, and treated the product not as a line extension but as the strategic heart of the company. They invested in brand experiences — cellar tours, tasting academies, sponsorships of the China Open and the Chinese classical music scene. They cultivated Guojiao 1573 as a "national ceremony" brand, the kind of bottle that appears at weddings, state banquets, and business dinners where you are quietly signalling that the evening is important. The positioning worked. The brand's gifting and banqueting share climbed, particularly in the post-anti-corruption environment where the consumer, rather than the official, had become the dominant premium buyer.

The third pillar was the most technically interesting, and in some ways the most lasting. It was called Laojiao Intelligent, and it was a distribution control system.

Remember that the worst damage of the 2012-2014 crash had come not from falling demand but from loss of control over price. Distributors, drowning in inventory, had dumped bottles into the grey market. To prevent that from ever happening again, Liu and Lin rolled out a digital platform that tracked every single bottle of Guojiao 1573 from the factory all the way to the final consumer. Each bottle carried a QR code. Each scan registered location. The company could see, in near real time, where its inventory was, how fast it was moving, and whether any given distributor was selling too much too fast or dumping into neighboring territories at cut prices. Think of it as an operating system laid on top of a supply chain that had historically been run on handshake relationships and paper invoices.

This was a big deal for two reasons. First, it gave management a lever to defend pricing that the previous generation had simply not possessed. Second, it sent a signal to distributors that the relationship between them and Luzhou had changed. The company was no longer a tolerant, price-indifferent older cousin; it was now a partner with eyes in the supply chain, willing to cut off bad actors.

The combined effect of these three pillars was dramatic. Between 2015 and 2022, Luzhou Laojiao's revenue roughly tripled, and its net profit grew by roughly five times. The stock went from being a recovery play to one of the best-performing large-cap consumer names on the Shenzhen Exchange. Guojiao 1573, the product that had been sold at grey-market discounts during the crisis, clawed its way back to an ex-factory price that placed it firmly in the top tier of Chinese premium spirits. The company reclaimed its position within the Big Four. And Yanghe, which had briefly displaced it, was now being outgrown.

None of this would have been possible without a stable leadership team willing to think in five-year rather than five-quarter cycles. Which raises the next question: inside a state-owned structure, how do you keep a management team aligned with shareholders?

V. Current Management & Incentives

State-owned enterprise leadership is one of the most misunderstood topics in Chinese corporate analysis. The foreign stereotype is that SOE executives are political appointees, indifferent to profit, incentivized only by their relationship with the Party. The reality in the modern baijiu sector is considerably more nuanced.

Liu Miao, born in the early 1960s, is a product of the Luzhou system in the most literal sense. He joined Luzhou Laojiao in the 1980s, climbed through production and operations, and had held positions at every major rung of the company by the time he was handed the chairmanship. Within the organization he is known as a disciplined, almost austere operator — more comfortable walking through a production facility than giving press interviews, more interested in cellar temperature logs than in media profiles. Colleagues describe him as a "General" in the sense that George Marshall was a general: the quiet kind, the organizer, the one who believes that logistics wins wars.

Lin Feng, the General Manager, is the counterweight. Younger, more outgoing, more inclined toward distribution strategy and brand-building, he is the company's public face in investor settings. While Liu sets the overall framework, Lin has historically owned the commercial execution. The pairing works because each is genuinely good at what the other is not, and because neither appears to be playing the internal-succession game at the other's expense.

Both answer, ultimately, to the Luzhou SASAC, which holds the controlling stake in Luzhou Laojiao Group, the parent entity. The SASAC in turn reports to the Luzhou municipal government. In theory, this makes the company a deeply political animal. In practice, the city of Luzhou has exactly one reason to exist in the Chinese national consciousness, and that reason is its distilleries. Luzhou Laojiao is the largest single tax-paying entity in the municipality, contributing double-digit percentages of the city's tax base in good years. The incentives of the city government and the incentives of the minority shareholders are, therefore, surprisingly well aligned. Both want the company to thrive. Both want it to grow. Both want the stock to do well, because the listed entity's valuation feeds back into the parent's balance sheet and the city's economic statistics.

What made the Liu-Lin era philosophically distinct from previous eras, though, was the 2021 restricted share incentive scheme.

For most of Luzhou Laojiao's modern history, the managerial incentive structure had been a hybrid of fixed salary, modest cash bonuses, and the usual invisible SOE benefits — housing, political standing, promotion pathways. Equity ownership for management was negligible. In 2021, the company rolled out a restricted share plan that granted equity to several hundred key employees — executives, R&D leads, sales managers, and production cadres — with vesting tied to multi-year revenue and profit growth targets. The size of the grant was modest relative to the total float, but the symbolism was enormous. It was one of the first large-scale equity incentive programs at a provincial SOE in the baijiu sector, and it explicitly tied the personal wealth of the operating team to the performance of ticker 000568 on the Shenzhen Exchange.

This is the moment, in the view of many long-term holders, when Luzhou Laojiao's corporate DNA quietly changed. Before 2021, the company was an SOE that happened to be listed. After 2021, it was a listed company whose operators had a personal stake in the price chart. The KPIs against which the grants vest — revenue growth, net profit growth, ROE thresholds — are the same KPIs that a rational minority shareholder would want. Lin Feng, Liu Miao, and their team now have a direct financial interest in the outcome that a foreign investor cares about, not merely the bureaucratic interest in hitting a political target.

It is not a free-market nirvana. The city still controls the majority vote. Strategic decisions of a certain magnitude — significant M&A, dividend policy, large capital deployment — still require political sign-off. Executive compensation, while better than before, remains well below the levels that a comparable private enterprise would pay. The plasticizer-era temptation to stuff channels for short-term revenue recognition has not been structurally eliminated, only culturally discouraged.

But the direction of travel is clear. What the company calls, a little poetically, its "SOE with a private soul" posture — disciplined state ownership on top, merit-based operational aggressiveness underneath — is what produced the Liu-Lin turnaround and what sustains the business model today.

VI. Capital Deployment & The "Hidden" Bank

Here is where the story takes a turn that surprises almost every first-time foreign analyst.

If you look at the consolidated financials of Luzhou Laojiao, you will notice that the company carries a meaningful pile of investment assets on its balance sheet. Some of those investments are in entities that have nothing to do with sorghum, cellars, or the distillation arts. The two most prominent are Luzhou Bank, a city-commercial bank headquartered in Luzhou, and Huaxi Securities, a mid-sized brokerage based in Chengdu and listed on the Shanghai Exchange. In both cases, Luzhou Laojiao is a large, strategic shareholder rather than a passive portfolio holder.

In Luzhou Bank, the company is the largest shareholder with a stake in the mid-teens. In Huaxi Securities, the company holds around ten percent of the equity, a stake that was acquired during the brokerage's pre-IPO rounds in the mid-2010s and has since become one of the more quietly valuable non-core assets in any Chinese consumer company's portfolio.

Why on earth does a baijiu company own a bank and a brokerage?

The conventional Western comparison is that global spirits companies — Diageo, Pernod Ricard, Brown-Forman — deploy their prodigious free cash flow into buying other brands. Diageo bought Casamigos. Pernod bought Jefferson's. Brown-Forman bought Glendronach. The logic is that the distribution platform scales, the brand portfolio diversifies, and the acquirer captures EBITDA multiples of fifteen, twenty, even twenty-five times for the right premium label.

Luzhou Laojiao has almost never done this. Part of the reason is cultural: the fractured, locally-rooted nature of the Chinese baijiu industry means that buying a smaller rival rarely gives you distribution leverage. Part of the reason is regulatory: cross-province SOE consolidation in the liquor sector faces political headaches that a Diageo-style deal never encounters. And part of the reason is simply that the company has chosen a different philosophy. Instead of accumulating brands, it has accumulated financial assets that throw off yield, carry strategic influence in Sichuan, and act as a counter-cyclical hedge against the volatility of the baijiu market itself.

Think of it this way. Liquor cycles in China are violent. The period from 2012 to 2014 erased half the industry's market value. The period from 2020 onward has seen at least one more mini-cycle of inventory tightening. In a bad year, a baijiu company's operating cash flow can plunge while its fixed costs — the cellars, the grain contracts, the sales force — stay roughly constant. Owning a stable-dividend bank and a brokerage that earns fees through all phases of the cycle gives the company what private equity investors call "cheap float": a source of non-correlated income that can buffer the dry years.

It is, in a sense, the Berkshire Hathaway logic transposed onto Sichuan provincial finance. Warren Buffett used insurance float to build an investment empire. Luzhou Laojiao uses baijiu float to own pieces of the financial plumbing of its home region.

Did they overpay? The honest answer is that we do not know with precision. The Luzhou Bank stake was accumulated over many years at various valuations; the public disclosures are partial. The Huaxi Securities stake looks, in retrospect, very well-timed — the brokerage sector in China has had a volatile decade, but Luzhou's entry cost was low enough that even through cycles the mark-to-market has been comfortably positive. What matters more than the entry price is the ongoing economic contribution: the dividend streams, the equity-method income, and, not to be underestimated, the political and relationship capital that comes from being a meaningful shareholder in the city's bank.

There is a second-order implication that deserves a short aside. A baijiu company with large stakes in a regional bank and a brokerage sits at the intersection of consumer branding and local financial services in a way that creates both diversification and concentration. Diversification, because the cash flows are not correlated. Concentration, because all of it — the cellars, the bank, the brokerage — is exposed to the economic health of Sichuan and its policy environment. For long-term fundamental holders, the lesson is that the ticker symbol 000568.SZ is a compound bet, not a pure consumer-staples bet.

And then, alongside the financial assets, the company has also poured significant capital into its own physical expansion. The Luzhou Laojiao Intelligent Brewing and Ecological Park, a multi-phase capital project announced in 2016 and executed through the back half of the 2010s and early 2020s, is a roughly one-billion-dollar-scale investment in new-generation production facilities, logistics, and grain-handling infrastructure. It is, in a sense, the opposite of the ancient-cellar story: highly modernized, sensor-driven, designed to scale the mid-premium portfolio. We will come back to this when we discuss the bull case.

For now, the takeaway is that Luzhou Laojiao's balance sheet is a strange hybrid of an ancient-heritage spirits company and a regional financial holding company. It is unusual among global peers. It is, in its own way, deliberate.

VII. Segment Analysis: Beyond the 1573

If you were to draw Luzhou Laojiao's revenue and profit waterfall on a napkin, you would end up with a deeply lopsided picture.

Guojiao 1573, the ultra-premium tier, accounts for roughly sixty percent of revenue and somewhere north of seventy-five percent of gross profit. It is the engine. It is the halo. It is the product to which nearly all of the marketing narrative attaches. The Guojiao sub-portfolio itself splits into several price points — the standard Guojiao 1573, the higher-end "low-alcohol" and special-edition variants, and a small but growing vintage-reserve tier aimed at collectors — but in the mind of the consumer, and in the pricing architecture of the Chinese premium spirits market, "Guojiao" is a single mental shelf.

The mid-tier, branded under the Luzhou Laojiao family, is a completely different business. This is where Tequ, Touqu, and Erqu live — price points that run from roughly the equivalent of ten or fifteen U.S. dollars a bottle to perhaps fifty or sixty. Historically this is the mass-market workhorse, the bottle that shows up at family reunions in small-town Sichuan, at wedding banquets in second-tier cities, at the modest end of the corporate entertainment spectrum. Lower margin, larger volume. The Liu-Lin pruning made this portfolio cleaner than it used to be, but the company is still rebuilding some of the mid-tier's distribution after the pre-2015 SKU explosion.

Then there is a third, much smaller category that the company has been experimenting with over the past few years: "innovation liquors." This is a grab bag of pre-mixed drinks, lower-alcohol baijiu cocktails, fruit-infused variants, and co-branding efforts aimed at younger urban consumers who, to put it bluntly, do not drink traditional baijiu and have no cultural memory of why anyone else does.

This last category is worth lingering on, because it is the most contested piece of the strategic puzzle.

The macro argument for it is straightforward. Traditional baijiu consumption in China skews older and male. The modal consumer is in his forties or fifties, buys premium bottles for gifting, business, or ceremonial dining, and has a complex cultural relationship with the product that includes a tolerance for its very high alcohol content — typically 38% to 52% alcohol by volume, with premium variants usually at 52%. Younger Chinese consumers, particularly urban women under thirty-five, drink less baijiu than their parents did at the same age. They drink more wine, more whisky, more craft beer, and, increasingly, locally-produced sparkling and low-ABV alternatives. If this demographic shift continues for another twenty years unchanged, the addressable market for traditional high-alcohol baijiu shrinks, not grows.

So in 2019 and 2020, Luzhou Laojiao set up an innovation liquor unit, launched several pre-mixed brands, and partnered with various tea-shop and coffee-chain players to co-brand limited-edition drinks. Some of these efforts have been commercial successes, some have flopped, and none of them yet moves the consolidated needle. Management frames the initiative as a ten-year hedge — an option on the future rather than a source of current earnings.

Skeptics will note that the innovation liquor strategy has exactly the right amount of strategic dilution to be worrying. If Luzhou's moat is the ancient cellars and the ceremonial brand, extending the brand downward into ready-to-drink cocktails risks cheapening the association without necessarily winning the new demographic. The counter-argument is that the brand extension is happening under secondary sub-brands, not under Guojiao 1573, and that the risk is therefore contained.

There is a third, subtler segment worth flagging: the export and overseas-Chinese business. Baijiu has, historically, been one of the least-exported major spirits categories in the world. A product that sells forty billion dollars a year in China sells a rounding error outside China. Several of the Big Four, including Luzhou, have spent the past decade attempting, with mixed success, to crack overseas markets — primarily Southeast Asia, the Chinese diaspora in North America and Europe, and a few enthusiastic mixology scenes in London and New York. The contribution to revenue is still small. The optionality, if the category globalizes the way that tequila did in the 2010s, is potentially meaningful.

For the near-term investor, though, the punch line is unchanged. Luzhou Laojiao is a Guojiao 1573 company with some supporting businesses. What happens to the ex-factory price, the ex-factory volume, and the distribution health of Guojiao 1573 determines what happens to the stock.

VIII. The Playbook: Hamilton's 7 Powers & Porter's 5 Forces

Good frameworks do not produce good companies — they reveal the structure of companies that are already either good or bad. With Luzhou Laojiao, they are unusually revealing.

Start with Hamilton Helmer's 7 Powers.

The Cornered Resource power is the dominant one, and we have already discussed it at length. The 1,619 ancient cellars, including the four National Cellar pits dating to 1573, constitute an irreproducible production asset. Any competitor wishing to produce a "450-year-old mud" flavored strong-aroma baijiu has exactly one option: wait 450 years. This is not a hyperbole. It is a statement of biological fact. The Cornered Resource here is about as literal as the framework gets — more literal, arguably, than rights to a rare ore body or exclusive talent, because it is quite literally irreplaceable over any commercial timescale.

Branding is the second and arguably equal power. The invention of the Guojiao 1573 brand in 2001 transformed a commodity producer into a luxury house, and the post-2015 reinvestment in the brand architecture consolidated that transformation. The word "Guojiao" — literally "national cellar" — has a specific cultural weight in Chinese that is difficult to translate. It evokes the Ming Dynasty, national heritage, imperial continuity, ceremonial gravitas. The brand has been built over a quarter-century of consistent positioning, and it is now one of the three or four most recognizable spirits brands in the Chinese-speaking world. You can replicate a factory. You cannot replicate a mental shelf position built by twenty-five years of high-production-value advertising and strategic sponsorship.

Scale Economies are present but more muted than in, say, a global consumer packaged goods company. Within the Sichuan strong-aroma ecosystem, Luzhou's production and distribution scale give it per-bottle cost advantages, particularly in the mid-tier. But the absolute cost floor for producing a bottle of premium baijiu is not the binding constraint on industry profitability; pricing is. The premium tier's margins come from price, not volume economies.

Switching Costs, in the traditional enterprise-software sense, are low. Nobody signs a multi-year contract to drink Guojiao 1573. But there is a cultural switching cost in the gifting-and-banqueting context: once a social circle has conventionalized around a particular brand as the "appropriate" bottle for a class of occasion, deviating from it sends a social signal. That is not a contractual switching cost, but it functions like one.

The remaining Helmer powers — Network Economies, Counter-Positioning, Process Power — are either weak or absent for Luzhou. The company's value is concentrated in the first two powers, and that concentration is a feature, not a bug.

Now turn to Porter's 5 Forces.

Bargaining power of buyers is close to zero at the premium tier. The consumer of a Guojiao 1573 bottle is a gift-giver, a banquet host, a family head marking an occasion. Price elasticity at the consumer level is very low, because the product is as much a social signal as a beverage. Distributors have more leverage than consumers, but the Laojiao Intelligent system has neutered much of their traditional price-negotiation power. In the mid-tier, buyer power is meaningfully higher; consumers there are more price-sensitive and cross-shop across brands.

Bargaining power of suppliers is modest. The key inputs are sorghum, wheat, water, and energy. Sorghum is commoditized; water is the local Yangtze tributary, effectively free; energy is commodity. None of these suppliers has meaningful pricing power over a national-scale distiller.

Threat of new entrants is almost entirely neutralized at the premium tier by the Cornered Resource. A new entrant could, in theory, launch a premium strong-aroma baijiu, but without ancient cellars the product could not compete on flavor with the established incumbents, and without a heritage story it could not charge a premium price. Craft baijiu as a category exists, but it is rounding-error-small and primarily a novelty play. At the mid-tier, the threat is higher but still buffered by distribution and brand.

Threat of substitutes is the most interesting force to debate. In the gifting and banqueting context, baijiu is nearly irreplaceable; presenting a bottle of Scotch at a traditional Chinese business banquet sends an entirely different social signal, and for most occasions the wrong one. Among younger consumers, however, substitutes are very much present — wine, whisky, beer, cocktails, and locally-produced low-ABV alternatives all compete for share of occasion. Whether the substitution pressure accelerates or stabilizes over the next decade is the single biggest variable for the long-run bull case.

Industry rivalry is intense, and localized. The Big Four — Moutai, Wuliangye, Luzhou Laojiao, and Yanghe — compete fiercely for premium share, for distribution, for gifting occasions, and for the mental real estate of the Chinese consumer. But the rivalry has, over the last decade, settled into something closer to a stable oligopoly. The wars are for incremental share within a growing top-tier rather than for survival.

The combined Helmer and Porter picture is of a company with two very strong structural powers, a benign immediate competitive environment, and one substantive long-run demographic risk. That setup frames the bull and bear cases.

IX. Analysis: The Bear vs. Bull Case

The bear case for Luzhou Laojiao is built on three pillars, and each deserves to be taken seriously rather than brushed aside.

The first is demographics. China's total population has been declining since 2022, and the decline is now projected by the National Bureau of Statistics to continue through the century. More importantly for baijiu, the peak of the baijiu-consuming cohort — urban and rural men aged roughly thirty-five to sixty — is also past its maximum and is drifting slowly downward. Younger consumers, as discussed, drink less baijiu per capita than their parents. If per-capita consumption in the core cohort stays flat but cohort size shrinks, volume declines. If younger cohorts never fully adopt the habit, the decline accelerates in the 2030s and 2040s.

The second bear pillar is the so-called "Moutai ceiling." The premium baijiu market has an informal price hierarchy, with Moutai's flagship Feitian bottle sitting at the top and Guojiao 1573 and Wuliangye's Puwu sitting just below. The ceiling matters because in the gifting culture, your bottle cannot cost more than the category leader's bottle and still be read as a premium-but-not-ostentatious gift. If Moutai does not raise its ex-factory price, Luzhou and Wuliangye cannot meaningfully raise theirs either. For most of the late 2010s and early 2020s, Moutai raised prices aggressively, dragging the entire tier up behind it. More recently, Moutai has been measurably more cautious, and the knock-on effect has been a compression of pricing headroom for Guojiao 1573.

The third bear pillar is what could loosely be called "policy overhang." The Chinese regulatory environment for premium consumption has been far more benign since 2016 than it was during the 2012-2014 crackdown, but the possibility of a renewed anti-corruption or anti-luxury push is not zero. Any return of that policy posture would be negative for premium baijiu, perhaps severely so. A secondary policy risk comes from consumption taxes; Chinese liquor consumption taxes have been periodically discussed as a revenue-raising lever, and any material increase would compress margins.

Against these three pillars, the bull case has three of its own.

The first bull pillar is the concentration effect. Chinese baijiu is a historically fragmented industry. The Big Four have been steadily gaining share from regional brands for two decades, and the pace of consolidation accelerated after the 2012-2014 crisis. Even if the total baijiu market stops growing or contracts modestly, the Big Four — and within the Big Four, the top three — can continue to grow by eating the middle and bottom of the industry. This is a classic "disinflationary growth" story in a mature category: shrinking pie, but winners' slices expand.

The second bull pillar is operational leverage from the Intelligent Brewing Park and the Laojiao Intelligent distribution platform. These investments, costly when made, are now in the harvesting phase. Production cost per bottle has a downward trajectory; distribution visibility reduces inventory-cycle volatility; marketing spend has higher return per dollar as the brand architecture has stabilized. The Liu-Lin playbook has produced a measurable structural improvement in the company's margin profile that is unlikely to reverse.

The third bull pillar is valuation. Relative to Moutai, Luzhou Laojiao trades at a meaningful discount on forward earnings multiples. Some of that discount is justified — Moutai's scarcity and pricing power are better — but the gap has historically been a useful barometer. Investors who view Luzhou as the "second-best" premium baijiu with the second-strongest brand have generally been compensated for the risk premium over multi-year periods. ROE has run in the thirty-to-forty-percent range in recent years, which, combined with modest leverage, is comparable to Moutai's on an asset-efficiency basis even if the pricing power is a notch lower.

The question many sophisticated investors ask is whether Luzhou Laojiao is a better investment than Moutai. That question does not have a single right answer, and we will not try to give a specific verdict. What can be said is that the two companies are not substitutes from a portfolio construction standpoint. Moutai is the category's defining incumbent, with the deepest moat and the tightest supply. Luzhou is the category's disciplined challenger, with a genuinely distinctive asset (the cellars), a proven management team, and a valuation that reflects the extra execution risk. How you weight cellars versus distillery, brand versus scarcity, and challenger valuation versus category-leader safety is a question of temperament as much as analysis.

A brief aside on what to watch from a due-diligence standpoint. The most important ongoing signals for Luzhou's trajectory are three: the ex-factory and secondary-market transaction price of Guojiao 1573 (which, unlike the listed price, reveals real demand health), the inventory-to-sales ratio at the distributor level (which shows whether channel stuffing is returning), and the gross margin trajectory of the premium segment (which is the cleanest summary of pricing power). These three KPIs, more than any macro narrative, tell you in real time whether the Liu-Lin model is still working.

X. Epilogue

Stand again at the edge of National Cellar No. 1, in the late afternoon light, and consider what that mud has witnessed.

When the first batch of sorghum was sealed into that pit in 1573, the Ming Dynasty had about seventy more years on its clock. The cellar was already a hundred and fifty years old when the Qing collapsed. It was three centuries old when the Qing's own successor state declared a republic. It was four hundred years old when the founders of the People's Republic were fighting their civil war. The cellar has outlived dynasties, regimes, and ideologies. It has been owned by a family, by a collective, by a city, and, through the listed vehicle, by anyone in the world with access to the Shenzhen Stock Exchange who can stomach the accompanying geopolitical and currency risks.

For most of that long history, the cellar was a production asset, nothing more. It made liquor. It did not make a brand. The extraordinary thing about the modern era of Luzhou Laojiao, and the central insight the company has supplied to the rest of the Chinese consumer-goods industry, is that heritage is a liability until you turn it into a brand. A 450-year-old fermentation pit, sitting in the ground, doing nothing more than fermenting grain, is a curiosity. A 450-year-old fermentation pit explicitly marketed as the foundation of the world's most culturally-loaded baijiu brand is a thirty-billion-dollar equity story.

The 2024 and 2025 results extended the Liu-Lin narrative, with continued single-digit-plus revenue growth through a softer macro environment and stable premium segment margins, although the pace of growth has clearly moderated from the breathless levels of 2019-2022. The Intelligent Brewing Park has come further online. The equity incentive grants have progressed through their vesting schedule. Liu Miao and Lin Feng remain in place as of this writing, now a decade into a turnaround that, in 2015, many outside observers considered improbable. Chinese baijiu watchers have begun to take the Liu-Lin era as a reference case — the template that other second-tier SOE consumer companies, from tea to dairy to traditional medicine, are studying for their own transformations.

Whether the next decade continues the trajectory depends, in order of importance, on three things: whether the premium baijiu category can defend its cultural relevance against generational substitution, whether the Moutai ceiling rises or stays flat, and whether Liu, Lin, and their internal successors can hold discipline on distribution, pricing, and brand — the three pillars that separate the Liu-Lin era from the Xie Ming era before it.

One of the quiet ironies of the Luzhou Laojiao story is that the single most modern thing about the company — the digital distribution platform, the data-driven pricing defense, the equity-aligned management team — is what protects the single most ancient thing about the company. The mud does its work only if the bottle it produces can reach the consumer at the price the brand commands. That is the real job of the corporate machine sitting on top of four-century-old fermentation pits. And for the first time in a long time, it looks like a machine built to run.

The 450-year-old startup is still, apparently, a startup.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube