Kia Corporation: Movement That Inspires (and Outprofits)

I. Introduction: The Most Unlikely Champion

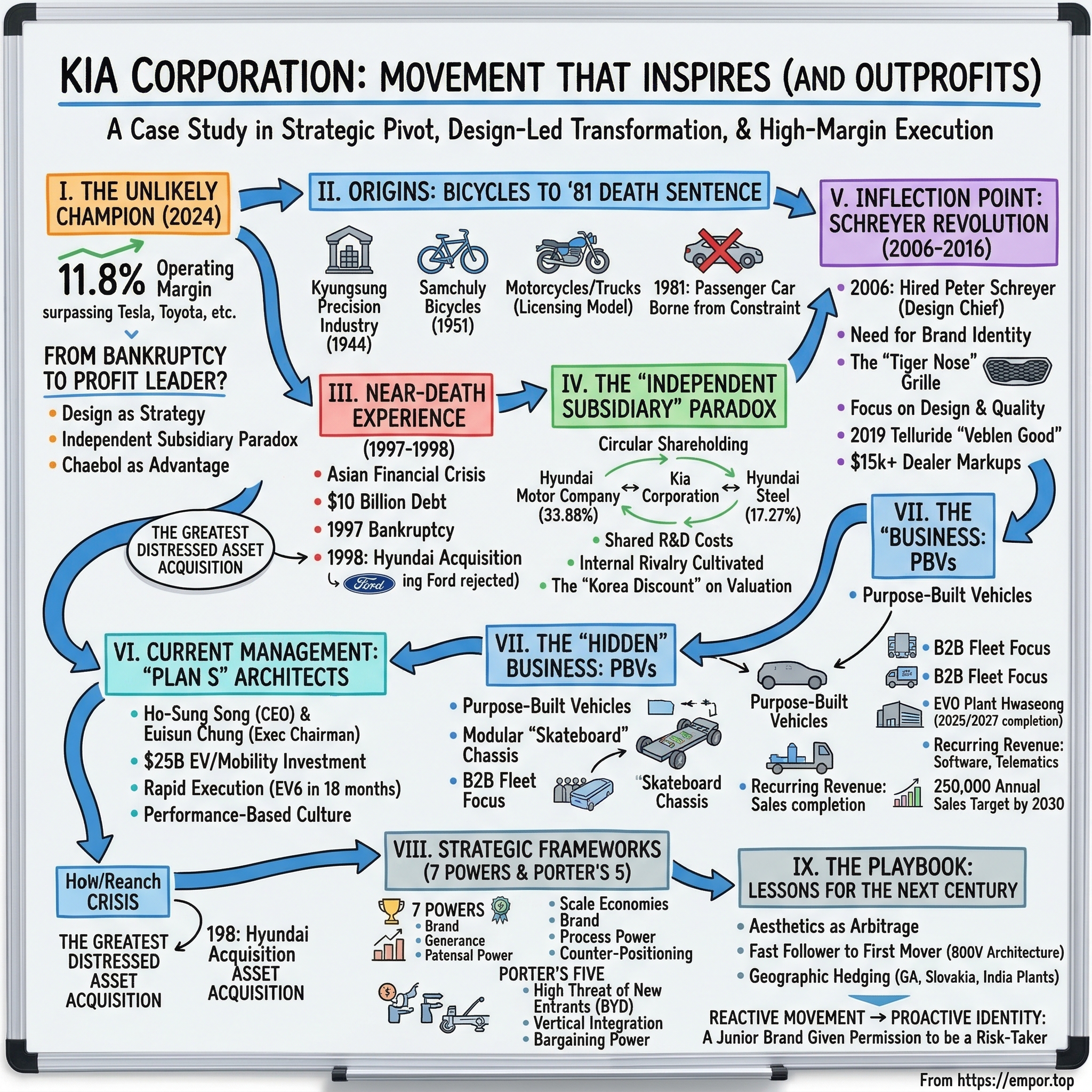

In the summer of 2024, a number landed on the desks of auto analysts that made some of them do a double take. Kia Corporation—yes, the company whose name was once shorthand for "cheap Korean car"—posted an operating profit margin of 11.8% on over 3 million vehicles sold. That figure surpassed Tesla. It surpassed Toyota. It surpassed BMW and Mercedes-Benz. It even surpassed Hyundai Motor, the very parent company that had rescued Kia from bankruptcy less than three decades earlier. Kia earned roughly 4.1 million Korean won—about $3,100—on every single vehicle it sold. For a mass-market automaker, that number was extraordinary.

How does a company that was stone-cold bankrupt in 1997, carrying nearly ten billion dollars in debt, become the most profitable volume automaker on the planet? The easy answer is "good cars." The real answer is far more interesting.

Kia's story is not simply an automotive turnaround. It is one of the great case studies in design as corporate strategy, in the paradox of the "independent subsidiary," and in what happens when a conglomerate gives its second-tier brand permission to be the risk-taker. Kia went from manufacturing bicycle tubes under Japanese occupation to building the EV6, the first vehicle on an 800-volt architecture to win European Car of the Year. It went from being forced by a military government to stop making passenger cars entirely to designing the Telluride—a vehicle so coveted that American dealers were charging $15,000 over sticker price for a car with a Kia badge on it.

The thesis here is simple: Kia is the ultimate "ugly duckling" story in global industry, and the transformation was neither accidental nor inevitable. It was the product of a single bet on design, a unique structural position within the Hyundai Motor Group, and a management team that figured out how to turn the constraints of the Korean chaebol system into competitive advantages. The playbook that emerges—from bicycle parts to purpose-built electric vehicles—holds lessons for anyone trying to understand how brands are built, how incumbents adapt, and how a company can change the way the world perceives it in less than a generation.

The story begins, as many Korean industrial stories do, in the ashes of war.

II. Origins: Bicycles, Steel, and the 1981 "Death Sentence"

Seoul, 1944. The Pacific War was grinding toward its end, and Korea remained under Japanese colonial rule. In that year, a small enterprise called Kyungsung Precision Industry began operating in Seoul, producing steel tubing and bicycle parts. It was about as modest a beginning as one could imagine for what would become a global automotive powerhouse. But in the context of 1940s Korea—a nation that had virtually no industrial base of its own, where most manufacturing capacity had been built by and for the Japanese occupiers—even making steel tubes was an act of industrial ambition.

When Korea gained independence in 1945, and then endured the devastating Korean War from 1950 to 1953, the young company pivoted to what the ruined country needed most: transportation. In 1951, Kyungsung produced South Korea's first domestically manufactured bicycle, branded "Samchuly." It is difficult to overstate what that meant in a country where most of the population had no motorized transport whatsoever. The Samchuly bicycle became a fixture of Korean life—the delivery tool of shopkeepers, the commuter vehicle of factory workers, the symbol of a nation beginning to rebuild. Kia, before it was Kia, put Korea on wheels.

By the late 1950s, the company had moved beyond human-powered transport. In 1957, it began manufacturing motorcycles under a license from Honda—learning Japanese precision manufacturing from the inside. By 1962, it was building trucks under a Mazda license. This was the classic Asian industrial development model: learn by licensing, absorb the manufacturing know-how, build your own capability over time. Kia was "standing on the shoulders of giants," and it was getting stronger with every passing year. Through the 1970s, the company produced the Mazda-derived Brisa range of passenger cars for the domestic market, steadily expanding its capabilities.

Then came the moment that nearly killed Kia—and, paradoxically, made it stronger.

In 1981, South Korea was under the military government of Chun Doo-hwan, and the regime decided that the country's auto industry was overcrowded. In a move that would be unthinkable in a Western market economy, the government issued an industrial consolidation decree: only three companies would be permitted to manufacture passenger cars. Kia was not one of them. The company was ordered to stop making cars entirely and focus exclusively on light trucks. It was, effectively, a death sentence for Kia's passenger car ambitions.

But here is the twist that rarely gets told. The forced specialization in light trucks created something unexpected: a lean, disciplined manufacturing culture that prioritized efficiency and durability over style or prestige. While Hyundai and Daewoo were building passenger sedans and chasing consumer brand recognition, Kia was perfecting the art of building reliable, no-nonsense commercial vehicles. The Besta van, the Sportage (which Kia would eventually develop into one of its signature models)—these products were born from a culture forged in constraint. When the Korean government finally re-liberalized the auto market in the late 1980s and Kia was allowed to make passenger cars again, the company re-entered with a manufacturing base that was leaner and more cost-efficient than almost anyone realized.

The company officially became Kia Motors Corporation in 1990, and its global export ambitions were beginning to take shape. But the seeds of catastrophe were already being sown. Like many Korean chaebols of the era, Kia began expanding recklessly—into steel, into construction, into businesses far removed from its core competency. The debt was piling up. The reckoning would arrive with shocking speed, and it would take the entire Asian economy down with it.

III. The Near-Death Experience (1997–1998)

The story of Kia's bankruptcy is inseparable from the story of the Asian Financial Crisis, and to understand what happened, one needs to understand the peculiar logic of the Korean chaebol in the mid-1990s. Chaebols—the family-controlled industrial conglomerates that dominated the Korean economy—operated on a simple principle: growth at all costs, funded by debt. Banks lent freely because chaebols were "too big to fail." Chaebols borrowed freely because banks never said no. It was a system that worked brilliantly during Korea's decades of rapid industrialization—and catastrophically when the music stopped.

By the mid-1990s, Kia had diversified well beyond automobiles. The company had interests in steel, construction, and various industrial ventures. It had become the seventh-largest chaebol in South Korea. And it was carrying approximately $10 billion in debt—a staggering sum for a company whose core business was building affordable cars and trucks.

The dominoes started falling in January 1997 when Hanbo Steel, a mid-tier chaebol, collapsed under $6 billion in debt. The bankruptcy sent shockwaves through the Korean financial system. Creditors began tightening. Investors began fleeing. By the summer of 1997, Kia—overextended, over-leveraged, and suddenly unable to refinance—tipped into bankruptcy protection. The date was July 15, 1997, and it was only the beginning. Within months, the broader Asian Financial Crisis would engulf Thailand, Indonesia, Malaysia, and Korea itself, forcing Seoul to accept a humiliating $58 billion bailout from the International Monetary Fund.

What followed for Kia was a government-supervised auction that pitted two very different suitors against each other.

In one corner was Ford Motor Company. Ford had actually held an equity stake in Kia since 1986—roughly 10%—and the two companies had a deep manufacturing relationship. The Kia Pride, a small car based on a Mazda design, had been rebadged and sold in North America as the Ford Festiva. Ford knew Kia's factories, knew its capabilities, and saw an opportunity to acquire a low-cost Asian manufacturing base at fire-sale prices.

In the other corner was Hyundai Motor Company, Korea's largest automaker and itself a chaebol under significant financial pressure. Hyundai's interest in Kia was strategic rather than opportunistic. Acquiring Kia would give Hyundai a second brand, a broader product range, and—critically—the manufacturing capacity and scale economies needed to compete globally against Toyota, Volkswagen, and General Motors.

Hyundai won. In 1998, Hyundai acquired a 51% controlling stake in Kia for roughly $940 million—just under a billion dollars. The stake was split across several Hyundai Group entities, with Hyundai Motor itself taking about 20%.

With the benefit of hindsight, this was one of the greatest distressed-asset acquisitions in industrial history. Consider the comparison: in 1989, Ford paid $2.5 billion for Jaguar. In 2000, Ford would pay $2.7 billion for Land Rover. Combined, Ford spent well over $5 billion on two niche premium brands that it would eventually sell to Tata Motors at a loss. Hyundai, for less than a billion dollars, acquired a fully functional mass-market automaker with manufacturing plants, a global dealer network, and—most importantly—a brand that could be repositioned rather than rebuilt from scratch.

The marriage was born of necessity, not romance. Kia's workers feared absorption. Hyundai's management viewed Kia as a fixer-upper. But the structure that emerged—Kia as a semi-autonomous subsidiary with its own brand identity, its own design philosophy, and its own management team, sharing platforms and powertrains with Hyundai underneath—would prove to be one of the most effective multi-brand strategies in the global auto industry. It would take nearly a decade for the full potential of this structure to become apparent, but the foundation was laid in the wreckage of the Asian Financial Crisis.

For investors, the Kia bankruptcy and acquisition story contains a timeless lesson about distressed assets: the best deals happen when a structurally sound business is trapped inside a broken balance sheet. Hyundai did not buy a broken car company. It bought a capable manufacturer with a liquidity problem, at a price that reflected the liquidity problem rather than the manufacturing capability.

IV. The "Independent Subsidiary" Paradox

To understand how Kia operates today—and why it can move faster than most automakers its size—one must understand the peculiar architecture of the Hyundai Motor Group. It is a structure that confuses Western investors, frustrates governance activists, and yet produces results that are difficult to argue with.

The chaebol system runs on circular shareholding, and the Hyundai-Kia web is a textbook example. Hyundai Motor Company owns approximately 33.88% of Kia Corporation. Kia, in turn, owns about 17.27% of Hyundai Steel. Hyundai Steel owns roughly 5.66% of Hyundai Mobis (the group's massive auto parts supplier). And Hyundai Mobis owns over 21% of Hyundai Motor Company. Follow the arrows and you trace a circle: HMC controls Kia, which partly controls Hyundai Steel, which partly controls Hyundai Mobis, which partly controls HMC. At the center of this web sits the Chung family—specifically Executive Chairman Euisun Chung—who maintains effective control of the entire group despite holding relatively modest direct equity stakes.

Western governance purists hate this structure, and not without reason. Circular shareholdings insulate management from market discipline, make it difficult for minority shareholders to exercise influence, and create potential conflicts of interest. This is a significant contributor to the "Korea discount"—the persistent gap between what Korean companies earn and what the market is willing to pay for those earnings. Kia trades at roughly 4 times trailing earnings, compared to 10-12 times for Toyota and 5-6 times for Volkswagen, despite having superior margins.

But here is the paradox: the very structure that depresses Kia's stock price is also what allows Kia to operate with unusual strategic agility. Because Kia is not a standalone company competing in the public market for every dollar of R&D spending, it can share the enormous fixed costs of platform development with Hyundai while maintaining its own brand identity. The E-GMP electric vehicle platform, the 800-volt charging architecture, the Smartstream engine family—all of these were developed jointly by Hyundai and Kia, with the costs amortized across both brands. This means Kia effectively gets to spend like a company twice its size on R&D while maintaining the marketing nimbleness of an independent brand.

The internal rivalry between the two brands is real and deliberately cultivated. Hyundai positions itself as the "sophisticated, premium" sibling—think Genesis, the luxury sub-brand. Kia positions itself as the "youthful, design-forward" rebel. They share platforms, they share engines, they share suppliers—but they compete fiercely for customers, for dealer attention, and for media coverage. It is a two-brand strategy that global competitors like Stellantis (with its sprawling portfolio of 14 brands) and Renault-Nissan have struggled to replicate with anything like the same efficiency.

The analogy that comes closest is probably Apple and its supply chain. Apple does not own its chip fabrication plants or its assembly lines—but it controls the design and captures the margin. Kia does not independently develop every powertrain or platform—but it controls the design language, the brand positioning, and the customer experience, and it captures margin that rivals its parent.

For the long-term investor, the structural question is whether the Korea discount will narrow. South Korea's government launched a "Corporate Value-Up Program" in 2024, modeled on Japan's successful push to improve corporate governance and shareholder returns. Kia has responded by increasing dividends and share buybacks. But the circular shareholding structure remains intact, and until it is unwound—or until global investors simply decide that 4 times earnings is too cheap for an 11.8% margin business—the discount is likely to persist. The question is not whether Kia is a good business. It clearly is. The question is whether the market will ever give it credit for being one.

V. The Inflection Point: The Schreyer Revolution (2006–2016)

In 2006, Kia had a problem that no amount of engineering excellence could solve. The cars were fine. The reliability was improving. The prices were competitive. But nobody cared. Kia had what the industry calls a "neutral image"—it was not disliked, but it was not desired either. In consumer surveys, Kia ranked near the bottom on brand desirability, just above the generics. People bought Kias because they were cheap, not because they wanted one. For a company trying to grow margins and move upmarket, this was an existential problem.

The man who would change everything was not Korean. He was a quiet, bespectacled German named Peter Schreyer, and he was, at the time, one of the most celebrated automotive designers in the world. His masterpiece was the original Audi TT—a car so iconic that it single-handedly elevated Audi from "the other German luxury brand" to a design-led competitor for BMW and Mercedes. Schreyer had spent decades at the Volkswagen Group, rising through exterior design, interior design, and conceptual design roles. He understood, at a molecular level, how design could transform a brand's perceived value.

The recruitment was personal. Euisun Chung—then president of Kia, now Executive Chairman of the entire Hyundai Motor Group—flew to Germany to make the pitch himself. The message was blunt: Kia needs a face. It needs an identity. It needs a reason for someone to choose it over a Honda Civic or a Toyota Corolla beyond price. Chung gave Schreyer something that most corporate design chiefs never receive: a blank canvas and a mandate from the top.

Schreyer's first major public statement was the Kee concept car, unveiled at the 2007 Frankfurt Motor Show. The car itself was striking, but the real debut was a single design element: the "Tiger Nose" grille. It was a bold, concave grille shape—wide at the top, narrowing to a point at the bottom—that Schreyer intended to become Kia's universal identifier. "Kia had no face," Schreyer later explained. "I wanted a powerful visual signal, a seal, an identifier." He wanted someone to be able to recognize a Kia from a hundred meters away, the way you could recognize a BMW kidney grille or a Jeep seven-slot.

The Tiger Nose rolled out across the entire Kia lineup over the next several years. The Optima sedan. The Sportage SUV. The Soul hatchback. The Rio. Each vehicle received the new design language, and with each new model, the cumulative effect grew stronger. Something was happening that almost never happens in the auto industry: a budget brand was becoming a design brand.

The data told the story. Kia's average transaction prices began climbing. Quality scores improved in parallel—Kia invested heavily in fit-and-finish to match the new design ambitions. By the mid-2010s, Kia was regularly appearing in J.D. Power's top rankings for initial quality, a dramatic reversal from its reputation a decade earlier. The company was no longer winning on price alone; it was winning on the combination of design, quality, and value that represents the sweet spot of the mass market.

But the true vindication—the moment when the Schreyer revolution proved it could produce a genuine halo product—came in 2019 with the Telluride.

The Telluride was unlike anything Kia had ever attempted. It was a full-size, three-row SUV designed at Kia's design center in Irvine, California, specifically for the American market. It was built at Kia's plant in West Point, Georgia. It was, in every sense, an American truck—conceived, designed, and manufactured for the customers who would buy it. And it was beautiful. Not beautiful-for-a-Kia. Beautiful, period.

The response was immediate and astonishing. The Telluride swept the 2020 awards season, becoming the first SUV in history to win the "Triple Crown": North American Utility Vehicle of the Year, MotorTrend SUV of the Year, and a spot on Car and Driver's 10 Best list. It also won 2020 World Car of the Year. Demand so outstripped supply that dealers began charging markups of $5,000 to $18,000 over MSRP. Some dealers were reported asking nearly $80,000 for a vehicle with a base price in the mid-$30,000s.

Think about what that means. A Kia—a brand that a decade earlier was the punchline of automotive jokes—had become a Veblen good. People were paying above sticker price for the privilege of owning one. That is the power of design as strategy. Peter Schreyer took a commodity and turned it into an object of desire, and in doing so, he proved that aesthetics is one of the most underappreciated forms of competitive advantage in industrial business.

Schreyer would eventually be named President of Hyundai-Kia—the first designer ever to hold such a rank at a major automaker. His legacy is not just the Tiger Nose or the Telluride. It is the proof of concept that a "neutral image" brand can be transformed into a design leader in a single decade, if the commitment comes from the very top of the organization.

The design revolution had given Kia a brand. Now the company needed a strategy for the electric future. And for that, it would need a new kind of leader.

VI. Current Management: The "Plan S" Architects

When Ho-Sung Song was appointed President and CEO of Kia in March 2020, the timing could hardly have been worse—or, depending on your perspective, better. The world was weeks away from a global pandemic that would upend the auto industry's supply chains, accelerate the shift to electric vehicles, and fundamentally change how consumers thought about mobility. Song, a career Kia executive born in 1962 in Jeonju, was an unlikely revolutionary. He had studied French Language and Literature at Yonsei University—not engineering, not business—and had built his career in the less glamorous corridors of export planning and regional operations. He had served as President of Kia Motors Europe and Head of Global Business Management. He was, in the best sense, an operations guy who understood how to sell cars in markets that most Korean executives considered secondary.

That background turned out to be precisely what Kia needed. Song's appointment coincided with the launch of "Plan S"—announced in January 2020, just weeks before the pandemic hit—which represented the most ambitious strategic pivot in Kia's history. The original plan called for investing 29 trillion Korean won, roughly $25 billion, by the end of 2025 to transform Kia from an internal-combustion-engine-centric company into an EV-centric one. This was not a hedge or a toe-in-the-water. It was a wholesale strategic reorientation, announced at a time when global EV penetration was still in the low single digits.

Song's approach was notably different from the traditional Korean chaebol management style. The old model was rigid seniority—you advanced based on tenure, not performance, and strategic decisions flowed top-down from the founding family. Song introduced a more performance-based culture, empowering regional leaders and accelerating decision cycles. The results showed up in execution speed. Kia went from announcing its EV strategy to delivering the EV6—a world-class electric vehicle on an entirely new platform—in roughly 18 months. By comparison, legacy automakers like Volkswagen and General Motors took years longer to bring their dedicated EV platforms to market.

The man who put Song in the role—and who continues to shape Kia's strategic direction from above—is Euisun Chung, the Executive Chairman of the entire Hyundai Motor Group. Chung is the son of Hyundai's legendary founder-era chairman Chung Mong-koo, but he is no passive inheritor. By all accounts, Euisun Chung is an intensely hands-on leader with a particular passion for technology and a willingness to make bets that his peers consider outlandish. It was Chung who personally recruited Peter Schreyer. It was Chung who pushed for the 800-volt architecture in Kia's EVs when the rest of the industry was still debating whether to go beyond 400 volts. And it was Chung who orchestrated the Hyundai Motor Group's $880 million acquisition of an 80% controlling stake in Boston Dynamics in 2021, along with the creation of Supernal, the group's electric air taxi subsidiary targeting commercial service by 2028.

Kia, within this structure, serves as something of a testing ground for Chung's most radical ideas. The PBV (Purpose-Built Vehicle) strategy, which represents a fundamental rethinking of what a car company can be, originated within Kia. The aggressive push into 800-volt charging, which gives Kia's EVs a meaningful technical advantage over most competitors, was championed by Chung and executed through Kia first.

Song's management of this portfolio has earned him the confidence of the board. In March 2025, he was reappointed to a third term as CEO, extending his tenure through 2028. At the 2025 CEO Investor Day, Song unveiled an updated strategic plan: invest 42 trillion won from 2025 through 2029, targeting 4.19 million global sales by 2030 including 1.26 million EV units and 2.33 million combined hybrid and EV units. The revenue target: 170 trillion won by 2030, with operating profit margins sustained above 10%.

Those targets are ambitious but not unreasonable given Kia's trajectory. In 2024, Kia crossed the 100-trillion-won revenue threshold for the first time in its history, posting 107.45 trillion won with an operating margin of 11.8%. The challenge facing Song and his team is maintaining those margins through the EV transition—a period when most automakers are seeing margins compress due to the high cost of battery technology and the price war being waged by Chinese competitors.

The leadership team's answer to that challenge is not to retreat from electrification but to diversify the revenue base—particularly through a business segment that most retail investors have barely noticed.

VII. The "Hidden" Business: PBVs (Purpose-Built Vehicles)

Somewhere in Hwaseong, South Korea, about 40 kilometers south of Seoul, a factory is rising that represents Kia's bet on the future of commercial mobility. It is not a car factory in any traditional sense. It is the EVO Plant—the world's first dedicated production facility for Purpose-Built Vehicles, and it is designed to manufacture a category of vehicle that does not yet have a clear parallel in the automotive industry.

Purpose-Built Vehicles, or PBVs, are modular electric vehicles built on a "skateboard" chassis—a flat platform containing the battery, motors, and drivetrain—onto which different body configurations can be mounted depending on the use case. Think of it as a LEGO base plate for commercial mobility. The same platform can support a last-mile delivery van for Amazon or Coupang, a ride-hailing vehicle for Uber or Kakao, a mobile medical clinic, a food truck, or a mobile office. The body is customizable; the platform is standardized.

This is a fundamentally different business model from selling SUVs to consumers. PBVs are B2B products sold to fleet operators, logistics companies, and ride-hailing platforms. They are high-utilization assets—driven hundreds of miles per day, every day—which means they need to be durable, easy to maintain, and optimized for total cost of ownership rather than curb appeal. And because they are fleet vehicles, the sales cycle is different: instead of marketing to millions of individual consumers, Kia is negotiating with dozens of large corporate buyers who care about unit economics, service contracts, and software integration.

The Hwaseong EVO Plant is being built in two phases. Phase 1, the EVO Plant East, was completed in November 2025 with capacity for 100,000 units per year, producing the PV5—a mid-size PBV that is the first vehicle in the lineup. Phase 2, the EVO Plant West, broke ground and is scheduled to begin operations in 2027, adding capacity for 150,000 units per year of larger models including the PV7. When both phases are running, the plant will have a combined annual capacity of 250,000 PBVs. The total investment: approximately 4 trillion won.

The product roadmap extends beyond the PV5 and PV7. Kia plans to introduce the PV1 (a smaller urban delivery vehicle) and the PV9 (a large-format PBV) by 2029, along with a PBV Conversion Centre that will allow third-party customizers to build specialized configurations on Kia's platforms. The company has also launched the Tasman, a pickup truck targeting global markets with an 80,000-unit annual sales target.

Why does this matter for investors? Because PBVs represent a potentially high-margin, recurring-revenue business that is structurally different from the cyclical consumer auto market. Fleet customers sign multi-year contracts. They value reliability and total cost of ownership over brand prestige, which plays directly to Kia's manufacturing strengths. And the software integration layer—fleet management, telematics, predictive maintenance—creates opportunities for ongoing service revenue that does not exist in the one-time-sale model of consumer vehicles.

Kia's target is 250,000 annual PBV sales by 2030, concentrated initially in Europe and Korea. If the average selling price and margin profile of these vehicles is anywhere near what Kia achieves on its consumer EVs, PBVs could represent a meaningful new profit pool. The risk, of course, is execution: building a new vehicle category from scratch, establishing a new sales channel, and competing against established commercial vehicle manufacturers (not to mention Amazon, which builds its own delivery vans through Rivian). But Kia has two advantages that are difficult to replicate: the scale economies of the Hyundai Motor Group's supply chain, and a manufacturing culture forged in eight decades of building vehicles for demanding, cost-conscious customers.

The PBV business is the clearest expression of a broader strategic truth about Kia: this is no longer just a car company. It is a mobility platform company that happens to make excellent consumer vehicles. Whether the stock market recognizes that transformation is another question entirely—which brings us to the framework for evaluating Kia's competitive position.

VIII. Hamilton's 7 Powers and Porter's 5 Forces

To truly assess whether Kia's current profitability is sustainable or merely a cyclical peak, it helps to apply two of the most rigorous frameworks in competitive strategy.

Starting with Hamilton Helmer's 7 Powers—the framework that asks "what gives a business durable competitive advantage?"—Kia's position is stronger than most observers appreciate, though not without vulnerabilities.

Scale Economies represent perhaps Kia's single greatest structural advantage, and they are somewhat hidden because they operate at the group level rather than the brand level. Kia does not bear the full cost of developing the E-GMP electric vehicle platform, the Smartstream engine family, or the advanced driver-assistance software that goes into every vehicle. Those costs are shared with Hyundai Motor. This means Kia amortizes its R&D investment across a much larger production base than its own 3.1 million units would suggest—effectively, it gets the R&D spending of a 7-million-unit automaker while operating as a 3-million-unit brand. This is the same structural advantage that Volkswagen Group theoretically has across its portfolio of brands, but Hyundai-Kia executes it with significantly less organizational complexity.

Brand is where the Schreyer revolution pays its deepest dividends. Helmer would classify Kia's design team as a "Cornered Resource"—a unique asset that competitors cannot easily replicate. You cannot buy taste; you cannot hire your way to a coherent design language overnight. The combination of Schreyer's legacy, Kia's design centers in Frankfurt, Irvine, Seoul, and Tokyo, and the institutional commitment to design-led product development represents decades of accumulated capability. The Telluride, the EV6, the EV9—these are not one-off hits. They are products of a design system that consistently produces vehicles people want to own, not just vehicles people settle for.

Process Power manifests in what insiders call the "Hyundai Way" of manufacturing. The Hyundai Motor Group is among the most vertically integrated automakers in the world. It makes its own steel through Hyundai Steel. It makes its own parts through Hyundai Mobis. It makes its own transmissions, engines, and increasingly its own battery components. This extreme vertical integration reduces dependence on external suppliers, shortens development cycles, and allows the group to capture margin at every stage of the value chain. When Kia reports an 11.8% operating margin, that number reflects the efficiency of an entire vertically integrated ecosystem, not just a single assembly operation.

Counter-Positioning is relevant in the context of the EV transition. Kia's aggressive commitment to 800-volt architecture—which enables ultra-fast charging speeds that most competitors cannot match—represents a genuine technological bet that legacy automakers have been slow to follow. The EV6 can charge from 10% to 80% in approximately 18 minutes on a 350-kilowatt charger. Most competing EVs from Toyota, Volkswagen, and General Motors use 400-volt systems that charge significantly slower. This creates a real switching cost for tech-savvy buyers: once you experience 800-volt charging, going back to a 400-volt car feels like going from fiber internet to DSL.

On the weaker side of the 7 Powers, Network Effects are essentially absent in the traditional auto business (though the PBV software ecosystem could eventually create mild network effects in fleet management). And Switching Costs in the consumer auto market remain low—people change car brands with every purchase cycle.

Turning to Porter's Five Forces, the picture is more nuanced.

The Threat of New Entrants is the force that keeps Kia's management up at night, and it has a name: BYD. The Chinese electric vehicle giant has surged to roughly 16.6% global EV market share, and it is aggressively expanding into precisely the markets where Kia has built its growth—Europe, Southeast Asia, Latin America, and potentially India. BYD is itself vertically integrated (it builds 75-80% of its components internally, including batteries and semiconductors) and its pricing is ferociously competitive. Chinese competitors Chery and Changan have already surpassed Hyundai-Kia in some global sales rankings. BYD's EU sales surged 272% while traditional brands stagnated. This is the single most significant competitive threat Kia faces over the next decade.

Bargaining Power of Suppliers is low, precisely because of the vertical integration discussed above. When you make your own steel, your own parts, and your own key components, suppliers have limited leverage over your cost structure. This is a structural advantage that Kia shares with BYD—and that competitors like Stellantis, which depend heavily on external suppliers, lack.

Bargaining Power of Buyers is moderate. In the consumer market, individual buyers have limited power—no single customer matters to a company selling 3 million cars. But in the emerging PBV business, Kia will be selling to large fleet operators who can negotiate aggressively on price and terms. Managing this dynamic will be critical to the PBV segment's margin profile.

Threat of Substitutes is evolving. Urban ride-hailing, car-sharing, and improved public transit in some markets could reduce individual car ownership over time. Kia's PBV strategy is, in part, a hedge against this trend—if people stop buying cars, someone still needs to build the vehicles that transport them.

Competitive Rivalry is intense and will remain so. The global auto industry is consolidating around a handful of players who have the scale to invest in electrification, autonomous driving, and software. Kia's position within the Hyundai Motor Group gives it the scale to compete; its design-led brand identity gives it the differentiation to charge a premium; and its manufacturing efficiency gives it the margins to fund continued investment. But the rivalry—particularly from Chinese manufacturers who are building equivalent products at lower cost—is the defining challenge of the next era.

For investors tracking Kia's ongoing competitive position, the two KPIs that matter most are: operating profit margin (which captures whether Kia can maintain its pricing power and cost discipline through the EV transition) and EV mix as a percentage of total sales (which measures the pace and success of the electrification shift that will define the company's relevance in 2030 and beyond). A third metric worth watching is average selling price per vehicle, which serves as a real-time readout on whether the brand continues to command premium pricing or is being forced to compete on discounts.

IX. The Playbook: Lessons for the Next Century

The Kia story distills into three strategic lessons that extend well beyond the automotive industry.

The first is that aesthetics is an arbitrage opportunity. In any commoditized industry—cars, smartphones, home appliances, financial services—the product that looks and feels different can charge a premium even when the underlying technology is similar. Peter Schreyer's Tiger Nose grille did not make Kia's engines more powerful or its suspensions more refined. It made the cars desirable. And desirability, in a world of functionally equivalent products, is the most underpriced asset a company can build. The lesson applies to any business where the product is becoming commoditized: invest in design before you invest in discounts.

What makes this lesson particularly powerful in Kia's case is the speed of the transformation. In 2006, Kia had a "neutral image." By 2019, dealers were charging $15,000 markups on the Telluride. That is a 13-year brand transformation—fast by any standard, but astonishingly fast in the auto industry, where brand perceptions typically take generations to change. The key ingredient was not just hiring a great designer; it was giving that designer the authority to impose a consistent design language across every product in the lineup, with unwavering support from the top of the organization. Most companies hire great designers and then overrule them with committee decisions. Euisun Chung did the opposite: he hired Schreyer, gave him a mandate, and defended that mandate against internal resistance. That organizational commitment is the part of the Kia story that is hardest to replicate.

The second lesson is the transition from "fast follower" to "first mover." For most of its history, Kia was a fast follower—licensing Honda motorcycles, building Mazda trucks, studying Toyota's manufacturing system. There is no shame in this; it is how most successful Asian industrial companies were built. But the EV transition presented an opportunity to leapfrog, and Kia seized it. By committing to 800-volt architecture in the EV6—a technology that allows charging speeds roughly twice as fast as the 400-volt systems used by most competitors—Kia moved ahead of Toyota, Volkswagen, and General Motors on a dimension that genuinely matters to consumers. Toyota's first dedicated EV platform would not arrive for years after the EV6's launch. Volkswagen's MEB platform used 400-volt architecture. Kia's willingness to bet on unproven-at-scale technology, enabled by the shared R&D resources of the Hyundai Motor Group, turned the former fast follower into a genuine technology leader.

The third lesson is geographic hedging. Kia manufactures vehicles on three continents: Georgia in the United States, Zilina in Slovakia, and Anantapur in India, in addition to its Korean plants. Each facility was established to serve its regional market directly, reducing exposure to currency fluctuations, trade barriers, and tariffs. The Georgia plant—a $3.2 billion cumulative investment producing over 350,000 vehicles per year—has been particularly strategic, shielding Kia from the U.S. tariffs that have hammered competitors who import vehicles from Asia. The Slovakia plant, capable of building up to eight different models on a single production line, serves as the hub for European operations. The India plant, opened in 2019 with 300,000-unit annual capacity, gives Kia access to one of the world's fastest-growing auto markets. The Seltos and Sonet, designed specifically for Indian consumers, have made Kia a significant player in a market where brand loyalty is still being formed.

This geographic diversification proved its value in 2025, when U.S. tariffs contributed to a significant compression of Kia's operating margins—from 11.8% to roughly 8%. The impact was real but manageable precisely because Kia's Georgia plant produces a large share of its U.S.-sold vehicles domestically. A competitor importing entirely from Asia would have faced a far more severe margin hit.

The broader strategic principle is simple: in a world of rising trade barriers and geopolitical fragmentation, manufacturing where you sell is not just a cost optimization—it is a strategic necessity. Kia figured this out earlier and more aggressively than most of its competitors.

X. Analysis: The Bull vs. Bear Case

The Bull Case

The optimistic view of Kia centers on three pillars. First, the PBV business represents a genuinely new revenue stream with potentially superior margins and lower cyclicality than the consumer auto business. If Kia captures even a fraction of the commercial EV fleet market, it adds a profit pool that analysts are not yet fully modeling. Second, Kia's EV margins are among the best in the industry, driven by the shared-platform economics of the Hyundai Motor Group and the brand's ability to command premium pricing on vehicles like the EV6 and EV9. Most legacy automakers are losing money on EVs; Kia appears to be making money on them. Third, and perhaps most importantly, Kia has successfully completed the most difficult transition in branding: shedding a "cheap" reputation and replacing it with one associated with design, quality, and innovation. That brand equity is a durable asset that should support pricing power for years to come. The stock's valuation—roughly 4 times trailing earnings, with an 11.8% operating margin and a balance sheet that generates enormous free cash flow—reflects a market that is either deeply skeptical of the sustainability of these results or simply applying a structural discount for Korean governance.

The Bear Case

The bearish argument is not about Kia's current execution, which is difficult to fault. It is about the environment in which Kia must compete going forward. The most immediate threat is the aggressive expansion of Chinese automakers, particularly BYD, into Kia's core markets. BYD's vertical integration, massive domestic scale, and willingness to operate on razor-thin margins make it a formidable price competitor. Chinese brands have already captured 85% of EV sales in Brazil and Thailand, and they are making rapid inroads in Europe. If BYD and its Chinese peers trigger a sustained price war in the global EV market, Kia's margins—no matter how well-managed—will face pressure.

The second bear concern is geopolitical. South Korea's proximity to North Korea introduces a tail risk that is difficult to price but impossible to ignore. Any escalation on the Korean peninsula would have immediate and severe implications for Kia's manufacturing base and stock price. This risk is partially mitigated by Kia's global manufacturing footprint, but the company's headquarters, its largest production facilities, its R&D centers, and the entire Hyundai Motor Group command structure remain concentrated in South Korea.

The third concern is the chaebol discount itself. Korean conglomerates have a long history of prioritizing growth and family control over shareholder returns. While Kia has improved its capital allocation in recent years—increasing dividends and conducting buybacks—the circular shareholding structure remains intact, and minority shareholders have limited recourse if the Chung family's strategic priorities diverge from profit maximization. Until structural governance reform occurs, the Korea discount may cap Kia's valuation regardless of its operational performance.

Finally, the 2025 financial results provided a sobering reminder that Kia is not immune to external shocks. Revenue rose to a record 114.1 trillion won, but operating profit fell 28.3% to 9.08 trillion won as U.S. tariffs and higher incentive spending compressed margins to roughly 8%. This is still a healthy margin by global auto standards, but it demonstrates that Kia's exceptional 2023-2024 profitability may have been partly a function of favorable external conditions—tight supply, low incentives, favorable currency—rather than a permanent new normal.

The honest assessment is that Kia is a fundamentally transformed company operating in an industry that is itself being fundamentally transformed. The company's execution over the past decade has been extraordinary. Whether that execution can continue against a rising tide of Chinese competition, geopolitical uncertainty, and the inherent margin pressure of the EV transition is the question that separates the bulls from the bears.

XI. Epilogue: Movement That Inspires

There is a particular irony in Kia's corporate tagline—"Movement That Inspires"—that is worth dwelling on. For most of its history, Kia was the company that moved because it had to, not because it chose to. It was forced to make bicycles because Korea had no industrial base. It was forced to make trucks because the government banned it from making cars. It was forced into Hyundai's arms because it could not pay its debts. At every critical juncture, Kia's movement was reactive—a response to crisis, to constraint, to the decisions of more powerful actors.

What changed, starting in 2006 with Peter Schreyer's arrival and accelerating through the Plan S era, is that Kia began to move on its own terms. The Tiger Nose was not a reaction to a competitor; it was a declaration of identity. The EV6 was not a response to a regulation; it was a bet on a technology. The PBV strategy is not a defensive pivot; it is an offensive expansion into a new market category.

Kia's story is ultimately about what happens when a company decides that being the second-class citizen—the junior brand, the budget option, the bankruptcy survivor—is not a limitation but a license. Because Kia was never the flagship brand, it could take risks that Hyundai could not. Because Kia had no prestigious heritage to protect, it could reinvent itself more radically than BMW or Mercedes ever would. Because Kia had been written off, it had nothing to lose by swinging for the fences.

From steel tubing in 1944 to the most profitable mass-market automaker in the world eight decades later, Kia Corporation is proof that in business, as in nature, the survivors are not always the strongest or the most prestigious. Sometimes they are simply the ones willing to adapt faster than anyone thought possible.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube