CK Hutchison: The Global Arbitrage Machine

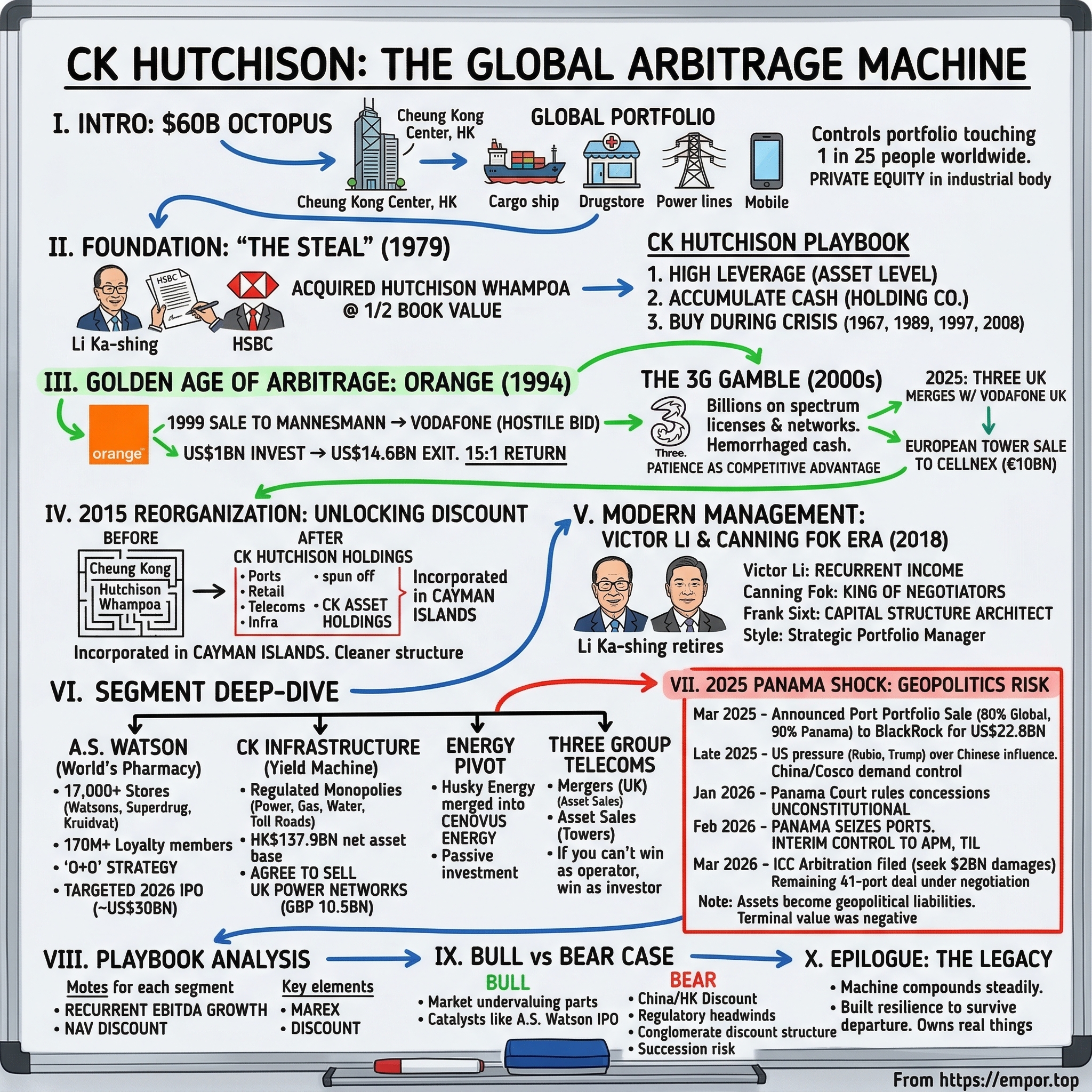

I. Introduction: The $60 Billion Octopus

There is a building in Central, Hong Kong—Cheung Kong Center, seventy stories of glass and steel rising from the reclaimed waterfront—where a single corporate entity quietly controls a portfolio that touches the daily life of roughly one in every twenty-five people on the planet. The container that carried your flat-screen television likely passed through one of its port terminals. The drugstore where you bought your shampoo in London, Amsterdam, or Kuala Lumpur is probably one of its seventeen thousand retail outlets. The electricity powering your home in the English Midlands flows through wires it owns. And if you are reading this on a mobile phone in the United Kingdom, Italy, or Austria, there is a reasonable chance your data is traveling over a network it built.

Most people who have heard of Li Ka-shing know him as the legendary real estate tycoon—"Superman," as the Hong Kong tabloids christened him decades ago. But to reduce CK Hutchison Holdings to a property story is to fundamentally misunderstand what the Li family built. CK Hutchison is, at its core, one of the world's most sophisticated private equity operations disguised in the body of an industrial conglomerate. It buys physical assets—ports, spectrum licenses, power grids, retail chains—at moments of dislocation, operates them patiently for years or decades, and then sells them at precisely the moment when a buyer is willing to pay a premium that the public market never would. The company does not disrupt industries. It owns the infrastructure that industries depend on, and it has an almost preternatural instinct for knowing when that infrastructure is overvalued.

The numbers are staggering in their scope. Revenue of approximately HK$281 billion in 2024—roughly thirty-six billion US dollars. Operations spanning more than fifty countries. Three hundred thousand employees. A balance sheet carrying HK$121 billion in cash alongside HK$325 billion in debt—a capital structure that looks aggressive until you realize that the debt sits at the asset level while the cash accumulates at the holding company, a deliberate architectural choice that has allowed CK Hutchison to survive every financial crisis of the past four decades without once facing a liquidity scare.

The story of CK Hutchison is organized around a series of perfectly timed transactions that, taken together, constitute one of the greatest records of capital allocation in modern corporate history. The 1979 acquisition of Hutchison Whampoa from HSBC at half of book value. The 1999 sale of Orange to Mannesmann at the absolute peak of the telecom bubble. The 2015 corporate reorganization that unlocked billions in value overnight. And now, in 2025 and 2026, the most ambitious restructuring yet: a simultaneous attempt to sell the global ports business, IPO the retail crown jewel, and spin off the European telecoms operation—a three-pronged dismantling of the conglomerate that could release more than fifty billion dollars of value and fundamentally transform what CK Hutchison is.

But as of today, that plan has collided with the hardest force in global business: geopolitics. The Panama ports sale—announced in March 2025 as a tidy US$22.8 billion deal with BlackRock—has devolved into a diplomatic crisis involving the United States, China, and the Republic of Panama. The ports have been seized. Arbitration proceedings are underway. And CK Hutchison finds itself at the center of a question that no amount of financial engineering can solve: what happens when the world's most skilled asset flipper discovers that some assets are no longer just business?

This is that story.

II. The Foundation: "The Steal" and the Conglomerate Playbook

On the morning of September 25, 1979, Li Ka-shing walked into a boardroom at the Hongkong and Shanghai Banking Corporation and signed the papers that would transform him from a wealthy property developer into a global industrial titan. HSBC was selling its 22 percent stake in Hutchison Whampoa, one of the storied British "hongs"—the colonial trading houses that had dominated Hong Kong's economy for over a century—and the buyer was a Chinese immigrant who had arrived in Hong Kong as a penniless twelve-year-old refugee fleeing the Japanese invasion of Guangdong.

The price was HK$639 million, roughly half of book value. HSBC's motivation for selling cheap has been debated for decades, but the most credible explanation is both simple and revealing: the bank needed a politically astute local partner as the colony's 1997 handover to China loomed on the horizon, and Li Ka-shing—already known for his shrewd deal-making and his careful cultivation of relationships on both sides of the political divide—was the ideal candidate. For HSBC, it was an insurance policy. For Li, it was the foundation of everything that followed.

What made the deal transformative was not just the price; it was what Li was buying. Hutchison Whampoa was not a single business but a portfolio—a sprawling collection of ports, retail operations, trading companies, and industrial assets inherited from the British colonial era. It was, in other words, a platform: a pre-built conglomerate with global reach, blue-chip relationships, and a brand name that opened doors in boardrooms from London to Sydney. No Chinese entrepreneur had ever controlled one of these hongs. The symbolic weight of the transaction was as significant as the financial logic. Li Ka-shing was not just buying assets. He was buying legitimacy on the global stage.

Over the next fifteen years, Li methodically applied a playbook that would become the CK Hutchison signature. The formula had three elements. First, use high leverage at the asset level to acquire physical infrastructure—ports, utilities, telecoms—that generates stable, recurring cash flows. Second, funnel those cash flows up to the holding company, where they accumulate as a massive war chest. Third, deploy that war chest to buy aggressively during moments of crisis, when asset prices collapse and other buyers are paralyzed by fear.

Li's timing was uncanny, and it was rooted in lived experience. He had survived the 1967 Hong Kong riots, buying property at rock-bottom prices while the colony teetered on the edge of chaos. He bought more after the Tiananmen Square crisis in 1989, when Hong Kong real estate prices cratered and the wealthy were fleeing to Vancouver and Sydney. And he would buy again during the Asian financial crisis of 1997 and the global financial crisis of 2008. Each time, the pattern was the same: others panicked, Li accumulated, and within a few years the acquired assets were worth multiples of what he had paid.

By 1985, the empire had expanded to include Hongkong Electric Holdings, the monopoly power supplier for Hong Kong Island. By the early 1990s, Hutchison Whampoa had become one of the world's largest container port operators, with terminals in Hong Kong, mainland China, the United Kingdom, and Panama. The retail arm, A.S. Watson, was growing from a colonial-era pharmacy into an Asian retail powerhouse. Each piece fit into a larger architecture: assets that generated predictable cash, owned by entities that could be leveraged individually without endangering the parent, all feeding a holding company that sat on an ever-growing pile of dry powder.

The model worked brilliantly for a single reason: Li Ka-shing understood, decades before it became fashionable in private equity circles, that the real money in physical infrastructure is made not in the operating income but in the spread between the price you pay for the asset and the price at which you ultimately sell it. Operating a container port competently generates a solid return. Buying that port during a downturn and selling it during a boom generates a spectacular one. CK Hutchison was, from the very beginning, an arbitrage machine—and the next chapter would produce its most legendary trade.

III. The Golden Age of Arbitrage: Orange and the 3G Gamble

In the early 1990s, the European mobile telephone industry was a frontier—a Wild West of competing standards, uncertain demand, and governments auctioning off spectrum licenses to anyone with the capital and the nerve to bid. Most of the established telecom operators viewed mobile as a supplement to their landline businesses, a niche product for executives and early adopters. Li Ka-shing and his dealmaker-in-chief, Canning Fok, saw something different. They saw a cornered resource—radio spectrum—that was being sold at prices that dramatically undervalued its long-term potential, in a market that was about to undergo exponential growth.

Hutchison Whampoa's entry into European telecoms began in 1994, when it acquired a mobile license in the United Kingdom and launched a brand called Orange. The investment was roughly one billion US dollars, a meaningful sum but not a bet-the-company wager. The execution was superb. Orange distinguished itself with a clean brand identity—literally, the color orange in a market dominated by sterile corporate blues—and a customer-friendly approach that won subscribers at a remarkable pace. By the late 1990s, Orange had become one of the most recognized mobile brands in Britain, with over three and a half million subscribers.

Then came the exit, and it remains one of the most celebrated trades in corporate history.

In October 1999, Germany's Mannesmann AG—a diversified industrial conglomerate that was aggressively expanding into telecoms—agreed to acquire Hutchison's roughly 49 percent stake in Orange for approximately US$14.6 billion. The deal was structured as a mix of cash and a significant stake in Mannesmann itself, giving Hutchison a seat at the table for whatever came next. What came next was extraordinary. Mannesmann's acquisition of Orange made it one of the largest mobile operators in Europe, which in turn made it the most attractive takeover target on the continent. Within weeks, Vodafone launched a hostile bid for Mannesmann. The resulting takeover, completed in February 2000 at a price of US$183 billion, was the largest merger in history. Hutchison Whampoa, holding its Mannesmann shares, found itself with a roughly 5 percent stake in the combined Vodafone Group. It promptly sold a large portion of that stake for approximately US$5 billion in cash.

Add it up: an investment of roughly one billion dollars, a primary exit at fourteen and a half billion, and a secondary exit that brought in billions more. The total return was somewhere north of fifteen-to-one, achieved over approximately five years. And the timing was impeccable. The telecom bubble peaked in March 2000, barely months after the Mannesmann deal closed. Within two years, European telecom stocks had lost seventy to eighty percent of their value. Mannesmann, Vodafone, France Telecom—every buyer in the chain ended up owning assets worth a fraction of what they had paid. Li Ka-shing had sold into the euphoria, pocketed the cash, and watched the bonfire from a safe distance.

But here is where the story takes a twist that reveals something deeper about CK Hutchison's risk appetite. Rather than banking the Orange windfall and resting on the achievement, Li and Fok immediately reinvested the proceeds into the next generation of mobile technology: third-generation, or 3G, networks. Between 2000 and 2003, Hutchison spent billions acquiring 3G spectrum licenses across Europe—in the UK, Italy, Austria, Ireland, Denmark, and Sweden—and began building networks under the "Three" brand from scratch.

The timing, this time, was terrible. The 3G license auctions of 2000 and 2001 occurred at the peak of telecom mania, when governments extracted eye-watering sums from operators desperate to secure their place in the mobile future. The UK auction alone raised over thirty billion pounds. Hutchison's bids were aggressive, and the cost of building out 3G networks on top of the license fees was enormous. Throughout the first decade of the 2000s, the Three operations hemorrhaged cash. Annual losses ran into the billions. Analysts downgraded the stock. Investors questioned whether the Orange windfall had been squandered on a vanity project.

It had not. What the market failed to appreciate was that CK Hutchison had acquired something far more valuable than a mobile subscriber base—it had acquired spectrum, a finite physical resource that cannot be manufactured, replicated, or disrupted by software. Spectrum is the real estate of the wireless world: there is a fixed supply, and every year the demand for wireless data grows exponentially. The Three networks eventually reached profitability as smartphones transformed 3G from a voice service into a data pipe, and the spectrum holdings appreciated in value as the industry consolidated.

The proof came in stages. In 2020 and 2021, CK Hutchison sold its European tower portfolio to Spain's Cellnex for approximately ten billion euros, monetizing the physical infrastructure of its networks while retaining the spectrum and the subscriber base. It was the Orange playbook in miniature: build an asset, operate it patiently, and sell the piece that the market overvalues while keeping the piece that the market undervalues. And the culmination came in 2025, when Three UK merged with Vodafone UK—the same Vodafone that had been on the other side of the Orange transaction a quarter century earlier. In a fitting piece of symmetry, CK Hutchison ended up with a 49 percent stake in the combined entity, VodafoneThree, which became the largest mobile operator in the United Kingdom by subscriber count.

The 3G saga taught CK Hutchison a lesson that runs through everything it does: patience is a competitive advantage. In a world where quarterly earnings drive stock prices and activist investors demand immediate returns, CK Hutchison has demonstrated a willingness to endure a decade or more of accounting losses in pursuit of an asset position that will ultimately prove irreplaceable. The Orange trade was brilliant in its timing. The 3G investment was brilliant in its stubbornness. Together, they defined the company's approach to capital allocation: buy cornered resources cheaply, endure the pain, and sell when the rest of the world finally recognizes what you own.

IV. The 2015 Reorganization: Unlocking the "Superman" Discount

By 2014, the corporate structure that Li Ka-shing had built over thirty-five years was, to put it charitably, a labyrinth. At the top sat Li Ka-shing personally, who controlled Cheung Kong Holdings, which controlled Hutchison Whampoa, which controlled various listed and unlisted subsidiaries including Cheung Kong Infrastructure, Hutchison Telecommunications, and Power Assets Holdings. Cross-holdings between entities created a web that even experienced Hong Kong analysts struggled to map. Cheung Kong owned roughly 50 percent of Hutchison Whampoa. Hutchison Whampoa owned stakes in CKI and Power Assets. CKI owned stakes in Power Assets as well. It was a Matryoshka doll of holding companies, each one owning a piece of the others, and the net effect was a discount that never seemed to close.

The holding company discount is one of the most persistent phenomena in Asian equity markets. Investors know that the underlying assets—the ports, the retail chain, the power grids—are each worth a certain amount. But when those assets are bundled together inside a complex corporate structure with opaque inter-company transactions, cross-subsidies, and the ever-present fear of related-party dealings, the market refuses to pay full price. By some estimates, the Li Ka-shing empire was trading at a thirty to forty percent discount to the sum of its parts—a gap that represented tens of billions of dollars in unrealized value.

The solution, announced on January 9, 2015, was as elegant as it was radical. Li proposed to dismantle the existing structure and rebuild it from scratch. Cheung Kong Holdings would offer approximately US$24 billion in stock to buy out the minority shareholders of Hutchison Whampoa, effectively collapsing the two entities into one. The combined assets would then be sorted into two clean buckets: all non-property businesses—ports, telecoms, retail, infrastructure, energy—would go into a newly created entity called CK Hutchison Holdings Limited; and all property businesses would be spun off into a separate entity called Cheung Kong Property Holdings, later renamed CK Asset Holdings.

The reorganization was completed on June 3, 2015. Hutchison Whampoa was delisted that same day, ending eighty years of history as one of the most storied companies on the Hong Kong Stock Exchange. The market's reaction was immediate and positive: CK Hutchison's shares jumped more than ten percent in the first days of trading, as investors rewarded the cleaner structure and the implied promise of more transparent capital allocation.

But the most controversial element of the reorganization had nothing to do with the financial engineering. It was the decision to incorporate CK Hutchison Holdings not in Hong Kong, but in the Cayman Islands.

The official rationale was straightforward: the Cayman Islands offered a well-established legal framework for international holding companies, greater flexibility in corporate governance, and a structure more familiar to global institutional investors. Critics saw something more ominous—a vote of no-confidence in Hong Kong's future as an autonomous business center, an insurance policy against the possibility that Beijing would one day extend mainland Chinese corporate law to the territory. Li Ka-shing denied any political motivation, but the timing was hard to ignore. The reorganization came against a backdrop of deepening anxiety about Hong Kong's relationship with Beijing, concerns that would intensify dramatically in the years that followed with the 2019 protests and the 2020 National Security Law.

Whatever the motivation, the practical effect of the 2015 reorganization was to create a cleaner, more legible corporate structure that set the stage for the next phase of CK Hutchison's evolution. With property separated out, CK Hutchison could be evaluated purely as an operating conglomerate—one that owned ports, retail, telecoms, and infrastructure—and managed for the explicit purpose of maximizing returns on those assets through operational improvement and, when the price was right, strategic divestiture. The "Asset Light" era had begun, and a new generation of management was about to take the helm.

V. Modern Management: The Victor Li and Canning Fok Era

On May 10, 2018, at the annual general meeting of CK Hutchison Holdings, Li Ka-shing formally stepped down as chairman. He was eighty-nine years old. He had built one of the largest business empires in Asia from nothing—a refugee boy who started by making plastic flowers in a factory and ended up controlling assets on six continents. The audience at the meeting rose to give him a standing ovation, and then Victor Li Tzar-kuoi, his elder son, took the chairman's seat.

The succession had been telegraphed for years, but it was nonetheless a pivotal moment. CK Hutchison had been, for its entire existence, a vehicle for one man's extraordinary instincts. Li Ka-shing's ability to sense inflection points in markets—to know when to buy and when to sell—was not a process that could be codified in a management manual. The question facing investors was simple and existential: could the machine run without the mechanic?

Victor Li is, in almost every respect, the opposite of his father's public persona. Where Li Ka-shing was charismatic, quotable, and visibly driven by a kind of immigrant hunger, Victor is measured, quiet, and methodical. He holds degrees in civil engineering and structural engineering from Stanford University. He joined the family business in the late 1980s and spent decades working his way through various operating roles, learning the portfolio from the inside. Colleagues describe him as deeply analytical, someone who makes decisions based on spreadsheets rather than gut instinct.

Victor's personal history includes a detail that is impossible to overlook. In 1996, he was kidnapped by the notorious gangster Cheung Tze-keung, known as "Big Spender," and held for ransom. Li Ka-shing reportedly paid over one billion Hong Kong dollars for his son's release—one of the largest ransoms in history. Victor has rarely spoken about the experience publicly, but those who know him say it profoundly shaped his approach to risk. He emerged from the ordeal as a man who prizes control, predictability, and downside protection above all else. In a corporate context, this translates into a management style that favors "recurrent income"—stable, predictable cash flows from regulated or quasi-monopolistic assets—over the high-wire deal-making that characterized his father's era.

The other key figure in the modern CK Hutchison management structure is Canning Fok Kin-ning, the Deputy Chairman who has been the operational brain behind the empire's most important transactions for over three decades. Fok was the architect of the Orange deal. He negotiated the 3G spectrum acquisitions. He structured the Cellnex tower sale. In the world of Hong Kong business, he is known as the "King of Negotiators"—a man who can sit across the table from the CEOs of the world's largest companies and extract terms that consistently favor CK Hutchison. His role has been gradually transitioning from front-line dealmaker to strategic advisor, but his fingerprints remain on every major transaction the company undertakes.

Completing the triumvirate is Frank Sixt, the Group Finance Director who has served in the role since 1991—a tenure of over thirty-five years. Sixt is the least visible of the three but arguably the most important to the company's structural resilience. He is the architect of CK Hutchison's distinctive capital structure: high leverage at the subsidiary level, massive cash reserves at the holding company, and a web of non-recourse financing that ensures no single asset failure can cascade upward to threaten the parent. The company carries approximately HK$325 billion in total debt, but this debt is distributed across dozens of operating entities, each ring-fenced from the others. Sixt has managed this structure through the Asian financial crisis, the dot-com collapse, the global financial crisis, and COVID-19 without once triggering a covenant breach or a distressed refinancing. In a conglomerate of this complexity, that track record is the equivalent of a perfect safety record at a nuclear power plant.

The Li family controls approximately 30 percent of CK Hutchison's shares, enough to maintain effective control but not so much that minority shareholders are powerless. The governance structure is unusual in that it blends family-office dynamics with institutional-scale operations. Executive compensation is tied not to revenue growth or share price performance, but to what the company internally calls "value realization"—the combination of dividends paid to shareholders and the cash proceeds generated from successful asset exits. This alignment of incentives explains much of CK Hutchison's behavior. Management is not rewarded for empire-building. It is rewarded for knowing when to hold an asset and when to let it go.

The result, under Victor Li's leadership, has been a decisive shift from "Aggressive Acquirer" to "Strategic Portfolio Manager." The acquisitions have slowed. The divestitures have accelerated. And the overarching strategy has become increasingly clear: transform CK Hutchison from an opaque conglomerate into a collection of transparently valued, independently listed businesses—a process that, if completed, would effectively work the company out of its own conglomerate discount.

VI. Segment Deep-Dive: The Hidden Engines

A.S. Watson: The World's Pharmacy

Walk into any major shopping district in Europe or Asia and count the drugstores. In London, it is Superdrug. In Amsterdam, it is Kruidvat. In Hong Kong, Kuala Lumpur, or Bangkok, it is Watsons. In Germany and Central Europe, the stores operate under the Rossmann brand through a joint venture. These are all, ultimately, the same company: A.S. Watson Group, the world's largest international health and beauty retailer, and CK Hutchison's single most valuable operating asset.

The numbers are remarkable. More than seventeen thousand stores across thirty-one markets, operating under twelve retail brands. Over 170 million loyalty program members—a customer database that rivals those of the world's largest tech platforms in scale, if not in glamour. Revenue growth has been steady, with the health category growing 8 percent and the beauty category growing 6 percent in the most recent fiscal year, with particularly strong double-digit growth in European health and Asian beauty.

But the headline numbers obscure what makes A.S. Watson truly exceptional as a business. The key is what the company calls its "O+O" strategy—Offline plus Online. Unlike pure-play e-commerce companies that are trying to build physical presence, and unlike traditional retailers that are trying to build digital capabilities, A.S. Watson has spent two decades building a platform that seamlessly integrates both channels. A customer might browse products on the Watsons app, check availability at her local store, order online for in-store pickup, and earn loyalty points that can be redeemed across any channel. The O+O platform achieved double-digit growth in 2025, and it has fundamentally changed the economics of the business by reducing inventory waste, improving demand forecasting, and creating a closed-loop marketing system that allows A.S. Watson to sell targeted advertising and shelf placement to consumer brands like L'Oreal and Procter & Gamble.

The procurement power is equally significant. When you operate seventeen thousand stores across thirty-one markets, you are not a customer of L'Oreal or P&G—you are a partner. A.S. Watson's buyers can negotiate terms that no regional drugstore chain can match, and the company uses its scale to develop private-label products that carry significantly higher margins than branded goods. This is the classic scale economy at work: every additional store makes the entire network more profitable through lower procurement costs and greater leverage with suppliers.

CK Hutchison is now pursuing a dual listing of A.S. Watson on the Hong Kong and London stock exchanges, targeting the first half of 2026. Goldman Sachs and UBS have been appointed as advisors, and early reports suggest a target valuation of approximately US$30 billion. The IPO would also provide an exit for Temasek, Singapore's sovereign wealth fund, which holds a 25 percent stake in A.S. Watson. If completed, this listing alone could be one of the largest retail IPOs in history—and it would, for the first time, give the market a transparent, standalone valuation for CK Hutchison's most valuable asset.

CK Infrastructure: The Yield Machine

If A.S. Watson is the crown jewel, CK Infrastructure Holdings is the ballast. CKI, in which CK Hutchison holds approximately 75.67 percent, is the largest publicly listed infrastructure company in Hong Kong. Its portfolio reads like a catalog of regulated monopolies: UK power distribution networks, Australian gas pipelines, Canadian water treatment plants, European toll roads, and electricity grids stretching across multiple continents.

The beauty of regulated infrastructure is its predictability. A power distribution network earns a rate of return that is set by the regulator, adjusted periodically for inflation and capital investment. The demand for electricity does not disappear in a recession. Customers do not churn. Competitors cannot build a rival grid. The cash flows are, for all practical purposes, annuity-like—and CKI has deployed this predictability to build a net asset base that has grown from HK$8.4 billion at its founding in 1996 to HK$137.9 billion at the end of 2025, a sixteen-fold increase over three decades.

CKI reported profit of HK$8.3 billion in 2025, up modestly from the prior year, with a remarkably conservative net debt to net total capital ratio of just 8.9 percent. The business generates cash so reliably that it has become, in effect, a "yield company" embedded within a conglomerate—a vehicle that pays a steady dividend funded by assets that have virtually zero risk of obsolescence.

The most significant recent development at CKI is the agreement to sell 100 percent of UK Power Networks to France's Engie for approximately GBP 10.5 billion, or roughly US$14.2 billion. The consortium that owns UKPN—CKI holding 40 percent, Power Assets Holdings holding 40 percent, and CK Asset Holdings holding 20 percent—acquired the business over a decade ago and has overseen its expansion into smart grid technology, EV charging infrastructure, and renewable energy integration. CKI's share of the proceeds, approximately GBP 4.2 billion, represents a substantial windfall that will further bolster the group's already formidable cash position.

The Energy Pivot: From Husky to Cenovus

For years, CK Hutchison's energy exposure was concentrated in Husky Energy, a Canadian oil and gas company in which it held a controlling stake. Husky was a source of frustration for investors—a mid-tier oil producer that lacked the scale of the Canadian majors and was heavily exposed to the notoriously volatile Western Canadian heavy oil market. When oil prices collapsed in 2014 and again in 2020, Husky's earnings evaporated, dragging down the group's consolidated results.

The solution was a merger. In 2021, Husky was folded into Cenovus Energy, one of Canada's largest integrated oil companies, in an all-stock transaction. CK Hutchison exchanged its controlling stake in a struggling mid-tier producer for approximately a 16 percent stake in a much larger, better-capitalized company with diversified operations spanning oil sands production, conventional drilling, and downstream refining. The move transformed energy from a management headache into a passive investment—one that still provides meaningful exposure to oil prices but no longer requires CK Hutchison to manage drilling programs, refinery operations, or regulatory compliance.

Three Group Telecoms: From Operator to Asset Seller

The European telecoms operations under the Three brand have been the most contested piece of the CK Hutchison portfolio. For years, Three was the smallest of the four mobile operators in each of its markets—the UK, Italy, Austria, Ireland, Denmark, and Sweden. Being the smallest operator in a four-player market is structurally disadvantaged: you lack the scale to spread infrastructure costs across enough subscribers, and you lack the negotiating leverage to secure the best spectrum positions. The result was persistently thin margins and, in some markets, outright losses.

CK Hutchison's response was a masterclass in capital recycling. First, it sold the European tower infrastructure to Cellnex for approximately ten billion euros, monetizing the physical steel and concrete while retaining the spectrum licenses and customer relationships. Then it pursued consolidation. The merger of Three UK with Vodafone UK, completed on May 31, 2025, created VodafoneThree—the largest mobile operator in Britain by subscribers. CK Hutchison holds 49 percent of the combined entity, Vodafone holds 51 percent. The merger resulted in a one-time non-cash accounting loss of HK$10.9 billion and net cash proceeds of GBP 1.3 billion, but the strategic logic is compelling. VodafoneThree plans to invest GBP 11 billion over ten years in its combined network, with expected synergies of GBP 700 million annually by year five.

The transformation from a money-losing standalone operator to a minority stakeholder in the UK's dominant mobile carrier is perhaps the clearest expression of Victor Li's management philosophy: if you cannot win as an operator, restructure the asset until you can win as an investor.

VII. The 2025 Panama Shock: Geopolitics as the Ultimate Risk

On a Tuesday morning in early March 2025, CK Hutchison Holdings announced what appeared to be the capstone of its transformation strategy: the sale of 80 percent of its global ports portfolio—43 ports, 199 berths, 23 countries—plus 90 percent of its Panama Canal port operations to a consortium led by BlackRock and Terminal Investment Limited, an affiliate of Mediterranean Shipping Company. The aggregate enterprise value for the entire ports perimeter was US$22.8 billion. Expected net cash proceeds to CK Hutchison: in excess of US$19 billion.

The deal had a beautiful logic. CK Hutchison had spent forty years building one of the world's most valuable port networks, anchored by the crown jewels: Balboa and Cristobal, the two terminals that bracket the Panama Canal. But the world had changed. Being a Hong Kong-headquartered company operating a strategic chokepoint in the Western Hemisphere was no longer just a matter of logistics and commerce. It was a matter of great-power rivalry.

The pressure had been building for years. The Trump administration, which returned to power in January 2025, made the Panama Canal a centerpiece of its confrontational posture toward both China and the Republic of Panama. US Secretary of State Marco Rubio traveled to Panama City in early February, delivering a blunt message to President Mulino: reduce Chinese influence over the canal or face consequences. President Trump himself had alleged—inaccurately, but loudly—that China was "running the Panama Canal." The fact that CK Hutchison is a Hong Kong company, not a mainland Chinese state-owned enterprise, was a distinction without a difference in the political theater of Washington.

CK Hutchison's management read the situation clearly. Canning Fok and Victor Li recognized that the ports had become a geopolitical liability—a "target" that attracted political risk disproportionate to the financial return. The BlackRock deal was their exit strategy: sell at a premium valuation to Western buyers with impeccable political credentials, pocket the cash, and redeploy into less controversial markets.

What happened next was a lesson in how geopolitics can overwhelm even the most carefully constructed deal.

The signing, initially targeted for early April 2025, was delayed. By late 2025, the Chinese government had made its displeasure known. China's state-owned Cosco Shipping was invited to join the BlackRock consortium in an attempt to secure Chinese regulatory approval for the transaction. But Cosco, reportedly under instructions from Beijing, demanded not a minority stake but a majority position in the consortium—a condition that would have defeated the entire purpose of the deal from the American perspective. BlackRock and MSC considered walking away.

Then Panama acted. In January 2026, the country's Supreme Court ruled that CK Hutchison's two port concessions at Balboa and Cristobal were unconstitutional. On February 23, 2026, the Panamanian government physically seized the ports, revoking CK Hutchison's operating rights and handing interim control to APM Terminals, a subsidiary of Maersk, and TIL, MSC's terminal affiliate.

CK Hutchison responded by filing international arbitration proceedings under the rules of the International Chamber of Commerce, seeking damages of at least US$2 billion. As of this writing in March 2026, Panama has failed to respond to the arbitration notice by the ICC deadline. China's Hong Kong and Macau Affairs Office has called Panama's ruling "absurd" and "shameful," warning that the country could face a "heavy price." The remaining 41-port deal with BlackRock and MSC—covering the non-Panama assets—is still under negotiation as a separate transaction.

The Panama saga is instructive for investors in several ways. First, it demonstrates that CK Hutchison's core skill—buying undervalued physical assets in politically complex jurisdictions—carries a tail risk that traditional financial analysis struggles to capture. The Panama concessions were enormously profitable for more than two decades, but the terminal value turned out to be negative in the most literal sense: the asset was not sold; it was confiscated. Second, it shows that management's instinct to exit was correct, even if the execution was overtaken by events. CK Hutchison recognized the risk and moved to monetize the asset before the political situation deteriorated further. The fact that it was too late does not negate the strategic judgment; it merely illustrates that in a world of great-power competition, "too late" can arrive faster than any corporate timeline anticipates.

The financial impact is significant but not existential. The Panama ports represented perhaps one to two billion dollars of the total US$22.8 billion enterprise value. The arbitration claim seeks at least US$2 billion in damages, which, if successful, would more than compensate for the lost asset value. And the remaining ports portfolio—spanning the Americas, Europe, the Middle East, and Southeast Asia—retains enormous value. But the reputational damage is real. CK Hutchison is now a case study in geopolitical risk, and every future investment it makes in a strategically sensitive sector will be scrutinized through the lens of what happened in Panama.

VIII. Playbook Analysis: Strategic Moats and Competitive Position

The most useful way to evaluate CK Hutchison's competitive position is to ask a simple question for each of its major business segments: could a well-funded competitor replicate this business from scratch?

In ports, the answer is effectively no. Container terminal concessions are finite. Governments award them infrequently, and once a terminal is built and operational, the switching costs for shipping lines are enormous. Port infrastructure benefits from what Hamilton Helmer calls a "Cornered Resource"—the berth, the land, the deep-water access, and the regulatory approval to operate form a bundle that cannot be duplicated. You cannot build another Port of Felixstowe next door. CK Hutchison's ports network, even after the loss of Panama, comprises some of the most strategically located terminals in global trade, and the barriers to replication are measured in decades and billions of dollars.

In retail, A.S. Watson's moat is built on scale economies. When you are negotiating with L'Oreal or Procter & Gamble as the operator of seventeen thousand stores, your per-unit procurement cost is structurally lower than that of any regional competitor. The loyalty database of over 170 million members creates an information advantage that compounds over time—A.S. Watson knows what its customers buy, when they buy it, and what promotions change their behavior, and it can sell this intelligence back to brands as a premium advertising channel. A new entrant would need decades and tens of billions of dollars to build a comparable network, and even then, the incumbent's data advantage would remain.

In infrastructure, the moat is regulatory. Power distribution networks, gas pipelines, and water treatment plants are natural monopolies. Regulators grant exclusive operating rights for defined territories, and the returns are set by regulatory formula. The competitive dynamic is not about beating rivals in the marketplace; it is about managing the regulatory relationship and deploying capital efficiently within the allowed framework. CKI's three-decade track record of regulatory engagement across multiple jurisdictions is itself a competitive advantage—regulators prefer to work with operators they know and trust.

In telecoms, the picture is more nuanced. The Three brand has historically operated from a position of structural weakness—the smallest operator in four-player markets. The merger with Vodafone UK has fundamentally improved this position in the UK, but the other European markets remain challenging. The 5G spectrum holdings represent a cornered resource, but the business of operating a mobile network is brutally competitive, with high churn rates, relentless price pressure, and heavy capital expenditure requirements. This is the one segment where CK Hutchison's competitive position is more "adequate" than "dominant," and it explains why management has been actively exploring options to spin off or restructure the remaining European telecoms assets.

From a Porter's Five Forces perspective, the picture is revealing. The threat of new entrants is extremely low across ports, infrastructure, and retail—barriers are simply too high. Supplier power is moderate; CK Hutchison is itself a major buyer across all segments, which limits suppliers' ability to extract rents. Buyer power varies dramatically: in infrastructure, where customers have no alternative, buyer power is near zero; in telecoms, where subscribers can switch carriers with a phone call, buyer power is high. The threat of substitution is real in telecoms (Wi-Fi, satellite broadband) but negligible in ports and infrastructure. And competitive rivalry ranges from muted (regulated infrastructure) to intense (European mobile).

The capital allocation discipline ties everything together. CK Hutchison's internal benchmark, according to investor communications over the years, targets a return on equity of 12 to 15 percent for any asset it holds. When an asset cannot meet this threshold—whether due to structural industry challenges, regulatory changes, or geopolitical risk—management sells. When an asset can exceed this threshold—typically because it was purchased at a distressed valuation or because market conditions have improved—management holds and compounds. This discipline explains the portfolio's constant evolution: the Panama ports are gone, the UK power network is being sold, the telecom towers have been monetized, and A.S. Watson is being prepared for public listing. Each exit reflects a judgment that the asset's return profile has peaked or that its risk profile has shifted unfavorably. It is not sentiment. It is arithmetic.

IX. The Bull vs. Bear Case

The Bull Case

The optimistic thesis for CK Hutchison rests on a single observation: the market is dramatically undervaluing the parts. At the current share price of approximately HK$60, CK Hutchison's market capitalization sits around HK$230 billion—roughly US$29 billion. Analysts who have attempted sum-of-the-parts valuations, assigning conservative standalone multiples to each business segment, consistently arrive at figures that are forty to fifty percent higher than the market price. If A.S. Watson is worth US$30 billion—the reported target for the upcoming IPO—then CK Hutchison's 75 percent stake in that business alone is worth US$22.5 billion, or roughly three-quarters of the entire group's current market cap. Add in the 75.67 percent stake in CKI, the Cenovus energy holding, the telecoms assets, and the remaining ports, and the implied value of everything else is close to zero.

The catalysts for closing this discount are tangible and imminent. The A.S. Watson IPO, if executed at the reported valuation, would establish a transparent market price for the retail business for the first time, forcing a revaluation of CK Hutchison shares. The proceeds from the UKPN sale—approximately GBP 4.2 billion to CKI—will flow up to the holding company through dividends. The VodafoneThree merger is expected to become accretive to free cash flow by fiscal year 2029, transforming the UK telecoms operation from a cash drain into a cash generator. And the remaining ports deal with BlackRock and MSC, if completed, would generate billions more in disposal proceeds.

Victor Li has stated that the group will seek investments offering "stable long-term cash flow in countries that respect foreign investments"—a clear pivot toward less geopolitically sensitive markets. The dividend, currently yielding approximately 5 percent, provides a meaningful return while investors wait for the restructuring to play out. Underlying profit rose 7 percent to HK$22.3 billion in 2025, demonstrating that the operating businesses are performing well despite the headline noise from Panama.

The Bear Case

The pessimistic thesis is equally straightforward: CK Hutchison may be permanently trapped in a valuation discount that no amount of financial engineering can resolve.

The "China/HK Discount" is the elephant in the room. In the decade since the 2015 reorganization, global institutional investors have systematically reduced their exposure to Hong Kong-listed companies, driven by concerns about Beijing's increasing assertiveness, the erosion of Hong Kong's judicial independence, and the broad deterioration of US-China relations. CK Hutchison is incorporated in the Cayman Islands and derives the vast majority of its revenue from outside China, but its listing venue, its controlling family, and its historical associations mark it as a "Hong Kong company" in the minds of global allocators. The Panama episode has only reinforced this perception. For a certain class of institutional investor, CK Hutchison is simply uninvestable—not because of its business quality, but because of its geopolitical address.

Regulatory headwinds are real across multiple segments. The VodafoneThree merger, while approved, came with conditions that may limit the combined entity's ability to raise prices or reduce competition in the UK market. European telecoms regulation remains hostile to consolidation, limiting CK Hutchison's options for its remaining Three operations in Italy, Austria, and Scandinavia. And the Panama arbitration, while potentially winnable, introduces years of legal uncertainty and reputational risk.

The conglomerate discount itself may be structural rather than cyclical. Markets have consistently refused to value diversified conglomerates at full sum-of-parts, and CK Hutchison's complexity—spanning six continents, five major industry sectors, and dozens of subsidiaries—is extreme even by conglomerate standards. The upcoming IPO and spin-offs could narrow the discount, but they could also fragment the shareholder base and reduce the holding company's strategic flexibility.

Finally, there is the question of succession beyond Victor Li. The current management team—Victor Li, Canning Fok, Frank Sixt—has been in place for decades, and all three are approaching or past traditional retirement age. The next generation of leadership is not yet visible to the market, and in a company where so much value has been created through individual judgment calls on asset timing, the question of who makes those calls in the future is not trivial.

KPIs That Matter

For investors tracking CK Hutchison's ongoing performance, the two metrics that matter most are the NAV discount (the gap between the market capitalization and the estimated sum-of-parts value of the underlying businesses) and recurrent EBITDA growth (the year-over-year change in operating cash flow from the company's core segments, excluding one-time disposal gains and accounting adjustments). The first tells you whether the market is recognizing the restructuring progress. The second tells you whether the underlying businesses are actually improving. If the NAV discount narrows while recurrent EBITDA grows, the thesis is working. If either metric moves in the wrong direction, it warrants a closer look.

X. Epilogue: The Legacy of the Superman

The CK Hutchison of 2026 looks almost nothing like the Hutchison Whampoa that Li Ka-shing acquired from HSBC in 1979. The British hong is gone. The plastic flowers factory is a museum. The freewheeling era of swashbuckling acquisitions financed by personal conviction and borrowed money has given way to something more disciplined, more institutional, and perhaps less exciting. Victor Li does not make the front pages of the South China Morning Post the way his father did. He does not deliver memorable aphorisms at annual meetings. He runs spreadsheets, consults advisors, and makes decisions that optimize for risk-adjusted returns rather than headlines.

And yet the machine continues to function. The A.S. Watson IPO, if executed, will be the largest listing in Hong Kong in years. The UKPN sale will crystallize billions in value that the public market never fully recognized. The VodafoneThree merger has created the UK's largest mobile operator from a perennial also-ran. Even the Panama debacle, for all its political drama, may ultimately be resolved through arbitration at a price that compensates for the lost concession.

Li Ka-shing's greatest achievement was not any single transaction—not the Hutchison Whampoa steal, not the Orange windfall, not the 3G gamble. His greatest achievement was building a corporate structure resilient enough to survive his own departure. The ring-fenced debt, the cash-rich holding company, the alignment of family and management incentives, the deep bench of operational expertise accumulated over four decades—these are the institutional assets that outlast any individual. CK Hutchison may never again produce a trade as spectacular as the Orange exit. But it does not need to. The machine was designed to compound steadily, to buy when others panic, to sell when others overpay, and to endure the inevitable stretches of political, economic, and market turbulence that are the price of operating in fifty countries simultaneously.

In a financial world obsessed with the next software platform, the next AI breakthrough, the next cryptocurrency cycle, CK Hutchison represents something deeply unfashionable and perhaps increasingly rare: a company that owns real things. Ports where ships dock. Stores where people buy medicine. Wires that carry electricity. Towers that transmit data. These assets are not weightless and infinitely scalable. They are heavy, capital-intensive, and geographically fixed. They require permits, licenses, and decades of regulatory relationships. They cannot be copied, pasted, or disrupted by a startup in a garage.

Whether that makes CK Hutchison a compelling investment or a relic of a passing era depends on a question that every investor must ultimately answer for themselves: in a world that is becoming more physical, more fragmented, and more geopolitically contested, does owning the infrastructure matter more or less than it did a decade ago?

Li Ka-shing, from his retirement in Hong Kong, already knows his answer. The machine he built is the answer itself.

XI. Top Resources for Further Study

-

Li Ka-shing: Hong Kong's Elusive Billionaire — The definitive biography covering the full arc from refugee to global tycoon, with detailed accounts of the key transactions.

-

The 2015 Reorganization Circular — Filed with the Hong Kong Stock Exchange, this document is a masterclass in corporate restructuring and financial engineering, worth reading for the legal architecture alone.

-

CK Hutchison 2024 Annual Report — The most comprehensive source for segment-level financial data, particularly the retail breakdown for A.S. Watson and the infrastructure portfolio at CKI.

-

The Orange Sale Case Study (Harvard Business Review) — An academic analysis of the 1999 exit that unpacks the timing, the negotiation strategy, and the lessons for corporate deal-making.

-

Canning Fok's rare interviews on the 3G rollout — Available through Hong Kong financial press archives, these interviews provide a first-hand account of the decision-making behind the most controversial capital allocation period in the company's history.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube